🏆 Where is the most affordable place to live in the U.S.? 🏆

Toledo, Ohio, is America’s most affordable city, with modestly priced homes and rental properties that are easily paid for with the area’s comfortable salaries. It’s one of three Buckeye State metros in the top 15, making Ohio the most affordable state overall.

Most Affordable U.S. Cities, Ranked | 15 Most Affordable Places to Live in the U.S. | America’s Most Affordable State | 10 Least Affordable American Cities | Rankings by Category | Methodology | FAQs

There’s no shortage of things on the wishlists of those searching for a new home, whether they’re buying or renting. Some look for extensive square footage and extra bedrooms, while others crave open-floor plans, natural light, and high-end kitchens. No matter what they want, there’s one thing every household needs: a price they can afford.

That’s become a higher hurdle than ever before in many U.S. cities, with inflation and a post-pandemic real estate boom pushing up home prices and rents far outside markets known for expensive housing costs, such as New York City and San Francisco.

Nationwide, rent prices have spiked by a third from pre-pandemic levels, while the cost to purchase a home is up at least 50% in many markets over the same period.

However, the prospect of owning a home or renting one affordably is more than just a dream for residents in many Midwest and mid-South cities. Our analysis found that Ohio stood out in particular, with Toledo taking the top spot for the most affordable city in the U.S. Akron came in fourth place, and Cleveland came in 15th.

On the flip side, Californians face the grimmest affordability challenges, with the Golden State earning six spots among the 10 least affordable cities in the U.S.

To determine our rankings, Clever analyzed data on 100 of the largest metros in the country, looking at factors such as typical home and rent prices, median income, insurance and property tax rates, energy costs, and more. We also zeroed in on the most affordable ZIP codes within each market, providing flexible buyers and renters a roadmap to their affordable future homes.

Read on to learn more about where budget-focused buyers and renters can find inexpensive places to call home.

💸 Most Affordable Places to Live in the U.S. Statistics

- The Midwest is home to three of the top five most affordable cities, but the South takes seven of the top 15 spots in our ranking.

- Pittsburgh and Scranton, Pennsylvania, are the only Northeast cities in the top 15.

- None of the top 15 most affordable places to live in the U.S. are located in the West. No. 44 Albuquerque, New Mexico, is the most affordable Western city.

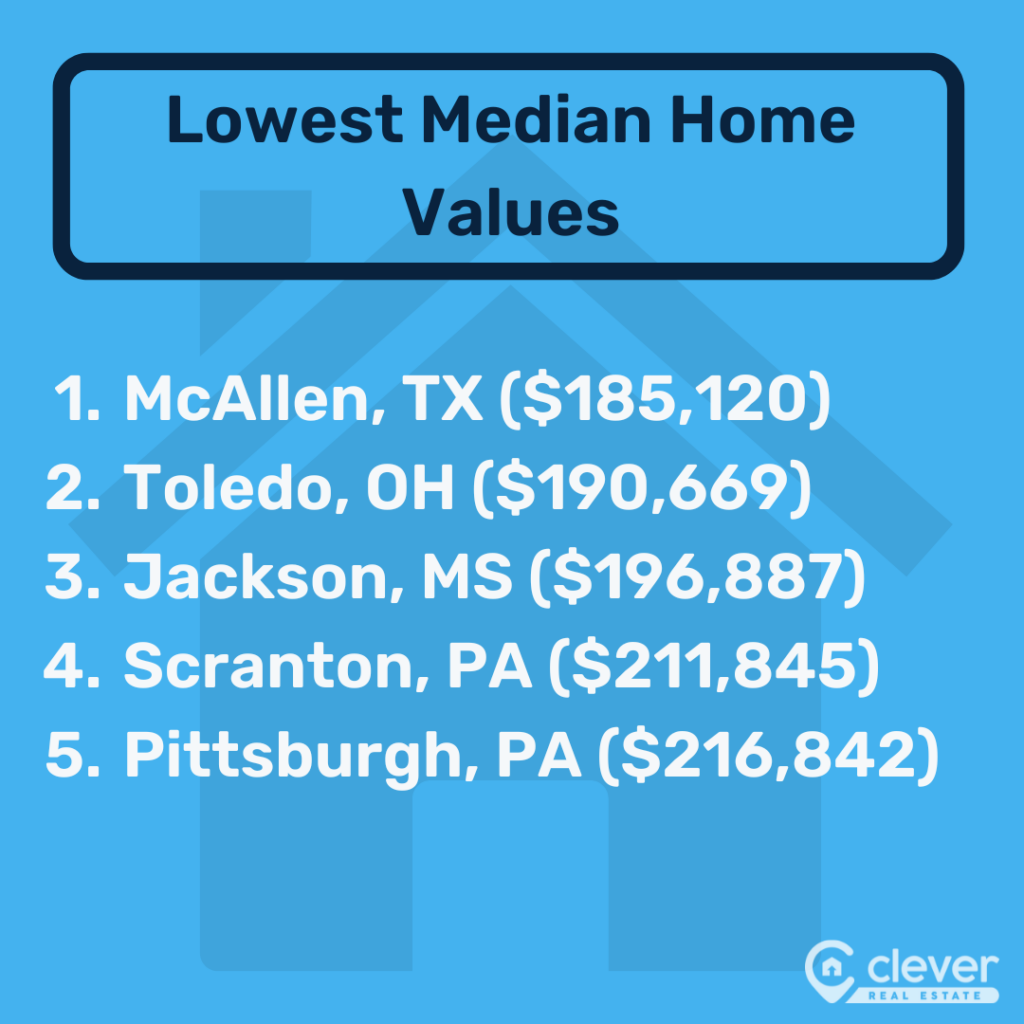

- McAllen, Texas, offers the cheapest typical home value at $185,120.

