A comparative market analysis (CMA) is an estimate of your home's value based on recent sales of similar nearby homes — and it's the document most sellers and buyers actually use to set a price or shape an offer. About 91% of sellers worked with a real estate agent in 2025, according to NAR's 2025 Profile of Home Buyers and Sellers, and almost all of them got their pricing from a CMA, not an online estimator.

Agents build a CMA by pulling three to six comparable sales from the past 3–4 months in the same neighborhood, then adjusting up or down for the differences — square footage, bedrooms, bathrooms, garage, condition, lot size, and view. A good CMA lands within 2–4% of the eventual sale price. A bad one can leave tens of thousands of dollars on the table.

CMAs beat algorithmic estimators because a person walks through the comps. Zillow's published Zestimate accuracy data shows a median error of 1.74% on homes that are actively listed (where Zillow can see asking prices and recent activity), but 7.20% on off-market homes. On a $500,000 house, that's a $36,000 swing — enough to misprice a listing into a stall.

Looking for a CMA without committing to a listing agreement? Most full-service agents will prepare one for free during a listing consultation. Match with a top local agent for a free CMA — and if you list with one, you'll pay a pre-negotiated 1.5% listing fee instead of the usual 2.5–3%.

Our guidance is based on hands-on experience completing comparative market analyses (CMAs) for real sellers and investors.

This article was written by a licensed South Carolina real estate agent who has prepared dozens of CMAs for prospective home sellers. The author is also an active real estate investor and has conducted CMAs to analyze flips and rental properties. These analyses rely on MLS data, recent comparable sales, local market trends, and appraisal benchmarks to determine realistic home values.

The article is also informed by research from Trent Seigfried, a data scientist and real estate writer whose work has appeared in Business Insider, The Christian Science Monitor, and U.S. News & World Report. His research on online home value estimators adds a data-driven perspective to our first-hand market experience.

Overview: What is a CMA?

-

📊 What it is: A report that gives an estimate of a home's value by comparing the recent sale prices of similar properties nearby

-

✍️ Who prepares it: Licensed real estate agents

-

👥 Who it's for: Home sellers, buyers, investors, and refinancers

-

🎯 Best ways to use it: To set a competitive listing price, determine how much to offer on a home, and get negotiating leverage

-

📈 How accurate it is: Often within ~2–4% of the final sale price, versus estimators like Zillow that can be off by ~7% on average

-

💰 What it costs: Many agents will prepare a CMA for free

Want a free CMA? Get matched with a top local realtor.

When to get a CMA, an online estimate, or an appraisal

A CMA, an online estimator, and a licensed appraisal answer related questions but aren't interchangeable. Pick by what you need the number for.

When to get a CMA

- Setting a listing price. A CMA helps you price your home competitively, backed by recent neighborhood sales — the single most common use case.

- Making an offer on a home. This is especially relevant after the August 2024 NAR settlement, when buyers are negotiating agent compensation directly. A buyer-side CMA tells you what comparable homes actually sold for, not just what the seller is asking.

- Investing in a property. Investors use CMAs to underwrite after-repair value and decide what to pay.

- Refinancing. You generally need at least 20% equity for a conventional cash-out refinance, though rate-and-term refinances, FHA streamlines, and VA IRRRLs often allow less. A CMA from a local agent is a quick sanity-check before paying for a full appraisal.

When to use an online home value estimator

Use an online home value estimator if you just want a rough idea of a home’s value. They're convenient and usually free. Online estimators are helpful for:

- Casual research. Pre-listing curiosity, neighborhood scouting, or watching how your equity is trending. Estimators are fast and free.

- Limits to know. Estimators don't see your interior condition, recent renovations, or current micro-market trends. They lean on comps the algorithm picks — which sometimes includes homes on the other side of a school district line or a flood zone.

When to get an appraisal

- Financing or refinancing. Most lenders require a licensed appraisal before they'll close a loan.

- FSBO pricing. Selling without an agent is risky on price — FSBOs sold for a median of $360,000 in 2025 versus $425,000 for agent-assisted homes, a $65,000 gap, per NAR's 2025 Profile of Home Buyers and Sellers. If you're going FSBO, a $300–$500 appraisal is cheap insurance.

- Unique property. Homes with no good comps (an old farmhouse on 40 acres, a custom luxury build) often need an appraiser who can use the cost approach.

