House hacking is simple in concept: buy a property with multiple units, live in one, and rent out the rest so your tenants help cover your mortgage. In the best-case scenario, you live for free. In a realistic scenario, you pay a fraction of what your housing costs would be otherwise.

The thing most guides don't tell you is that house hacking isn't really a real estate investment strategy in isolation: rather, it's a way to start building a real estate portfolio by getting paid to own your first property. Every month that you collect rent, you're building equity, reducing your out-of-pocket housing costs, and learning how to be a landlord in a relatively low-stakes environment.

But it's not effortless. You're signing up to manage tenants, handle maintenance calls, and live in close proximity to people you're in a business relationship with. Whether that tradeoff makes sense depends on your market, your finances, and your personality.

This guide covers how to find, finance, and evaluate a house hack — including a real deal breakdown from Clever's co-founder — so you can decide if it's right for you.House hacking means you live in one unit of house (often a duplex, triplex, or quadriplex) and rent out the remaining units. Basically, you’re signing up to be a live-in landlord.

What is house hacking?

How house hacking works

- Find an empty 2- to 4-unit house. Traditionally, house hacking involves living in one unit of a duplex, triplex, or fourplex (although it may also work with a single-family home). But you can also hack a guest house, converted garage, or mother-in-law suite.

If you want to start even smaller, buy a single-family home and rent the extra bedrooms. Just make sure you have enough bathrooms — and that you’re okay sharing your space with strangers!

Many lenders won’t underwrite a house with more than four units, and it may be more than you can handle without taking on full-time responsibilities or hiring a property manager. - Finance your purchase. Buying with the intent to house hack isn’t too different from a traditional home purchase since you’ll live in it. However, if you’re counting on having a low down payment, know that most government-backed loans restrict rental properties and how long you live there.

Tell your lender about your plans to have tenants as they may offer you loan options with a lower down payment or a favorable interest rate.

- Find tenants. After you close on the house, you can start looking for renters. A good rule of thumb is to charge 1% of the home’s value as rent, and for tenants to earn three times the rent. This is referred to as the 1% rule in real estate.[1]

So, for a $225,000 house, you might charge a monthly rent of $2,250 (1%) per unit. In that case, your ideal tenant may earn a gross monthly income of about $6,750.

Read a real-life house hacking breakdown from Clever’s co-founder.

Scenario 1: Large single-family home, room rental

Let's say you buy a five-bedroom house for $625,000, put 20% down, and rent out four rooms at $800 each:

| Expense | Monthly cost |

| Mortgage (at 7% APR) | $3,327 |

| Property taxes | $250 |

| Insurance | $83 |

| Repairs and maintenance | $125 |

| Vacancy rate (5%) | $160 |

| Total expenses | $3,945 |

| Rent from 4 tenants | +$3,200 |

| Out-of-pocket monthly | ~$745 |

The rental income from four rooms covers about 87% of your total monthly costs, leaving you to pay just $745 for everything.

Scenario 2: Duplex with FHA financing (budget-friendly entry point)

For buyers who can't swing a $625,000 property, here's how a duplex works:

| Expense | Monthly cost |

| Mortgage on $350k duplex, 3.5% FHA down, 7% APR | $2,415 |

| Property taxes | $250 |

| Insurance | $120 |

| Repairs/maintenance | $150 |

| Vacancy reserve (5%) | $75 |

| Total expenses | $3,010 |

| Rent from unit 2 | +$1,400 |

| Out-of-pocket monthly | ~$1,610 |

Compare that to renting a one-bedroom apartment in most metros — and you're often paying less while building equity each month. Your FHA down payment on a $350,000 duplex would be $12,250. After one year of required owner-occupancy, you can move out and convert both units to full rentals.MORE: 5 Best Ways to Invest $10k in Real EstateDespite a tight housing market, house hacking is definitely still possible — even for first-time buyers. Higher housing prices and mortgage rates are squeezing margins, but the savings can make it a smart strategy.