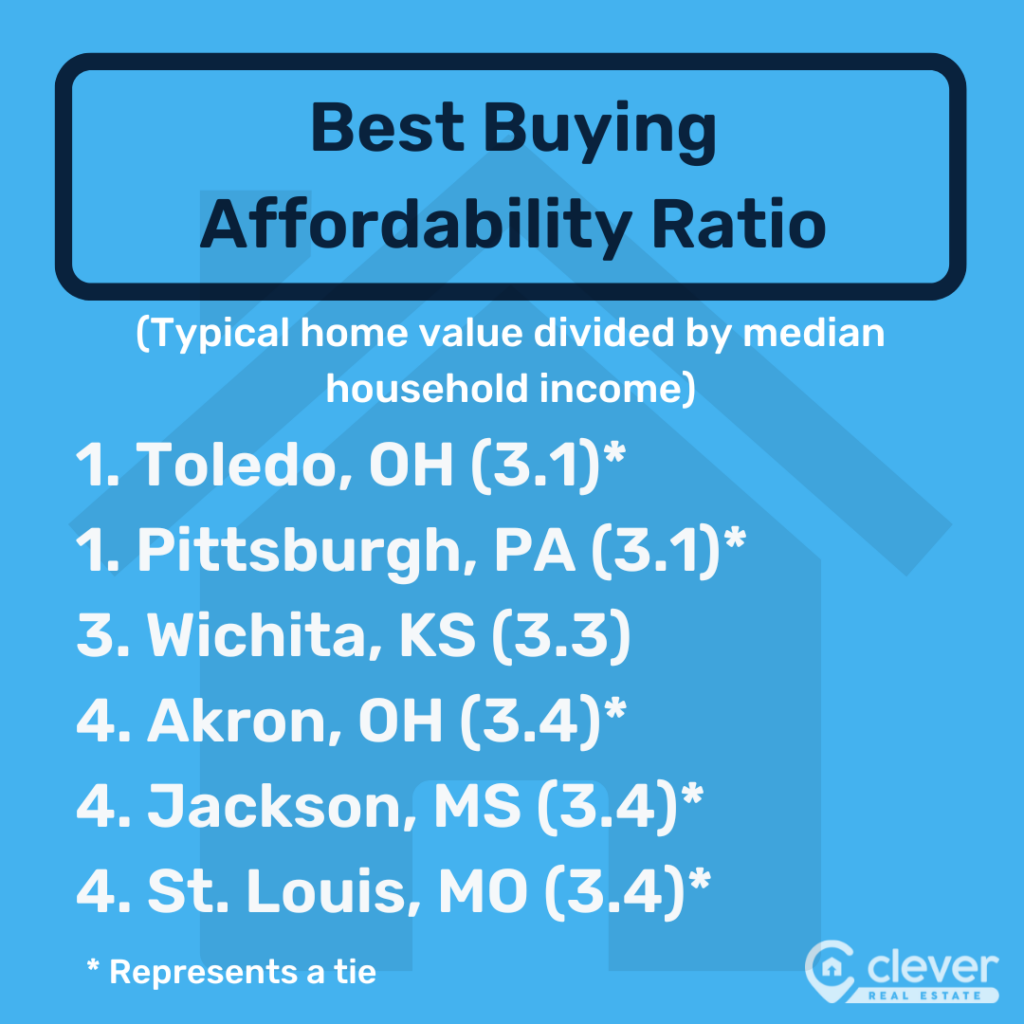

- When factoring in salaries, the most affordable homes can be bought in Toledo, Ohio, and Pittsburgh, where typical properties are valued at 3.1x the median household income.

- The most budget-friendly rentals can be found in Wichita, Kansas, where renters enjoy a typical monthly rent of $1,120.