Home appraisals run about $323–$428 nationally.[1] Price varies from state to state and depending on the property type.

How accurate is a CMA report?

A well-prepared CMA is typically within 2–4% of the final sale price. On a $400,000 home, that's an $8,000–$16,000 range — narrow enough to set a defensible list price without leaving money on the table.

Online estimator ranges are wider. Zillow's published Zestimate accuracy data shows a median error of 1.74% on homes actively listed for sale, but the error jumps to 7.20% on off-market homes. Redfin's Estimate is similar. The reason is the same on both platforms: algorithms can't see what an agent sees during a walkthrough — a new kitchen, water damage, a converted garage, or how the lot actually drains.

When CMAs are less accurate

CMAs lose precision in slow markets, rural areas, recently rezoned neighborhoods, and on unique homes. The problem is the same in each case: not enough recent, comparable sales to draw from. If your neighborhood has had two sales in the past six months and one was a teardown, the comp set is thin no matter how skilled the agent.

Alex Wright, a former Realtor in Bozeman, Montana and Cody, Wyoming with six years of experience in rural markets, says the core problem is the gap between asking and sold. "The problem is listed and sold are two different things. I saw this a lot during the Bozeman boom. Two houses can look similar, but one backs to a busy road, one has mountain views, one was fully updated, one wasn’t." In slow or rural areas, the fix is to widen the geographic radius, stretch the time window to six months when you have to, and call the listing agents on each comp to understand what’s behind the sale price.

How to make sure yours is accurate

Before you trust a CMA from an agent, ask:

- How recent are your comps? The standard is the past 3–4 months. Six months is the outer edge in stable markets — and even that is too old in a fast-moving one.

- What's the range, not just the point estimate? A good agent will give you a high, low, and most-likely list price.

- Did you adjust for [your specific feature]? A new roof, finished basement, or backyard pool changes the math. If the agent didn't ask, they probably didn't adjust.

- What's your list-to-sold ratio in this neighborhood? Agents who price well consistently sell within a tight band of list price — usually 97–101% in stable markets.

Key factors agents weigh in CMAs

Real estate agents consider multiple factors to estimate a home’s value, including:

- Location: The neighborhood, nearby schools, shops, and the street the house is on

- Recent sales dates: Homes that sold recently are the most important for comparison

- Square footage: The total living space and how it compares to other homes

- Condition and upgrades: How well the home is maintained and any improvements like a new kitchen, bathroom, or roof

- Layout and features: Number of bedrooms and bathrooms, garage, yard, and extras like a pool or fireplace

- Lot size: How big the yard is and how easy it is to use

- Market trends: How many homes are for sale, how many buyers are looking, and whether it’s a buyer’s or seller’s market

- Adjustments for differences: Changes in price to account for differences between your home and similar homes

Adjustments aren't arbitrary. Agents use local market rates ($40–$80 per square foot is common for living-space differences in many markets) and reference recent paired-sales analyses. We'll show real numbers in the Charleston example below.

Caleb Hollis, a Florida certified residential appraiser with more than 20 years of valuation experience, says the mistake is the question sellers start with. "Do not ask, ‘What is the highest number we can justify?’ Ask, ‘What would the next informed buyer reasonably pay after seeing the same alternatives?’ That mindset usually produces a better price than cherry-picking the three most flattering sales."

Comparative market analysis example from an agent

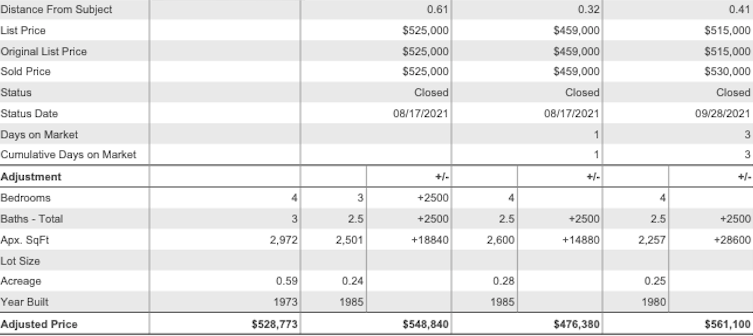

This is an example of a real comparative market analysis that I completed for a home in Charleston County, South Carolina. CMA reports may look different in other markets or states, but they all include the same basic information.

