When you've owned a rental property for several years and are curious about whether selling now would be a good financial decision, many investors and landlords face similar challenges. Property purchased years ago has appreciated substantially, and once the equity starts growing, owners wonder if they could unlock a large gain by selling ... and how much of that potential profit will go toward taxes on the sale.

While selling a primary residence can be complicated, selling an investment property is typically even more convoluted. Instead of a single tax, most investment property sellers face layers.

The gain itself is usually taxed at the federal long-term capital gains rate. But landlords may also owe depreciation recapture, which taxes deductions taken over years of rental ownership. Higher-income investors may also face the net investment income tax (NIIT).

All variables considered, investment property owners can end up with a larger tax bill than they expect when they first consider selling. To be sure you get the most value, it's important to be prepared and to understand how taxes on investment property sales work and how depreciation affects your taxable gain. Strategies such as a 1031 exchange, an installment sale, or careful timing can sometimes reduce or defer the tax burden.

{kind=link}

How much tax will you actually owe?

In an investment property sale, the tax bill is made of three layers, each applying to a different part of the gain.

For example, if an investor buys a duplex for $350,000 in 2018 and rents it out until selling in 2026 for $575,000, the total tax bill can include:

- Long-term capital gains tax

- Depreciation recapture tax

- Net investment income tax (NIIT)

Understanding how each layer works makes it easier to estimate the final tax bill before selling and determine if now is the right time.

Short-term vs. long-term gains

The tax amount in the first layer is dependent on how long the property was held.

If an investment property owner sells within one year of purchase, the profit is treated as a short-term capital gain taxed as ordinary income. Depending on the seller’s tax bracket, that rate can be as high as 37%.[1]

Because most rental properties are held longer than a year, the gain qualifies for long-term capital gains rates, which are lower than standard income tax rates.

For the 2026 tax year, the long-term capital gains brackets are approximately:[2]

| Rate | Single filer | Married filing jointly |

|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 |

| 15% | $49,451 – $545,500 | $98,901 – $613,700 |

| 20% | Above $545,500 | Above $613,700 |

Although most investment property sellers fall into the 15% long-term capital gains tax bracket, the final rate depends on total taxable income in the year the property is sold. That taxable income includes wages, business income, and other investment income. In short, waiting past a year to sell can lower your tax bill.

Depreciation recapture: The tax most landlords overlook

Rental property owners benefit from depreciation while they own the property, which is a major tax deduction.

Under the IRS’s Modified Accelerated Cost Recovery System (MACRS), residential rental property is depreciated over 27.5 years.[3] Each year, owners can deduct a portion of the building’s value from taxable income.

When the property is sold, the IRS requires those deductions to be accounted for in the gain calculation. The part of the gain attributable to depreciation, known as unrecaptured Section 1250 gain, is usually taxed at a maximum federal rate of 25%.[2]

Using the example property:

- Purchase price: $350,000

- Allocation:

- $280,000 structure

- $70,000 land (land cannot be depreciated)

- Allocation:

- Annual depreciation: $280,000 ÷ 27.5 ≈ $10,182 per year

- If the property was owned for eight years: 8 × $10,182 ≈ $81,455 total depreciation

That portion of the gain may be taxed at up to 25% when the property is sold, depending on the seller’s overall tax situation.

Another important standard is the IRS’s “allowed or allowable” rule. Even if a landlord did not claim depreciation deductions during ownership, the IRS generally treats the property as if those deductions were taken when calculating the gain.

Depreciation also lowers the property’s adjusted basis (purchase price plus improvements minus depreciation), which increases the taxable gain when the property is sold.

The net investment income tax (NIIT)

The third tax layer applies to higher-income investors.

The net investment income tax (NIIT) tacks on another 3.8% federal tax on certain investment income, including capital gains from property sales, when income is above $200,000 for single filers or $250,000 for married couples filing jointly.[4]

Unlike depreciation recapture, which applies only to the depreciation portion of the gain, the NIIT is calculated on the lesser of the total investment gain or the amount by which the seller's modified adjusted gross income (MAGI) exceeds the applicable threshold. When other income already pushes the seller past the threshold before the gain is counted, the NIIT can apply to the entire investment gain. When it doesn't, which is common for sellers with moderate earned income, it applies only to the portion of the gain that crosses the line.

For higher-income sellers, the combined federal tax exposure can look like:

- Up to 23.8% on long-term capital gains (20% + 3.8% NIIT)

- Up to 25% on depreciation recapture

This layered structure explains why investment property sales often produce larger tax bills than many landlords initially expect.