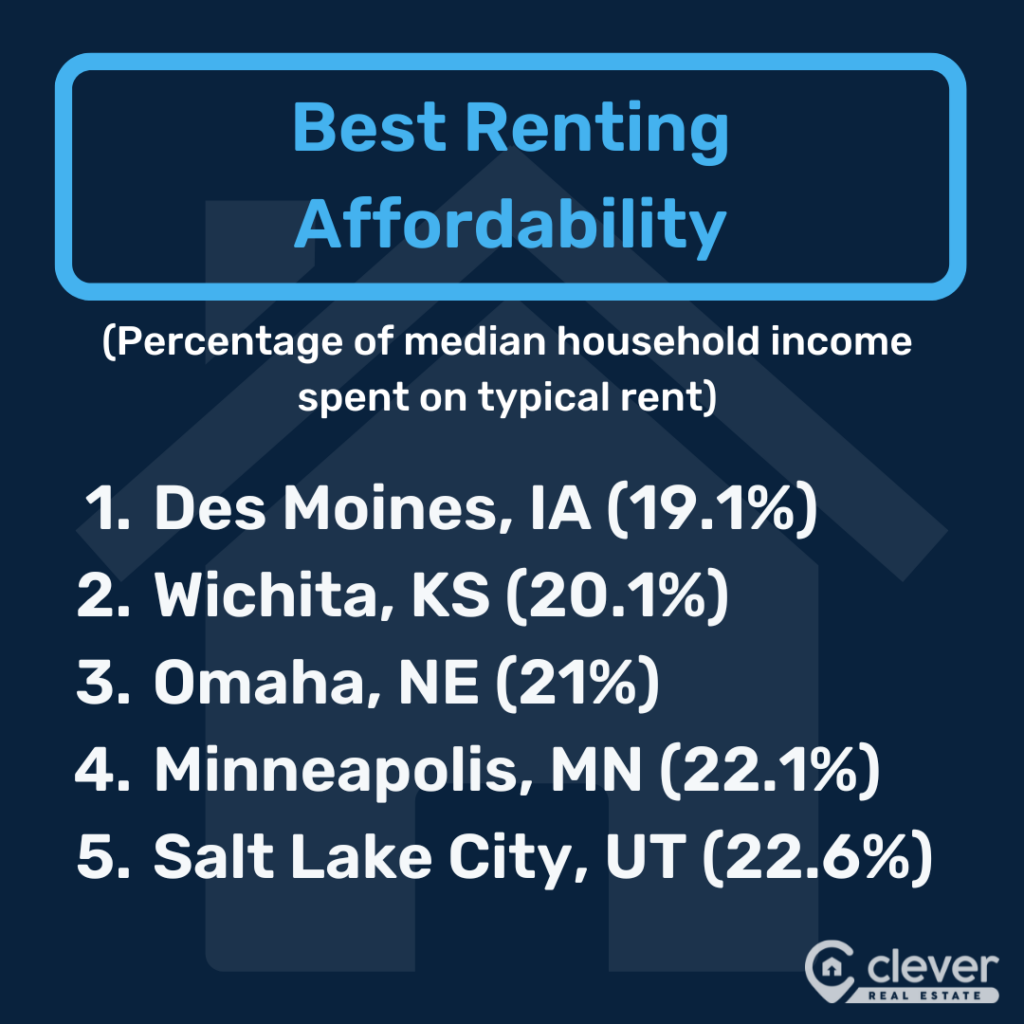

- As a percentage of income, the best rental deals are located in Des Moines, Iowa. Renters there pay 19.1% of the area’s typical wages for an average property.

- The country’s most expensive rentals are located in New York City with a typical rent of $3,493.

- Of the top 15 most affordable metro areas, only Des Moines has a median household income ($80,061) in the top half of the 100 cities studied (No. 38 overall).

- Property tax rates are lowest in Honolulu (0.32%), but Birmingham, Alabama, residents pay the least in taxes for a typical home ($1,022 annually).

- Owners of an average Toledo property have the cheapest home insurance bill ($837 per year), although Portland, Oregon, has the cheapest homeowners insurance rates ($1,012 annually on a $300,000 home).

- Seattle offers residents the most affordable electricity, with an average of $0.14 per kilowatt hour.

- Gas is cheapest in Tulsa, Oklahoma, where drivers can save just over 20% per gallon compared to the national average.

