A 1031 exchange is a tax-deferral strategy that allows the owner of an investment or business property to sell that property and reinvest the proceeds into another “like-kind” property without immediately paying capital gains taxes.

Named after Section 1031 of the Internal Revenue Code, these exchanges offer substantial tax savings for real estate investors and business owners. However, they come with complex rules and regulations and aren't beneficial in every situation.

Our guide covers everything you need to know about 1031 exchanges, including how Clever's co-founder, Ben Mizes, used the 1031 strategy to expand his real estate portfolio from one unit to 26 units.

Given their complexity, consulting an accountant or tax professional before starting an exchange is your best bet.

What is a 1031 exchange?

A 1031 exchange allows the owner of an investment or business property to sell that property and use the proceeds to buy another similar property.

When structured correctly, a 1031 exchange defers — rather than eliminates — capital gains tax and depreciation recapture. The taxes are carried forward into the replacement property and typically come due only when that property is sold without another exchange.

“The tax deferral provided by 1031 exchanges is a major economic incentive for real estate investors,” says Sean Ross, CEO of 1031x. “It allows investors to reinvest their equity without immediate tax penalties, accelerating portfolio growth.”

For a 1031 exchange to be valid, a qualified intermediary must hold the proceeds from the sale until they can be transferred to the seller of the new property.

You must file Form 8824 with your tax return to report the exchange to the IRS.

1031 exchange tips

📅 Plan ahead. In a 1031 exchange, timing is crucial. You must identify a replacement property within 45 days of selling your current property. To ensure success, research the market and identify potential replacement properties before you sell.

🤫 Keep it confidential. Avoid disclosing to the seller that you’re doing a 1031 exchange. They may be less flexible on the price or deal terms if they know you're on a tight timeline. You're not legally required to inform the seller about the exchange, so keep this information to yourself to maintain negotiating leverage.

⏱️ Allow extra time to close. Although you have 180 days to close on the replacement property, unexpected issues can cause delays. Choose a closing date within the 180-day window to ensure you don't run out of time.

How a 1031 exchange works

Most investors complete a delayed (or deferred) 1031 exchange, which follows a specific timeline:

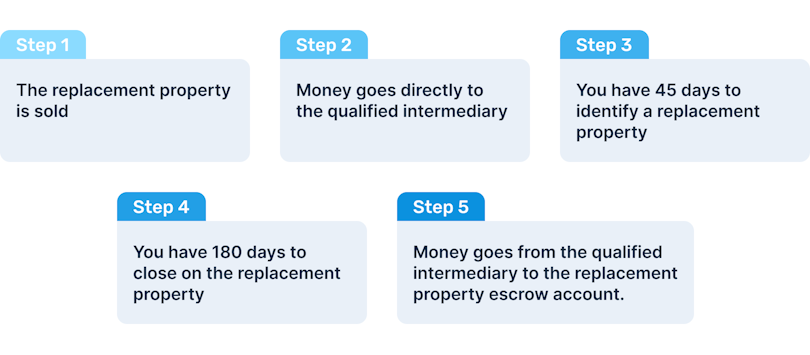

- Sell the relinquished property You sell your investment or business property. The sale contract must reflect your intent to complete a 1031 exchange.

- Proceeds go to a qualified intermediary (QI) You cannot receive or control the sale proceeds. A qualified intermediary — an independent third party — holds the funds to avoid “constructive receipt,” which would trigger taxes.

- Identify replacement property within 45 days Within 45 calendar days of closing the sale, you must formally identify potential replacement properties in writing. This deadline is strict and non-negotiable.

- Close on the replacement property within 180 days You must complete the purchase of the replacement property within 180 days of selling the original property (or by your tax-filing deadline, whichever comes first).

If any step is missed or handled incorrectly, the exchange fails — and capital gains taxes become immediately due.

In a delayed or deferred 1031 exchange, the process involves selling the first property, identifying a new one, and completing the exchange at closing time.

1031 exchange steps to follow

Specify intent for 1031 exchange. When selling the first property, you must declare your intent to perform a 1031 exchange. This ensures the sale proceeds don't go directly to you.

Proceeds to qualified intermediary (QI). The proceeds from the sale must go directly to a qualified intermediary, a non-related third party responsible for holding the money from the sale until it's used to purchase another property. A valid 1031 exchange requires a QI.

Who can be a qualified intermediary?

- There's no official IRS license or certification for QIs.

- The QI must be a third party with whom you have no previous relationship.

- Examples include attorneys, investment bankers, or professional QI services.

- Any person who has acted as your "agent" within the last two years is disqualified.

Tip: Choosing the right qualified intermediary (QI) is crucial for a smooth 1031 exchange process. Look for a QI with specific expertise, a strong reputation, financial safeguards, personalized service, and a clear fee structure to ensure efficiency and minimize risks.