A real example: What the tax bill looks like

To see how these taxes combine, consider a real-world example.

Scenario:

- Single filer

- $180,000 W-2 income

- Duplex purchased in 2016 for $350,000

- Allocation:

- $280,000 structure

- $70,000 land

- Sold in 2026 for $575,000

Step 1: Calculate accumulated depreciation

Annual depreciation: $280,000 ÷ 27.5 ≈ $10,182

After 10 years of ownership: 10 × $10,182 ≈ $101,820

Step 2: Determine adjusted basis

Adjusted basis: $350,000 − $101,820 = $248,180

Step 3: Calculate total gain

Sale price − adjusted basis: $575,000 − $248,180 = $326,820 total gain

Step 4: Apply the tax layers

Layer 1: Depreciation recapture

- $101,820 × 25% = $25,455

Layer 2: Long-term capital gains

- Remaining gain: $326,820 − $101,820 ≈ $225,000

- Capital gains tax: $225,000 × 15% = $33,750

Layer 3: Net investment income tax

- Total income including gain(MAGI): $506,820

- MAGI excess over $200,000 threshold: $306,820

- NIIT: $306,820 × 3.8% ≈ $11,659

Estimated federal tax

Total federal tax: $25,455 + $33,750 + $11,659 ≈ $70,864

That equals an effective federal tax rate of roughly 21.7% on the total gain.

Also consider state taxes, which can further increase the total bill. Many states tax capital gains through their normal income tax system, though some states, including Texas, Florida, and Nevada, have no state income tax.

In high-tax states such as California, the top rate reaches 13.3%, while states like Texas, Florida, and Nevada have no state income tax.[5]

What investment property sellers can't use, and what they can

In most cases, the home sale exclusion under Section 121 applies only to primary residences.[5] However, some property owners convert a rental property into their primary residence before selling.

If the owner lives in the home for at least two of the five years before the sale, they may qualify for a partial capital gains exclusion.

There are two important limitations.

- Depreciation claimed after May 6, 1997, cannot be excluded and may still be taxed at the up-to-25% rate.[6]

- The exclusion may be reduced for periods when the property was used as a rental rather than a primary residence.

Because the rules are complex, owners considering this strategy should consult a CPA or tax professional before relying on it.

Strategies to reduce or defer capital gains tax

While it’s difficult to eliminate taxes when selling an investment property, several strategies may help reduce or defer the tax bill. Each option works best in specific situations and has its own trade-offs, so the right approach depends on the investor’s long-term goals.

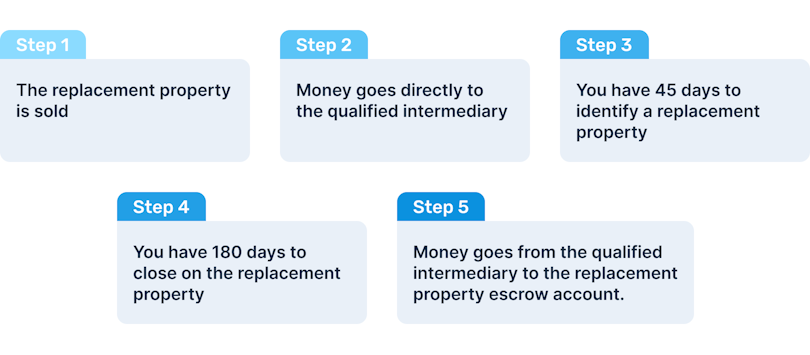

1031 exchange: defer the tax and reinvest the gain

One of the most common tools real estate investors use is the 1031 exchange, which allows an investor to sell one property and reinvest the proceeds into another “like-kind” investment property, deferring both capital gains tax and depreciation recapture.[7]

Strict timing rules apply:

- 45 days to identify a replacement property

- 180 days to close on the purchase

- A qualified intermediary must handle the transaction

This approach works best when investors want to:

- Stay invested in real estate

- Upgrade to a larger or higher-performing property

- Reinvest the full sale proceeds rather than paying taxes immediately

However, a 1031 exchange may not make sense if the seller wants to exit real estate investing or needs immediate access to the proceeds.

"While it can be an excellent strategy to defer both capital gains tax and depreciation recapture," said Chris Picciurro, CPA, "it also comes with strict timelines and rules that investors need to understand before they sell."

"Another important point is that a 1031 exchange should rarely be viewed as a one-time tax decision," he said. "The most successful investors use exchanges as part of a long-term strategy to grow and reposition their real estate portfolio over time."