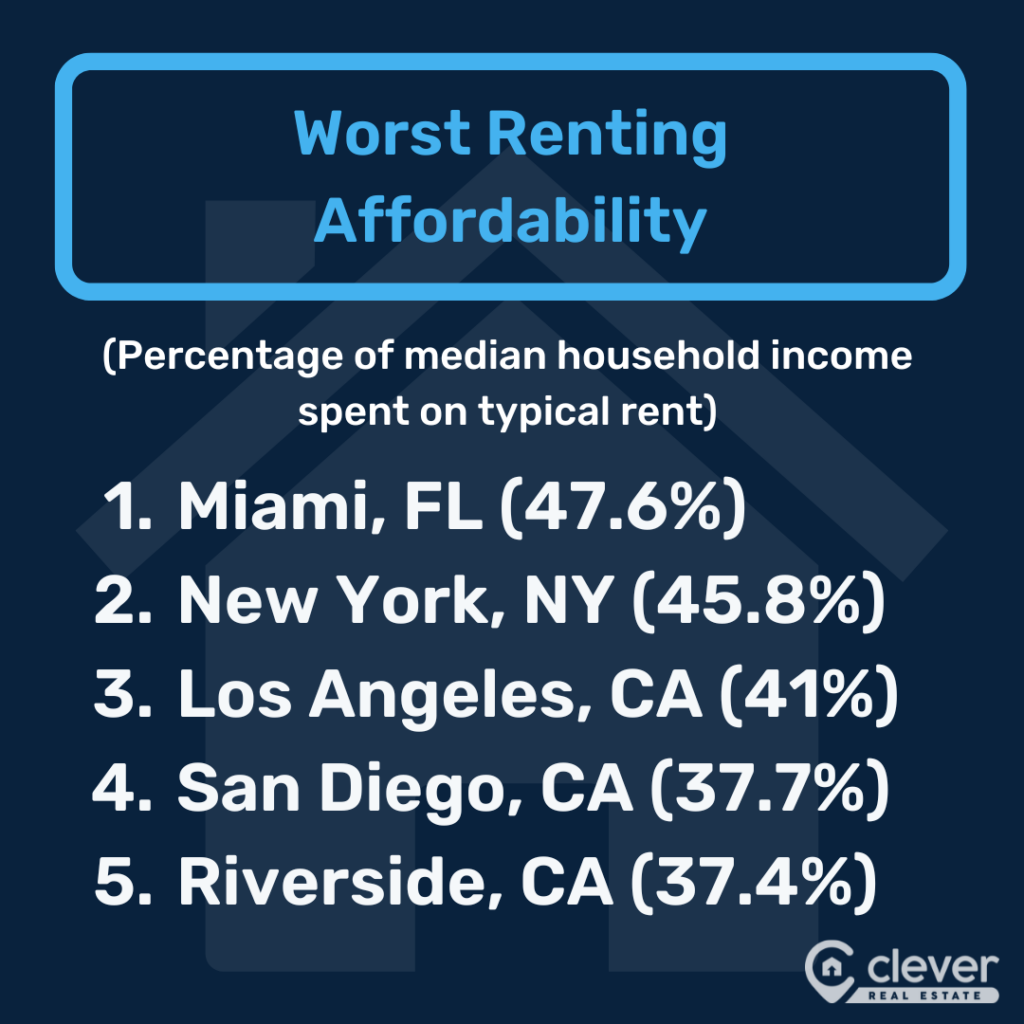

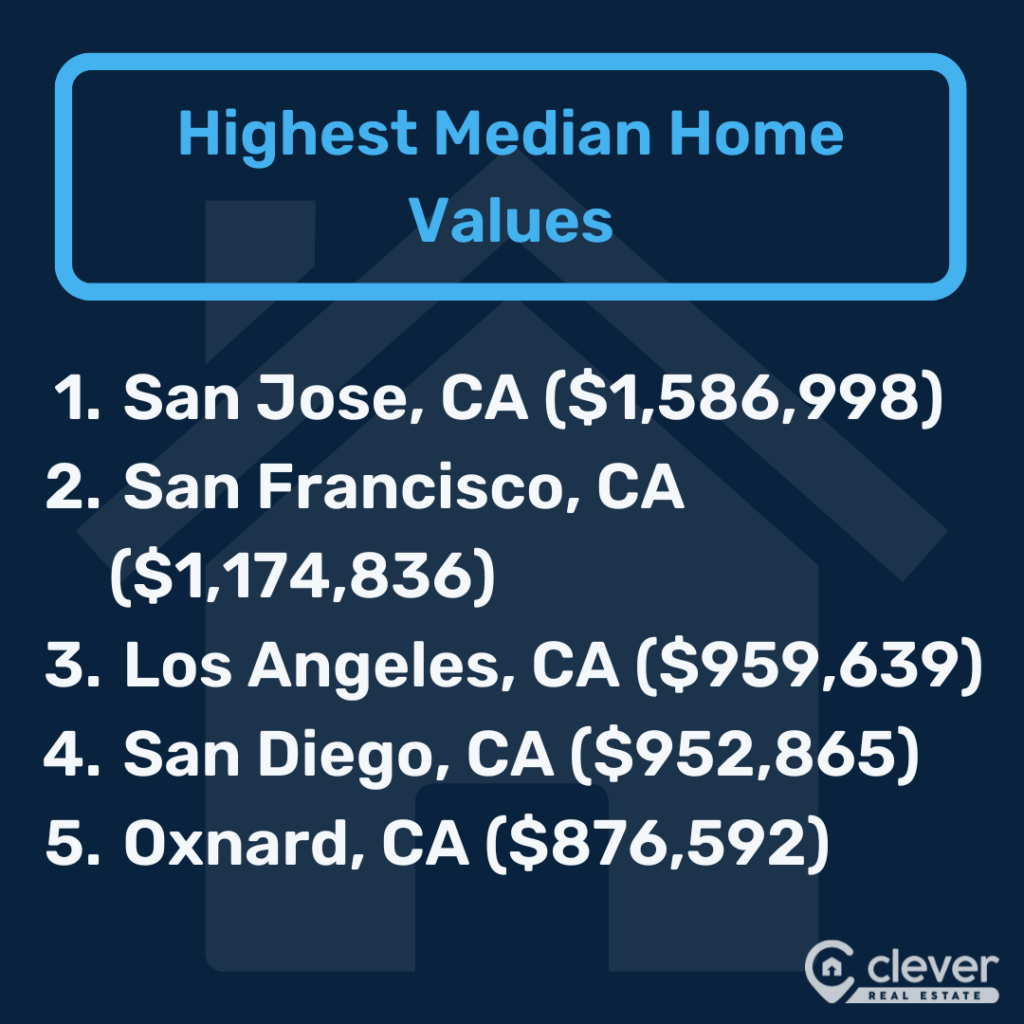

- Six of the 10 least affordable markets are, unsurprisingly, in California: San Diego, Los Angeles, Oxnard, Riverside, San Francisco, and San Jose.

The Most Affordable Cities in the U.S., Ranked

| Rank | City | Typical Home Value | Home Buying Affordability Ratio* | Monthly House Payment** | Typical Rent | Rent Affordability Ratio*** | Property Tax Rate**** |