Identify replacement property within 45 days. You have a 45-day window to identify potential replacement or "like-kind" properties. This time frame is strict and essential for the exchange process.

How to identify properties for a 1031 exchange

| Rule | How it works | Best for |

|---|---|---|

| 3 property rule | Identify up to three properties to replace the one being sold, but only need to close on one of them. | Exchanging one property for another. |

| 200% rule | Identify unlimited properties, but their combined value can't exceed 200% of the original property's value. | Exchanging one property for multiple properties. |

| 95% rule | Identify an unlimited number of properties with no maximum value, but must close on at least 95% of their total value. | High-value transactions where a significant portfolio increase is involved. |

Important: Regardless of the rule you choose, the exchange will be voided if you receive any proceeds from selling the first property. Funds must be transferred directly to a qualified intermediary and held until the new property is purchased.

Close on replacement property within 180 days. The 180-day period starts from the closing of the original property sale. You must close on the replacement property within this period to maintain the validity of the exchange.

Funds transfer by QI. The qualified intermediary will transfer the funds to the replacement property's escrow account. This step ensures you don't handle the sale proceeds directly, maintaining the exchange’s integrity.

How much does a 1031 exchange cost?

According to Ross, typical 1031 costs include Qualified Intermediary fees, which normally range between $800 and $1,200 per exchange. However, complicated exchange structures have higher fees.

Ross explains that some QIs charge extra fees for wire transfers, document preparation, or based on the number and value of properties involved.

"A QI might charge $900 for properties under $1 million and $1,500 for properties over $1 million, with additional fees for late notice before closing," he says. "Investors should review their exchange agreements carefully. Additionally, title companies and closing attorneys often charge extra for transactions involving a 1031 exchange."

Tax savings vary depending on the specifics of each investment property. According to Ross, taxes on the sale of appreciated property can range from 15% to over 30%, depending on the property's location and the investor's income bracket.

Other costs may be associated with the exchange, such as appraisal fees, escrow fees, and any necessary repairs or improvements to the replacement property to meet the exchange criteria.

Consult with a financial advisor or tax professional to help you determine if the benefits of a 1031 exchange justify the costs.

What is a "like-kind" property?

In a 1031 exchange, both the relinquished and replacement properties must be considered “like-kind,” a term that often causes confusion.

According to the IRS, like-kind refers to the nature or character of the property, not its quality or value. Nearly all U.S. real estate held for investment or business use is considered like-kind to other U.S. investment real estate.[1]

For example, you can exchange:

- An apartment building for vacant land

- A rental home for a commercial property

- A warehouse for an office building

However, some property types don’t qualify, including:

- Primary residences

- Fix-and-flip inventory

- Property held mainly for resale

- Foreign real estate exchanged for U.S. property

"The IRS defines like-kind property as any real property held for investment or in use in trade or business," Ross explains. "Virtually any type of real property could fit this definition: raw land, residential property, commercial property, farmland, single-family, multifamily, tenant-in-common interests, industrial property, and more."

While finding a "like-kind" property imposes some limits on your 1031 exchange, there's more flexibility than most people realize. The term "like-kind" can be misleading, encompassing various property types.

What is the "boot?"

"Boot" or "mortgage boot" is a term commonly used in the context of 1031 exchanges. Although not a technical term the IRS uses, it refers to any cash received in the exchange that isn't reinvested in the replacement property.

This can occur if the mortgage on the new replacement property is less than the mortgage paid off when the original property was sold.

For example, if the mortgage balance on the original property was $100,000 at the time of sale, but the mortgage needed for the replacement property is only $80,000, the "boot" would be $20,000.

This $20,000 debt reduction is a taxable cash benefit and will be taxed as a capital gain.[2]

3 reasons to use a 1031 exchange

There are three important reasons why savvy business people or real estate investors would use a 1031 exchange.

1. Defer capital gains

The primary reason for using a 1031 exchange is to defer the payment of taxes on your profits.

When you sell a property, you’re typically taxed on your capital gain — the difference between what you paid for the property and what you sold it for. Capital gains tax can add up quickly, especially if you’re selling a valuable property or something significantly appreciated.

Capital gains tax includes federal and state taxes, depreciation recapture, and possibly the Net Investment Income Tax (NIIT) of 3.8% if your income exceeds the IRS threshold.[3]

For example, if you purchased a four-unit residential property in California for $250,000 and sold it 10 years later for $400,000, you would have a capital gain of $150,000. After accounting for $30,000 in depreciation and $5,000 in eligible closing costs, your actual gain is $175,000. Adding federal capital gains tax (15%), California capital gains tax (13.3%), and depreciation recapture (25%), your tax liability would be $52,525!