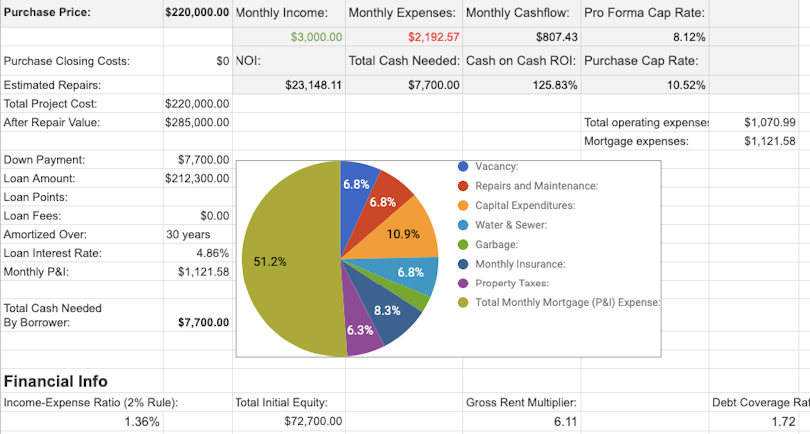

Let’s say you buy a large five-bedroom house for $625,000, put 20% down on the loan, and rent out four rooms at $800 each. Here’s how it can work:

| Expense | Annual cost | Monthly cost |

|---|---|---|

| Mortgage (at 7% APR) | $39,924 | $3,327 |

| Property taxes | $3,000 | $250 |

| Insurance | $1,000 | $83 |

| Repairs and maintenance | $1,500 | $125 |

| Vacancy rate (5%) | $1,933 | $160 |

| Total expense | -$47,357 | -$3,945 |

| Rent from tenants | +$38,400 | +$3,200 |

| Out-of-pocket costs | -$8,957 | -$745 |

The rental income from the four rooms would cover ~87% of your mortgage, leaving you to pay just $745 monthly for everything else. Compare that to paying the full monthly mortgage plus taxes, insurance, and other expenses if you lived there alone.

MORE: 5 Best Ways to Invest $10k in Real Estate

Is house hacking right for you?

House hacking could work for:

- Those who work from home, are handy, or can afford contractors

- Singles or couples who don’t need a ton of exclusive space

- Families that want to rent out units to family members (kids, siblings, in-laws) at discounted rates

It’s not for you if you:

- Live in an expensive market — if you can’t afford a house for yourself, you likely won’t be able to finance a rental property

- Don’t have the bandwidth to be a landlord

- Need more space than a single apartment unit to yourself, especially if you have a large family (most apartments have 1–3 bedrooms)

What the first year actually looks like

The math looks good on paper. Here's what the experience tends to look like in practice:

Months 1–2: You close, move in, and scramble to find a tenant for the vacant unit. This is often the hardest part. Budget for 1–2 months of vacancy and don't panic — it's normal.

Months 3–6: You settle into a rhythm. Rent comes in, mortgage goes out. You learn quickly that being a landlord means being reachable when the water heater fails on a Saturday.

Months 6–12: You start to see the math actually work. The rental income begins to feel less like a windfall and more like a reliable system. Many investors start running numbers on their next property during this phase.

Year 2+: If your tenants are stable, this transitions from active management into something closer to a passive income stream. Experienced house hackers typically move out after year one, convert all units to rentals, and begin searching for their next property.

The investors who struggle most are usually those who didn't screen tenants carefully, picked a property in a market with flat rents, or underestimated how long a vacancy could last. All three are avoidable with solid due diligence before you buy.

Top real estate investing markets

Our state guides provide detailed insights into the top real estate investing markets across all 50 states. We analyze and rank the top 5 markets in each state based on key metrics such as property values, population trends, economic indicators, and more.

AL | AK | AR | AR | CA | CO | CT | DE | FL | GA | HI | ID | IL | IN | IA | KS | KY | LA | ME | MD | MA | MI | MN | MS | MO | MT | NE | NV | NH | NJ | NM | NY | NC | ND | OH | OK | OR | PA | RI | SC | SD | TN | TX | UT | VT | VA | WA | WV | WI | WY

If you already own a big house or building but don't want to be a landlord because it doesn’t fit your long-term goals, you have a couple of alternative options for making the most of your space.

- Rent-to-own: You can offer your tenants a rent-to-own contract — they’ll eventually buy out the unit.