| 1 | Toledo, OH | $190,669 | 3.1 | $1,286 | $1,242 | 24.4% | 1.59% |

| 2 | Wichita, KS | $218,458 | 3.3 | $1,595 | $1,120 | 20.1% | 1.34% |

| 3 | Little Rock, AR | $222,138 | 3.6 | $1,416 | $1,229 | 24.2% | 0.64% |

| 4 | Akron, OH | $223,354 | 3.4 | $1,506 | $1,283 | 23.1% | 1.59% |

| 5 | Pittsburgh, PA | $216,842 | 3.1 | $1,437 | $1,455 | 24.7% | 1.49% |

| 6 | St. Louis, MO | $255,196 | 3.4 | $1,652 | $1,420 | 22.9% | 1.01% |

| 7 | Scranton, PA | $211,845 | 3.5 | $1,404 | $1,300 | 25.8% | 1.49% |

| 8 | Des Moines, IA | $285,680 | 3.6 | $1,971 | $1,274 | 19.1% | 1.52% |

| 9 | Oklahoma City, OK | $237,118 | 3.6 | $1,693 | $1,366 | 24.7% | 0.89% |

| 10 | Jackson, MS | $196,887 | 3.4 | $1,259 | $1,473 | 30.5% | 0.67% |

| 11 | Baton Rouge, LA | $240,418 | 3.7 | $1,614 | $1,387 | 25.9% | 0.56% |

| 12 | Birmingham, AL | $255,417 | 3.8 | $1,570 | $1,420 | 25.3% | 0.40% |

| 13 | Augusta, GA | $235,671 | 3.6 | $1,500 | $1,434 | 26.7% | 0.92% |

| 14 | Louisville, KY | $260,835 | 3.8 | $1,730 | $1,406 | 24.3% | 0.83% |

| 15 | Cleveland, OH | $233,535 | 3.6 | $1,575 | $1,455 | 26.8% | 1.59% |

| 16 | Harrisburg, PA | $286,578 | 3.9 | $1,899 | $1,415 | 23.0% | 1.49% |

| 17 | Tulsa, OK | $238,126 | 3.8 | $1,700 | $1,384 | 26.2% | 0.89% |

| 18 | McAllen, TX | $185,120 | 3.8 | $1,395 | $1,187 | 29.0% | 1.68% |

| 19 | Detroit, MI | $256,071 | 3.6 | $1,719 | $1,489 | 25.1% | 1.38% |

| 20 | Omaha, NE | $293,908 | 3.7 | $2,346 | $1,392 | 21.0% | 1.63% |

| 21 | Memphis, TN | $242,228 | 3.8 | $1,514 | $1,496 | 28.0% | 0.67% |

| 22 | Buffalo, NY | $267,158 | 3.9 | $1,790 | $1,376 | 24.0% | 1.40% |

| 23 | Kansas City, MO | $307,503 | 4.1 | $1,990 | $1,491 | 23.8% | 1.01% |

| 24 | Indianapolis, IN | $283,596 | 3.7 | $1,765 | $1,582 | 25.0% | 0.84% |

| 25 | Syracuse, NY | $237,522 | 3.5 | $1,591 | $1,566 | 27.5% | 1.40% |

| 26 | Cincinnati, OH | $288,938 | 3.8 | $1,948 | $1,547 | 24.7% | 1.59% |

| 27 | Rochester, NY | $257,786 | 3.7 | $1,727 | $1,510 | 26.0% | 1.40% |

| 28 | Columbia, SC | $252,535 | 4.0 | $1,561 | $1,563 | 29.3% | 0.57% |

| 29 | San Antonio, TX | $288,945 | 4.1 | $2,177 | $1,505 | 25.6% | 1.68% |

| 30 | New Orleans, LA | $246,685 | 4.0 | $1,656 | $1,681 | 32.7% | 0.56% |

| 31 | Columbus, OH | $316,666 | 4.2 | $2,135 | $1,568 | 24.8% | 1.59% |

| 31 | Milwaukee, WI | $351,351 | 5.0 | $2,360 | $1,397 | 23.6% | 1.61% |

| 33 | Greensboro, NC | $258,343 | 4.3 | $1,662 | $1,514 | 30.1% | 0.82% |

| 34 | Albany, NY | $337,365 | 4.2 | $2,260 | $1,610 | 23.9% | 1.40% |

| 35 | Greenville, SC | $299,935 | 4.6 | $1,854 | $1,566 | 28.6% | 0.57% |

| 36 | Minneapolis, MN | $378,329 | 4.1 | $2,525 | $1,682 | 22.1% | 1.11% |

| 37 | Grand Rapids, MI | $329,362 | 4.2 | $2,210 | $1,623 | 25.0% | 1.38% |

| 38 | El Paso, TX | $219,166 | 4.1 | $1,651 | $1,589 | 35.7% | 1.68% |

| 39 | Chattanooga, TN | $309,878 | 4.5 | $1,937 | $1,619 | 28.1% | 0.67% |

| 40 | Winston, NC | $271,396 | 4.4 | $1,746 | $1,622 | 31.6% | 0.82% |

| 41 | Richmond, VA | $373,135 | 4.6 | $2,315 | $1,692 | 24.9% | 0.87% |

| 42 | Fayetteville, AR | $342,107 | 4.7 | $2,180 | $1,613 | 26.4% | 0.64% |

| 43 | Houston, TX | $311,325 | 4.2 | $2,346 | $1,746 | 28.0% | 1.68% |

| 44 | Albuquerque, NM | $338,188 | 5.1 | $2,088 | $1,606 | 29.0% | 0.67% |

| 45 | Virginia Beach, VA | $353,274 | 4.7 | $2,192 | $1,794 | 28.9% | 0.87% |

| 46 | Allentown, PA | $336,044 | 4.4 | $2,227 | $1,796 | 28.3% | 1.49% |

| 47 | Baltimore, MD | $388,642 | 4.3 | $2,469 | $1,902 | 25.2% | 1.05% |

| 48 | Madison, WI | $419,350 | 5.0 | $2,816 | $1,650 | 23.8% | 1.61% |

| 49 | Tucson, AZ | $353,339 | 5.5 | $2,173 | $1,598 | 30.0% | 0.63% |

| 50 | Philadelphia, PA | $365,902 | 4.3 | $2,425 | $1,885 | 26.9% | 1.49% |

| - | National Average | $362,481 | 4.8 | $2,373 | $2,070 | 33.2% | 1.04% |

| 51 | Ogden, UT | $496,131 | 5.4 | $2,913 | $1,764 | 22.9% | 0.57% |

| 52 | Raleigh, NC | $447,526 | 4.8 | $2,879 | $1,797 | 23.3% | 0.82% |

| 53 | Jacksonville, FL | $361,704 | 4.7 | $2,657 | $1,769 | 27.4% | 0.91% |

| 54 | Chicago, IL | $327,899 | 4.0 | $2,433 | $2,106 | 30.5% | 2.08% |

| 55 | Salt Lake City, UT | $546,393 | 5.9 | $3,209 | $1,731 | 22.6% | 0.57% |

| 56 | Austin, TX | $460,832 | 4.9 | $3,472 | $1,828 | 23.2% | 1.68% |

| 57 | Knoxville, TN | $348,441 | 5.1 | $2,178 | $1,832 | 32.4% | 0.67% |

| 58 | Dallas, TX | $378,841 | 4.6 | $2,854 | $1,838 | 26.6% | 1.68% |

| 59 | Hartford, CT | $367,701 | 4.3 | $2,579 | $1,909 | 26.7% | 1.79% |

| 60 | Spokane, WA | $417,914 | 6.1 | $2,573 | $1,536 | 26.8% | 0.87% |

| 61 | Provo, UT | $530,973 | 5.5 | $3,118 | $1,896 | 23.8% | 0.57% |