However, with a 1031 exchange, you could defer this hefty tax bill by acquiring a replacement property of equal or greater value. In some cases, you may never pay capital gains tax at all. If you die before selling a property acquired through a 1031 exchange, the government forgives the capital gains tax, making 1031 exchanges an interesting option for estate planning.

You should talk to an accountant, tax advisor, or financial planner to determine if a 1031 exchange is a good idea.

» Understanding Capital Gains Tax on Real Estate Investment Property

2. Avoid depreciation recapture

Landlords can record depreciation on their investment properties to offset income tax, even though most properties appreciate over time. Depreciation is allowed because it’s assumed that tenants will wear and tear the properties.

However, when you sell an investment property at a gain, the IRS "recaptures" the depreciation, taxing the total depreciation recorded during ownership. Here's an example:

- Suppose you bought an investment property for $200,000 and claimed $50,000 in depreciation over 10 years. Your adjusted cost basis is now $150,000 ($200,000 - $50,000).

- If you sell the property for $300,000, your capital gain is $150,000 ($300,000 - $150,000).

- The $50,000 depreciation you claimed is subject to recapture at 25%. This means you would owe $12,500 in depreciation recapture tax ($50,000 x 25%).

A 1031 exchange allows landlords to sidestep depreciation recapture by building their portfolio without being hit by the depreciation they’ve benefited from for years.

Depreciation recapture will eventually come into play if the replacement property is sold, but a 1031 exchange can delay this tax liability.

3. Leverage equity

By exchanging a property you already own for one (or several) that could increase your cash flow, you’re effectively "leveling up" your investment. Every new purchase has a cost, but using a 1031 exchange can minimize the cost and potentially improve your investment's upside.

1031 exchange case study from Clever's co-founder

I'm Ben Mizes, co-founder and CEO of Clever Real Estate. In under two years, I used the power of 1031 exchanges to significantly expand my real estate portfolio from a single unit to 26 units.

I began my investment journey by purchasing and rehabbing small multifamily units in St. Louis, Missouri. This process taught me various skills, from installing new flooring to managing tenants.

However, discovering 1031 exchanges transformed my investment strategy. It allowed me to defer capital gains taxes and reinvest my profits into larger, more valuable properties.

After successfully renovating a fourplex, my investment partner and I set our sights on a more ambitious project: an 18-unit apartment building. We utilized a 1031 exchange to sell our existing properties and reinvest the proceeds into the new acquisition, deferring the capital gains taxes that would have otherwise eaten into our profits.

Despite the strict 45-day identification and 180-day closing windows imposed by the IRS, we completed the exchange just in time, which was crucial for securing the new investment. This strategic use of 1031 exchanges enabled us to rapidly scale our portfolio and maximize our investment returns.

One crucial piece of advice from my experience is to find your new deal before selling your current property. You must have a solid investment lined up and be able to proceed smoothly with the 1031 exchange. When we identified the 18-unit complex we wanted to acquire, we went under contract for it first and then listed our existing property for sale.

This strategy prevented us from scrambling to find a replacement property and potentially ending up with a bad deal just for the sake of tax savings. Always secure your next investment before selling to avoid unnecessary risks.

The bottom line

When the numbers make sense, 1031 exchanges can be a great way to leverage equity and continue to build your investment property portfolio or scale up the assets in your business.

Successfully navigating a 1031 exchange could also save you thousands of dollars in capital gains taxes, leaving you with more money for other business expenditures.

However, because the rules and regulations surrounding 1031 exchanges can be confusing, talk to an accountant and get their advice on how to proceed.

FAQ

How much does a 1031 exchange cost?

A 1031 typically costs between $800 to $1200 per exchange. These costs often include fees for the qualified intermediary and legal and administrative expenses. Other associated costs may include appraisal fees, escrow fees, and any necessary repairs or improvements to the replacement property to meet the exchange criteria.

Are there any risks with a 1031 exchange?

Yes, there are risks involved in a 1031 exchange, such as:

- Failing to identify the right replacement property within the 45-day window.

- Not closing on the replacement property within the 180-day period.

- Accidentally receiving sale proceeds, which would void the exchange and trigger a capital gains tax.

- The seller of the replacement property backing out, preventing you from completing the exchange.

How long does a 1031 exchange take?

A 1031 exchange must be completed within 180 days from the date you sell your old property to the date you close on the replacement property. However, the process can be quicker if you promptly identify and close a new property.

Can you use a 1031 exchange to purchase a primary residence?

No, the purpose of a 1031 exchange is to exchange properties used for business or investment purposes. Primary residences don't qualify for a 1031 exchange.

Can you have a mortgage in a 1031 exchange?

Yes, you can have a mortgage in a 1031 exchange. The profits from the sale of the first property can be used to pay off the remaining principal on the mortgage, and a new mortgage can be secured for the replacement property.