- Vacation rentals: You can host short-term guests. Private spaces are more popular than shared spaces. But you’ll need to pay a fee to a hosting platform, such as Airbnb or Vrbo, and keep the rental space in hotel-level quality.

If you’re just starting to invest in real estate, consider a rehab loan instead of house hacking. It’ll allow you to buy a fixer-upper for cheap, rehab it, and live in it for 3 to 5 years. You can pay less for it and then sell it for more.

House hacking pros and cons

Pros

- Smaller mortgage payments

- Faster mortgage payoff

- Easy wealth-building

- Flexibility

Cons

- Extra responsibilities

- Extra carrying costs

- Extra taxable income

One of the key benefits of house hacking concerns is that it pays for itself. Depending on how high you set the rent, you can take advantage of smaller out-of-pocket mortgage payments. You can also use that extra cash to pay off your mortgage faster (and gain equity) or other expenses, like insurance.

With house hacking generating passive income — earning money with relatively little effort or input — a few months of high occupancy can start netting you some profit. That can offer you flexibility to continue investing, expand your portfolio, or even scale back a full-time job if you're doing well.

Since you’re setting the rent, you also have the flexibility to charge rents that could help you pay the bills or be competitive enough to attract and retain tenants. You can even allow family members to live with you at reasonable rates.

But there’s always risk and responsibility to house hacking, as with all forms of investing. As a landlord, you’ll have to:

- Find and vet renters

- Ensure you’re following local landlord and tenant ordinances

- Be available for repairs and emergencies (or have reliable contractors)

- Pay carrying costs when you can’t rent out other units — this is called the “vacancy rate”

If you decide that house hacking isn’t for you anymore, you may have a hard time selling the property. Multi-family homes are less popular than single-family, and coordinating around tenants introduces its own complexities — for example, transferring leases.[2]

Your best bet would be to sell to another investor. Free services like Clever Offers and Sundae help you find and compare cash offers for homes with renters.

Compare multiple offers from trusted cash buyers in your area against the sale price you'd get with an agent. Clever Offers is free, and there's no obligation to accept an offer from our investors. Simply tell us about your property, and we'll do everything we can to get you the best possible price for your home.

Get Cash OffersPlus, any additional income is taxable; see the IRS guidelines on Rental Real Estate Income.

Common house hacking mistakes

There are plenty of ways house hacking can go wrong. Here's how you can avoid the most frequently made mistakes.

- Picking the wrong property type. Duplexes are easiest to manage but generate less income than triplexes or fourplexes. Many beginners default to duplexes when a triplex in the same neighborhood would generate enough rent to cover the entire mortgage. Model all options before committing.

- Underestimating vacancy. If you plan for 100% occupancy, one empty unit for two months will stress your finances. A 5–8% vacancy buffer in your cash flow projections is standard practice — build it in from the start.

- Not screening tenants carefully enough. Living next door to a problem tenant is a very different experience from owning a distant rental. Verify income (aim for renters earning 3x monthly rent), check references, and run a background check. Don't skip these steps just because someone seems like a nice person at the showing.

- Forgetting about the occupancy requirement. Government-backed loans (FHA, VA) require you to occupy the property as your primary residence for at least one year. Renting out all units while you live elsewhere isn't just a lease violation — it can constitute mortgage fraud. Know your occupancy requirements before signing.

- Buying in a landlord-unfriendly market without knowing it. Eviction laws vary dramatically by city and state. Some markets require 12+ months to complete an eviction, which dramatically raises your risk profile as a landlord. Research local tenant protection laws before you buy.

House hacking real-life example from Clever

From Ben Mizes, co-founder of Clever Real Estate

In 2017 I decided that I was going to get into real estate investing, and I was going to start by house hacking. I had two neighborhoods that I wanted to live in — one in St. Louis City and the other in the St. Louis County.

This was before I was a licensed agent, so I went online and found a real estate agent, and set up MLS alerts to look at every fourplex in those zip codes that hit the market.

I only wanted to look at fourplexes, as they offer more cash flow in my market. Additionally, they offer three streams of tenant income vs just one in a duplex (once you move into one unit), which means less risk.

My agent and I looked at several houses, but the best one would leave me barely breaking even — and was over $400k.