| 62 | Charlotte, NC | $386,254 | 5.0 | $2,485 | $1,817 | 28.3% | 0.82% |

| 63 | Durham, NC | $418,245 | 5.3 | $2,690 | $1,749 | 26.5% | 0.82% |

| 64 | Atlanta, GA | $387,508 | 4.6 | $2,466 | $1,950 | 27.6% | 0.92% |

| 65 | Bakersfield, CA | $356,453 | 5.4 | $2,168 | $1,839 | 33.3% | 0.75% |

| 66 | Springfield, MA | $354,899 | 5.2 | $2,290 | $1,846 | 32.4% | 1.14% |

| 67 | Lakeland, FL | $316,553 | 5.1 | $2,325 | $1,925 | 37.2% | 0.91% |

| 68 | Palm Bay, FL | $357,134 | 4.7 | $2,624 | $1,995 | 31.8% | 0.91% |

| 69 | Las Vegas, NV | $433,042 | 6.1 | $2,537 | $1,820 | 30.9% | 0.59% |

| 70 | Deltona, FL | $347,327 | 5.3 | $2,551 | $1,933 | 35.2% | 0.91% |

| 71 | Washington DC | $567,683 | 4.8 | $3,378 | $2,479 | 25.3% | 0.62% |

| 72 | Boise City, ID | $480,565 | 5.9 | $2,867 | $1,835 | 27.2% | 0.67% |

| 73 | Phoenix, AZ | $459,067 | 5.5 | $2,823 | $1,884 | 27.3% | 0.63% |

| 74 | Colorado Springs, CO | $464,486 | 5.7 | $2,972 | $1,905 | 27.9% | 0.55% |

| 75 | Nashville, TN | $445,517 | 5.6 | $2,785 | $1,951 | 29.2% | 0.67% |

| 76 | New Haven, CT | $375,358 | 4.6 | $2,633 | $2,082 | 30.5% | 1.79% |

| 77 | Portland, OR | $553,245 | 6.2 | $3,380 | $1,895 | 25.5% | 0.93% |

| 78 | Fresno, CA | $398,650 | 5.7 | $2,424 | $2,016 | 34.8% | 0.75% |

| 79 | Denver, CO | $589,914 | 6.0 | $3,774 | $2,096 | 25.4% | 0.55% |

| 80 | Charleston, SC | $440,517 | 5.6 | $2,723 | $2,077 | 31.6% | 0.57% |

| 81 | Tampa, FL | $382,195 | 5.5 | $2,808 | $2,125 | 36.8% | 0.91% |

| 82 | Cape Coral, FL | $391,020 | 5.5 | $2,872 | $2,129 | 35.9% | 0.91% |

| 83 | Orlando, FL | $400,221 | 5.6 | $2,940 | $2,097 | 35.0% | 0.91% |

| 84 | Worcester, MA | $461,007 | 5.5 | $2,975 | $2,124 | 30.4% | 1.14% |

| 85 | Seattle, WA | $746,560 | 7.0 | $4,597 | $2,310 | 25.9% | 0.87% |

| 86 | Stockton, CA | $543,505 | 6.3 | $3,305 | $2,445 | 34.1% | 0.75% |

| 87 | Sacramento, CA | $587,125 | 6.6 | $3,570 | $2,337 | 31.4% | 0.75% |

| 88 | North Port, FL | $449,055 | 5.9 | $3,299 | $2,350 | 37.3% | 0.91% |

| 89 | Providence, RI | $490,045 | 6.0 | $3,328 | $2,121 | 31.1% | 1.40% |

| 90 | Honolulu, HI | $870,792 | 9.0 | $4,919 | $2,802 | 34.8% | 0.32% |

| 91 | San Jose, CA | $1,586,998 | 10.7 | $9,650 | $3,474 | 28.0% | 0.75% |

| 92 | San Francisco, CA | $1,174,836 | 9.2 | $7,144 | $3,132 | 29.3% | 0.75% |

| 93 | Bridgeport, CT | $630,873 | 6.0 | $4,426 | $2,945 | 33.3% | 1.79% |

| 94 | Riverside, CA | $586,780 | 7.1 | $3,568 | $2,583 | 37.4% | 0.75% |

| 95 | Miami, FL | $492,318 | 7.0 | $3,617 | $2,806 | 47.6% | 0.91% |

| 96 | Boston, MA | $705,496 | 6.8 | $4,553 | $3,101 | 35.7% | 1.14% |

| 97 | Oxnard, CA | $876,592 | 8.5 | $5,330 | $3,111 | 36.4% | 0.75% |

| 98 | New York, NY | $672,129 | 7.3 | $4,503 | $3,493 | 45.8% | 1.40% |

| 99 | Los Angeles, CA | $959,639 | 10.9 | $5,835 | $3,001 | 41.0% | 0.75% |

| 100 | San Diego, CA | $952,865 | 9.6 | $5,794 | $3,106 | 37.7% | 0.75% |

**Payment factors in principal and interest on a 30-year mortgage at a 6.49% interest rate with a 20% down payment, as well as typical property taxes and insurance for the market.

***Determined by dividing average annual rent by median household income.

****Statewide average effective rate.

The 15 Most Affordable Cities in the US

1. Toledo, OH

| Typical Home Price: $190,669 (No. 99) Typical Rent: $1,242 (No. 97) Median Household Income: $61,012 (No. 94) |

America’s most affordable place to live is the northwestern Ohio city of Toledo, located along the western shores of Lake Erie and home to just over a quarter-million residents.

When it comes to homebuying affordability, Toledo tied for first place with a ratio of 3.1. That’s more than a third lower (36%) than the national average of 4.8.

Toledo earns that honor, in part, by having the second-lowest median home price of the 100 markets studied. The typical home value in Toledo is $190,669, barely half the typical home value nationwide ($362,481)

Moderate homeowners insurance costs also contribute to Toledo’s high ranking. It has the lowest average annual spending on premiums of any city at $837, thanks to low housing prices. That's less than a third of the annual homeowners insurance premium on the typical home nationwide, which clocks in at $2,743.

In addition, property taxes in Toledo are about 19% lower than the national average.

Toledo is also a great place for budget-focused renters. Factoring in units of all sizes, the typical monthly rent in Toledo is $1,242 — 40% lower than nationwide ($2,070). That’s the fourth-lowest price in the country. Meanwhile, when it comes to rent as a proportion of income, Toledo is more than a quarter (26%) lower than the national level.