The first two pages of a CMA report include photos and information about the subject property. The third page (image above) provides details on the subject property (second column), along with three comparable sales in the area. Additional pages contain more in-depth information.

How the CMA was prepared

Here’s the process I followed for this example:

- Select comparable homes: I chose three nearby homes that sold in the last four months and were similar in size, condition, and features to the subject property.

- Gather property details: I collected information such as list price, sold price, sale date, distance from the subject property, number of bedrooms and bathrooms, and square footage.

- Adjust for differences: Because every home is unique, I adjusted the prices of the comparable homes. For example:

- The subject home had one extra bedroom, adding $2,500 in value.

- It had a half bathroom more than the comparables, adding another $2,500.

- Additional square footage added between $14,880 and $28,600, based on local market rates.

- Average the adjusted values: After adjustments, the estimated fair market value for this home came out to $528,773.

- Make in-depth adjustments: More detailed CMAs may also adjust for features such as acreage, garage type, or interior and exterior upgrades.

How to do a CMA on your home

Here's how to do a CMA without an agent. This is a basic approach that uses sales data from the home-buying website Zillow.

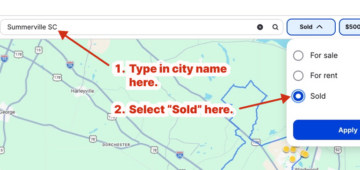

Step 1: Find homes in your area that have sold recently

- Type your city in the Zillow search bar.

- Check the box for "sold homes" to view only closed sales.

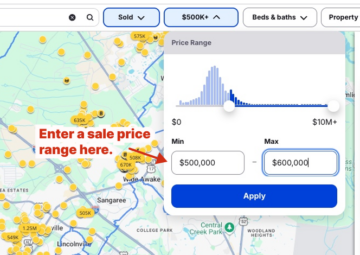

- Choose a sale price range that's within what your home is likely worth.

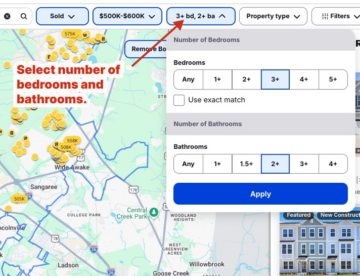

- Select a minimum bedroom and bathroom number that's at least equal to your home.

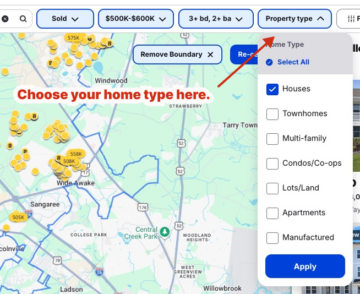

- Choose your home type (single-family house, townhouse/condo, or multi-family).

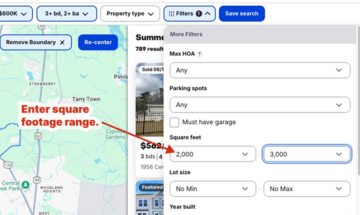

- Add a range of square footage within about 500 square feet of your home.

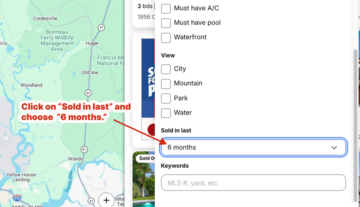

- Under the "sold in last" tab, select homes that have sold within the past six months.

Fill in the information on each Zillow tab, from left to right, to narrow down sold homes in your area.

On the search bar, type in your city, and then on the next tab, check the box for "sold homes" to view only closed sales.

Choose a sale price range that is within what your home is likely worth (using an online home value estimate is okay). For example, if Zillow estimates your home is worth $550,000, you can choose a range of $500,000 to $600,000.

On the next tab to the right, select a minimum bedroom and bathroom amount that's at least equal to your home (don't select "use exact match," which will limit the amount of results).

Choose your home type (single-family house, townhouse/condo, or multi-family) and then hit done.

Select the "filter" tab and add a range of square footage that's within 500 square feet or so of your home. For example, if your home has 2,500 square feet, you can choose a range of 2,000 to 3,000.

Scroll down to the bottom, and select the "sold in last" tab. Select homes that have sold within the past six months.

Hit apply, and zoom in on the map to view all sold homes in your area.