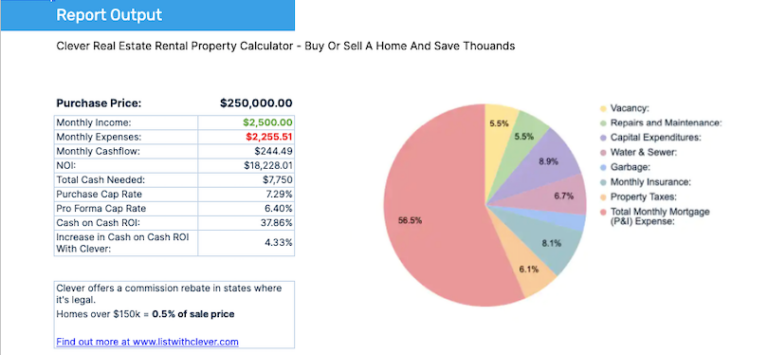

Then one morning I got an email about a fourplex that had hit the market for only $220k, and rented for a total of $2,300 per month. The property barely had any photos and the owner wouldn’t do any showings without an accepted contract. The units were about 900 square feet and the rent seemed low for that size.

Depending on what the insides of the property looked like, I thought that this could be a good deal. I was in a hot market, so my agent and I put in a full-price offer with a walkthrough and inspection contingency — so I could back out if the house wasn’t what I expected.

It turns out I hit the jackpot.

This owner was selling because they were having an affair with their property manager, but they’d just caught the property manager having relations with someone else!

I’ll save you the details of the love triangle, but the owner was no longer receiving the rents from his property manager, and needed to sell asap. He also chose a new agent that had never sold a property like this before, and it was not priced appropriately.

The neighborhood this property is located in used to be rough, but has rapidly improved in the last decade. This property used to house a drug dealer and was hit by a molotov cocktail that resulted in fire large enough that an insurance settlement redid all of the interiors — new kitchens, plumbing, floors, paint, etc.

The moment we stepped inside, I looked at my agent and we both realized I’d stumbled into a home run. We breezed through the inspections and I was able to negotiate another $5,000 in repair credits to redo the roof and a minor sewer repair. The property didn't need anything else beyond that!

Over the next year I raised the rents to $795 for any units that tenants moved out of, and the building’s numbers looked like this:

Shortly thereafter, I sold the building for $285,000, and used the resulting $60,000 in profit to 1031 exchange into a portfolio of 18 apartments.

While I got lucky on the specifics of this deal, I was only able to find it because I put in 100+ hours modeling properties with my calculator, searching on Zillow, and going to showings. When the moment finally came, I was able to realize that this deal had potential — and was confident enough to trust my numbers and take action.

One thing I love about real estate is that you don’t need to be right often — you just need to buy a few good deals and you can build a huge portfolio.

The confidence from this house hack gave my partner and I the guts to go after something a lot harder: our first full renovation of a 6,000-square-foot building for our second house hack.

Finding a property to house hack

Now that we know how to model potential properties to identify a good deal, it's time to find one!

When it comes to finding your first house hack there’s two main ways to find them, and I’ve had success with both methods!

MLS Alerts

Setting up MLS or property alerts and checking out properties as soon as you get an email is incredibly important if you want to get the jump on new investment opportunities.

The MLS is the network that agents use to list new properties that gets pushed out to sites like Zillow or Trulia, and it's the best place for real-time housing data.

If you ask your agent, they will set you up with MLS alerts that notify you every time a property that matches your criteria is listed. When I did this, I had my agent set up instant alerts every time a fourplex was listed between $100,000-400,000 in any of my desired zip codes.

Once you have your alerts set up, it's important to open the emails you get ASAP - in my experience good deals go fast, and you don’t want to miss out on your house hack because you were asleep at the wheel.

This is when getting comfortable with your market and the rental property calculator will come in handy. When a good deal hits the market you need to be able to model it quickly, then have a team in place — i.e., your agent and lender — to act fast and submit a strong offer.

Finding off-market deals

If finding something for sale on the MLS that meets your goals is proving to be tough, a great strategy is to look for deals off market.

While there are tons of ways to find off-market properties, many of them are expensive and involve making hundreds of phone calls and/or sending thousands of yellow letters to find sellers.

These methods are good for professional investors, but don’t make sense if you’re just looking for a house hack.