Most Affordable ZIP Code in the Metro Area: Toledo, OH (43613)

» Learn more about the most affordable places to live in Ohio.

2. Wichita, KS

| Typical Home Price: $218,458 (No. 95) Typical Rent: $1,120 (No. 100) Median Household Income: $67,012 (No. 77) |

Known as the “Air Capital of the World” for its long-running role in the design and production of aircraft, Wichita’s cost of living is decidedly more grounded. Close behind Toledo overall, Wichita boasts the second best rent-to-income ratio of 20.1%, which is a result of the lowest typical monthly rent of any market studied ($1,120). That’s barely half the national average cost.

Home buyers will also find the area is home to the third-best home purchase affordability, with the value of a typical property just 3.3x the median household income. The country as a whole has an affordability ratio of 4.8.

The median home value in Wichita is only $218,458 — 40% lower than the typical U.S. home value of $362,481. That’s the sixth-most affordable price in the U.S.

Meanwhile, property taxes on the average Wichita home ($2,927) are 22% lower than the cost for a typical home nationwide, representing nearly $70 per month in savings.

Wichita also offers affordability benefits beyond just housing. Prices for electricity are the 10th lowest in the country ($0.15 per kilowatt hour), and gas prices are also 9% below the national average.

Most Affordable ZIP Code in the Metro Area: Newton, KS (67114)

» Learn more about the most affordable places to live in Kansas.

3. Little Rock, AR

| Typical Home Price: $222,138 (No. 93) Typical Rent: $1,229 (No. 98) Median Household Income: $60,931 (No. 95) |

Rounding out a tight top three is Arkansas’ capital and largest city, Little Rock. Monthly rent in the city is 40% below the national average at just $1,229, the third-lowest of the 100 cities studied.

Home values are also more affordable by a similar 39%, with a median property value of $222,138, the eighth-cheapest price in the country. The metro area has stayed relatively budget-friendly, even in the face of steep price growth in most parts of the country. Little Rock property values grew 28% less than the typical market over the past five years.

Arkansas also stands out for its low property taxes, with a typical Little Rock homeowner paying $1,422, which is the fifth-lowest rate in the country. That’s barely a third of the national median of $3,758.

In addition, both energy prices per kilowatt hour and gas prices per gallon are cheaper than the national average by 10% and 9%, respectively.

Most Affordable ZIP Code in the Metro Area: North Little Rock, AR (72116)

» Learn more about the most affordable places to live in Arkansas.

4. Akron, OH

| Typical Home Price: $223,354 (No. 92) Typical Rent: $1,283 (No. 95) Median Household Income: $66,652 (No. 78) |

Akron may be best known these days as the home of basketball megastar LeBron James, but the one-time “Rubber Capital of the World” is also noteworthy for its affordable homes. Akron is tied for the third-best home-buying affordability ratio, with typical homes in the city valued at 3.4x the median household income.

This is partly due to the state’s low insurance costs, with the average homeowner spending $981 in annual premiums, the fourth-lowest amount nationally.

Renters also enjoy the sixth-lowest monthly rent ($1,283). Compared to the national median of $2,070, that saves Akron renters $9,444 per year. When factoring in local salaries, Akron’s rent affordability ratio is 30% better than the country as a whole.

Most Affordable ZIP Code in the Metro Area: Ravenna, OH (44266)

5. Pittsburgh, PA

| Typical Home Price: $216,842 (No. 96) Typical Rent: $1,455 (No. 82) Median Household Income: $70,607 (No. 64) |

Pittsburgh isn’t just a great city for real estate agents. Home buyers, in particular, should also look to the Steel City for an affordable place of their own. It shares the top spot for home affordability with No. 1 Akron.

Typical Pittsburgh home values are just 3.1x the median household income, with an average property valued at a modest $216,842. That’s 40% lower than the national median home value ($362,481).

Housing in Pittsburgh is poised to potentially get even more affordable, with Zillow forecasting a 1.7% decline in home values over the next year.

Annual homeowners insurance premiums in the Pittsburgh metro sit at a median of $869, an eye-popping 68% lower than the national median of $2,743. That’s the third-most affordable overall. Property taxes on the typical home in Pittsburgh are 14% lower than the property taxes on the typical home nationwide.

Renters see benefits, too, with the monthly rent price ($1,455) in Pittsburgh, 30% lower than the U.S. average ($2,070).

Most Affordable ZIP Code in the Metro Area: New Brighton, PA (15066)

» Learn more about the most affordable places to live in Pennsylvania.

6. St. Louis, MO

| Typical Home Price: $255,196 (No. 82) Typical Rent: $1,420 (No. 84) Median Household Income: $74,531 (No. 55) |

Relatively strong salaries and modest costs to buy or rent a home help power “The Gateway to the West” to a top-10 spot. The average St. Louis home costs 3.4x the area’s median household income — tied for third best in the country — while rent takes up an average of 22.9% of residents’ budgets — the seventh lowest.

Typical home values in St. Louis ($255,196) are more than $100,000 under the national median ($362,481), while monthly rent averages $1,420. Both are roughly a third lower than the national average.

Annual property taxes ($2,577) and homeowners insurance premiums ($1,773) on a typical home are also around a third less than average. Meanwhile, St. Louis drivers save a few bucks on gas, too, with local prices per gallon roughly 10% lower than the national cost.

Most Affordable ZIP Code in the Metro Area: Alton, IL (62002)

» Learn more about the most affordable places to live in Missouri.

7. Scranton, PA

| Typical Home Price: $211,845 (No. 97) Typical Rent: $1,300 (No. 94) Median Household Income: $60,537 (No. 96) |

Finding an affordable home within a day trip’s distance from New York City and Philadelphia might seem improbable, but it’s a reality in Scranton.