Step 2: Choose three comparable sales

From this list of homes, pick three that are most similar to your home and have sold most recently.

Use these factors to pick the best comparable sales:

- Location: Comparable properties should be located in the same neighborhood or subdivision as the subject property (and no more than a mile away).

- Date of sale: Homes sold within the past three months are ideal comps, and the sooner the closing, the better, given how fast the market can change.

- Size: Agents typically try to stay within 500 square feet of the subject home's square footage.

- Condition: A home and its comparables should have similar interior and exterior upgrades, and be in the same condition. You can browse online photos to see a home's condition and upgrades.

- Age of home: The closer in age, the better, as the market tends to value new and old homes differently.

- Type of home: A brick, ranch-style home isn't a good comparable for a two-story townhouse or condo, for example.

Step 3: Use averages to estimate your home's value

Two ways you can estimate your home's value are by using the average sale price and the average price per square foot of the comparable properties.

Average sale price

Let's say your search returns three solid comps that recently sold for $517,000, $544,000, and $555,000 in your neighborhood.

Based on the average sale price of the three comps, your home's fair market value is $538,667.

| Property | Sale price |

|---|---|

| Comp 1 | $517,000 |

| Comp 2 | $544,000 |

| Comp 3 | $555,000 |

| Your home's estimated value | $538,667 |

Average price per square foot

To get an estimated value, you'll need to divide each home's sales price by its interior square footage.

The average sales price per square foot for the three comps is $202. If your home is 2,500 square feet, it has an estimated value of $505,000.

| Property | Sale price | Square feet | Price per sq. ft. |

|---|---|---|---|

| Comp 1 | $517,000 | 2,553 | $203 |

| Comp 2 | $544,000 | 2,643 | $206 |

| Comp 3 | $555,000 | 2,800 | $198 |

| Your home's estimated value | $505,000 | 2,500 | $202 |

Your CMA won't be as accurate as an experienced agent's. Agents have access to more data and have more local market knowledge. They know in depth what factors affect a home's value and by how much. If you want to set a competitive listing price, we recommend you get a free CMA from a top local agent.

How to get a free CMA

Most real estate agents will give you a free CMA during a listing consultation to win your business and help you set a fair listing price.

To make sure your CMA is accurate and that you don't overprice or underprice your home, it's important to find the right agent. You want to choose a realtor who's highly qualified and knowledgeable about your local market.

Clever Real Estate can match you with top local agents from trusted brands like Century 21 and RE/MAX. You'll receive multiple hand-picked matches so you can compare your options and choose the agent with the best marketing plan and pricing strategy.

In addition, Clever negotiates exclusive savings on your behalf. You'll pay just a 1.5% listing fee in exchange for guaranteed full service from a traditional agent. Try Clever for free and interview as many agents as you want until you find the right fit — or walk away at any time with no obligation.

Match with top-rated agents from brand-name brokerages, like Keller Williams and RE/MAX, and request a free CMA today! Sellers will save thousands in realtor commissions with pre-negotiated 1.5% listing fees.

Clever's service is 100% free with zero obligation. Interview as many agents as you like until you find the perfect fit — or walk away at any time.

FAQ

Real estate agents often provide free CMAs as part of a listing presentation to prospective home sellers before a house is listed for sale. Get a free CMA from a top local agent.

You can do your own CMA reports by researching comparable home sales on real estate websites, such as Zillow or Realtor. But a local realtor can provide a more in-depth analysis of a home's value, and at no cost to you.

A CMA and an appraisal are not the same thing. Real estate agents complete free CMA reports to provide an estimated home value for clients; licensed appraisers complete appraisal reports for banks or lenders who have ordered the report for home buyers.

The primary purpose of a comparative market analysis (CMA) is to determine a property's value. Most real estate agents will perform a free CMA for sellers, allowing them to set an accurate listing price. A CMA can also help a buyer know whether a home is priced well, allowing them to make a competitive offer.

A CMA typically takes 2–4 hours for an agent to prepare if they don’t need to visit your home in person. The main factor is finding a time to review it with you. So after you request a report, it may take a few days or a week to actually get it.

An agent needs data about homes that recently sold nearby that are similar in size, style, age, and condition to your home. The realtor looks at the prices of these homes, then makes an estimate of your home's value based on factors like whether your home has more or less bedrooms and bathrooms, square footage, upgrades, or additional features like a garage or pool.