A simple way that’s worked for me is to drive around town and look for old "for rent" signs, then Google the property to see if it's listed for rent on Zillow. If you find a property that’s for rent but isn’t listed on the popular rental sites, it's a good sign that you might have found an older owner that isn’t very tech savvy, and they might be ready to sell and retire.

This also works with properties on Craigslist that aren’t for rent anywhere else. One of the best deals I ever found — my second house hack — came from this strategy!

Download real estate software for more help

You can also download useful investing software to help you as you "drive for dollars" around town.

DealMachine has an app that is fast and easy to use. When you're driving around town and spot a home that could be a great deal (overgrown grass and shrubs, broken windows, vacant, etc), you just pull up the app to view the homeowner's contact information, and call them to see if they're interested in selling.

You can also send the owner direct mail (postcards) through the app for huge time savings (no post office visits required!). ⚡ Sign up for a 7-day free trial and test it out

How to finance a house hack

Buying a house for yourself or to house hack is essentially the same. For the most part, if you’re using a government-backed loan, you only need for the home to be your primary residence.

| Loan type | Down payment | Minimum credit score | Other fees |

|---|---|---|---|

| Conventional | 5–20% | 620 | PMI if less than 20% down |

| HomeReady | 3% | 680 | PMI |

| Home Possible | 3–5% | 660 | PMI |

| FHA loans | 3.5–10% | 580 | PMI |

| VA loan | $0 | 580 | 1.25–2.4% |

| USDA loan | $0 | Varies | 1% |

Conventional loans

A traditional loan from a bank or mortgage lender works best for home buyers with an average credit history, who can afford the same interest rate for the entire loan duration. Most lenders require a 20% down payment but will accept less if you pay private mortgage insurance.

If you’re planning on investing in real estate, conventional loans could give you the flexibility to start with one house and then expand to other properties.

HomeReady (Fannie Mae)

HomeReady loans are designed for low-income households to start house hacking. Some of the lowest down payment requirements on the market make HomeReady perfect for getting into homeownership. You still need average credit, though.

Some additional perks:

- Flexible down payment sources, including from other grants and projected rental income

- Extra $2,500 for very low-income borrowers toward down payment or closing costs

- Reduced mortgage insurance rates

Home Possible (Freddie Mac)

Home Possible loans can be great for lower-income households who want to house hack once — but not necessarily pursue a bigger real estate investment portfolio. That’s because borrowers can own two properties, with a max of four units.

» Learn more about Fannie Mae and Freddie Mac loans

FHA loans

FHA loans are best for borrowers with a poor credit history and relatively low debt, including first-time buyers and seniors. Because you’re putting down only 3.5%, you have to pay mortgage insurance premiums, so make sure you have enough income to cover your monthly payments.

An FHA loan could be a good way to finance a house hack — though probably not for medium-term real estate investing. That’s because you have to live in your home for three years, so you wouldn’t be able to move onto a new house hacking venture as soon as the first one becomes profitable.

Note: FHA mortgages have varying requirements depending on the household size, regardless of whether all members are on the mortgage. Having boarders in a single-family house can maximize the benefits of an FHA loan: their rent payments will help cover the mortgage, providing flexibility in the type of house you can buy and manage.

FHA Section 203(k)

Section 203(k) is a rehab loan. If you buy or refinance a house that’s at least a year old, you can renovate it and, get paid back by the FHA, then let out the remaining units. Rehabilitation projects might include:

- Repairing major structural issues (e.g., roof, foundation, HVAC)

- Making changes for improved functions and modernization.

- Updating large appliances

- Adding accessible features

You can also add or convert a garage, which can then be used for rental income.

VA loans and NADL (Native American Direct Loans)

You'll likely get more competitive interest rates if you’re a veteran, active duty service member, or married to one.

That, plus a $0 down payment requirement makes VA loans great options for taking on house hacking. You have to pay a one-time funding fee instead of a monthly PMI, which is a worthwhile price for a relatively small investment.

Your first step to applying for a VA loan is to get a Certificate of Eligibility (COE).

USDA loan

The typical USDA loan for single-family home buyers may not work for house hacking since it prohibits earning income from renting. Connect with a mortgage loan officer in your area to see if these rules apply.

Related reading