Recent tax legislation also reinforced the long-term viability of this strategy. The One Big Beautiful Bill Act (2025) preserved 1031 exchanges after earlier proposals to limit them were debated.[8]

Tax-loss harvesting

Investors sometimes offset real estate gains with losses from other investments.

For example, if an investor sells stocks at a loss during the same tax year, those losses can offset capital gains from the property sale, dollar-for-dollar.

If total losses exceed gains, up to $3,000 can offset ordinary income, and additional losses can carry forward to future tax years.

Because this strategy requires careful timing, it’s typically part of year-end tax planning with a financial advisor or CPA.

Installment sale

Another option may be an installment sale, in which the buyer pays the purchase price over multiple years. Because the seller receives the proceeds gradually, part of the capital gain may also be recognized over several tax years, potentially lowering the tax bracket applied to those gains.[9]

For residential rental property depreciated on a straight-line basis, the portion of the gain attributable to depreciation is not required to be recognized entirely in the year of sale. Instead, it is spread across installment payments but allocated first, meaning earlier payments carry the 25% rate until the full depreciation-related gain is accounted for. Later payments are then taxed at the lower long-term capital gains rate.

Installment sales tend to work best when:

- The buyer is open to seller financing

- The seller does not need the full payment immediately

Timing the sale strategically

Sometimes the most practical strategy is choosing the right year to sell.

Because capital gains tax brackets depend on total income, selling during a lower-income year may reduce the rate applied to the gain.

Situations where timing may matter include:

- Retirement

- A career change

- A year with unusually low business income

- Large deductible losses elsewhere

Even relatively small timing differences can have a noticeable impact. For example, the difference between a 15% and 20% capital gains rate on a $200,000 gain is $10,000.

For that reason, many investors consult a CPA before listing a property to evaluate whether adjusting the timing could meaningfully reduce taxes.

Holding the property until death (stepped-up basis)

Another rule sometimes part of long-term estate planning is a step-up in cost basis. When heirs inherit property, the cost basis is typically reset to the fair market value on the date of death.[10]

This adjustment eliminates accumulated capital gains and depreciation recapture. As a result, heirs who sell the property shortly after inheriting it may owe little or no capital gains tax.

However, this strategy primarily benefits heirs rather than the current owner, so it is usually considered in the context of estate planning rather than near-term tax reduction.

How to calculate your capital gains (and get help)

If you’re considering selling a rental property, estimating the potential gain ahead of time can help you understand the tax implications.

The basic calculation usually involves three steps.

1. Determine your adjusted basis, which typically equals:

Purchase Price + Capital Improvements - Accumulated Depreciation

2. Calculate the total gain. Subtract the adjusted basis from the expected sale price.

3. Identify the applicable taxes, which may include:

- Depreciation recapture

- Long-term capital gains tax

- The net investment income tax

In practice, the final calculations appear on IRS Schedule D and Form 4797. Because investment property sales involve several interacting tax rules, many investors work with a CPA or tax advisor during the year they sell, even if they normally handle their own tax filings.

Planning and understanding how these tax layers work can make a major difference in how much of the sale proceeds you ultimately keep.

FAQ

Is capital gains tax the same for an investment property as a primary residence?

No. Investment property doesn't qualify for the Section 121 exclusion ($250k/$500k) that primary residence sellers can use. You'll also owe depreciation recapture tax (up to 25%) on any depreciation claimed during ownership, plus potentially the 3.8% NIIT. The rules are meaningfully different, and the tax bill is typically higher.

What is depreciation recapture, and do I have to pay it?

Yes. If you claimed depreciation deductions on your rental over the years, the IRS requires you to "recapture" those benefits when you sell, taxed at up to 25% — even if you never claimed them (the IRS uses the "allowed or allowable" standard). It's calculated on total accumulated depreciation against the building's cost basis, not the land.

Can I avoid capital gains tax on investment property with a 1031 exchange?

A 1031 exchange defers, not eliminates, the tax. You sell one investment property and reinvest all proceeds into a "like-kind" replacement property, delaying capital gains and depreciation recapture taxes until you eventually sell the new property. You must identify a replacement within 45 days and close within 180 days. See our full 1031 exchange guide for rules and timelines.

How do state taxes affect capital gains on investment property?

Most states tax capital gains as ordinary income, meaning no preferential "capital gains rate" at the state level. California taxes investment property gains at up to 13.3%, stacked on top of federal taxes. States like Texas, Florida, and Nevada have no state income tax. Always factor in your state's rate when modeling net proceeds from a sale.