A typical residential property in Pennsylvania’s Electric City — no office parks or beet farms included — is 42% cheaper than the national median, priced at $211,845. That’s the fourth-lowest in the country.

These affordable prices, combined with lower-than-average insurance rates, give Scranton the second-lowest average annual homeowners insurance bill at $849 per year. Property taxes on the typical home ($3,156) are also 16% lower than the national average ($3,758).

Renters can also save a few bucks in Scranton, where the typical rent of $1,300 is the country’s seventh-lowest. As a proportion of their income, an average renting household pays 25.8%, substantially lower than the national level of 33.2%.

Most Affordable ZIP Code in the Metro Area: Carbondale, PA (18407)

8. Des Moines, IA

| Typical Home Price: $285,680 (No. 73) Typical Rent: $1,274 (No. 96) Median Household Income: $80,061 (No. 38) |

Few think of Iowa as an ideal spot for renters, but the numbers tell a different story. Des Moines offers the country’s best affordability for those who rent, with typical annual rent taking up just 19.1% of the median household income. On a nationwide basis, renters spend an average of 33.2%.

The city is able to offer this kind of affordability through strong salaries paired with the country’s fifth-lowest typical monthly rent ($1,274).

Home buyers won’t have to bust their budgets either, thanks to Des Moines’ ninth-best home affordability ratio. Typical homes are valued at roughly 3.6x the median household income. Although home prices have climbed 35% in the past five years, that’s still the 11th-lowest price among the 100 markets studied.

Residents of Iowa’s capital also enjoy the 10th-cheapest energy prices at $0.15 per kilowatt hour.

Most Affordable ZIP Code in the Metro Area: Des Moines, IA (50313)

» Learn more about the most affordable places to live in Iowa.

9. Oklahoma City, OK

| Typical Home Price: $237,118 (No. 89) Typical Rent: $1,366 (No. 93) Median Household Income: $66,301 (No. 80) |

Oklahoma City is another ideal spot for renters, who can reap the benefits of a 34% “discount” on monthly rent ($1,366) compared to the national average ($2,070). That’s the eighth-best price among the 100 markets studied.

Those buying a home will find a typical property costs 3.6x the city’s median household income, over a quarter (26%) more affordable than the country overall. Only eight markets offer better home affordability ratios.

Modest property taxes also help keep OKC affordable, with a typical home receiving a bill for $2,110, the 10th-lowest amount in the country and 44% lower than average.

In addition, Oklahoma’s energy industry may help keep gas prices low in the capital city, where drivers pay more than 20% less than the national average.

Most Affordable ZIP Code in the Metro Area: Chickasha, OK (73018)

» Learn more about the most affordable places to live in Oklahoma.

10. Jackson, MS

| Typical Home Price: $196,887 (No. 98) Typical Rent: $1,473 (No. 80) Median Household Income: $58,064 (No. 98) |

While many Americans are focused on the sticker price of a home, savvy buyers know the actual costs that matter are the principal, interest, taxes, and insurance (PITI) they must pay to own it. Jackson’s average PITI payment of $1,259 is the lowest of any market studied.

This central Mississippi city earns this distinction through the third-lowest home values of our 100 cities. The typical home is worth just $196,887, which is 46% lower than the national median home value of $362,481.

At the same time, Jackson's home prices have risen at the eighth-slowest rate (33%) of any market over the past five years, and homes are expected to decrease in value by 2.1% by mid-2025. The relatively cool housing market is a notable contrast to prices throughout the country, which are expected to rise by 0.9% over the same time period.

However, unlike some places with bargain-priced homes and slumping economies, Jackson residents earn reasonable salaries compared to the local cost of housing. Typical homes are valued at 3.4x the median household income, tied for the third-best ratio in the country.

Keeping the lights on is also cheap in Jackson, where a kilowatt hour of electricity costs the third-least of anywhere in the country ($0.15). In addition, getting to work is affordable thanks to the sixth-cheapest gas price, which is 13% lower than the national average.

Most Affordable ZIP Code in the Metro Area: Jackson, MS (39212)

» Learn more about the most affordable places to live in Mississippi.

11. Baton Rouge, LA

| Typical Home Price: $240,418 (No. 86) Typical Rent: $1,387 (No. 90) Median Household Income: $64,222 (No. 86) |

Despite soaring real estate prices across the country since 2019, Baton Rouge has avoided the worst of the affordability crisis, with home values rising at the second-lowest rate (23%) of any market over the past five years. Nationally, home values grew 49% over that period.

What’s more, the metro area is poised to get even more affordable over the next 12 months. Home values are expected to decline by 3%, the third-biggest drop of any market studied.

Typical homes are valued at $240,418, which is 34% lower than the national average and just 3.7x the median household income in the region. Rock-bottom property tax rates are a big help for Baton Rouge housing costs, with the 0.56% rate sitting at the fifth-lowest among our 100 markets. It’s barely half the national rate of 1.04%.

Meanwhile, the average rent in Baton Rouge is just $1,387 per month, 33% cheaper than the national average of $2,070. Residents also reap extra savings from gas prices and electricity costs ($0.16 per kilowatt hour) that are 10% less than the nation at large.

Most Affordable ZIP Code in the Metro Area: Baker, LA (70714)

» Learn more about the most affordable places to live in Louisiana.

12. Birmingham, AL

| Typical Home Price: $255,417 (No. 81) Typical Rent: $1,420 (No. 85) Median Household Income: $67,242 (No. 76) |

It might truly be a “Sweet Home Alabama” for buyers concerned about minimizing their spending on property taxes. In Birmingham, the country’s second-lowest rate (0.4%) combines with modestly priced housing (with a median value of $255,417) to produce the lowest typical property tax burden of $1,022 per year.

Like many other small- to medium-sized Southern cities, rent is also reasonable, with a typical monthly rent of $1,420. That’s $650 per month in savings compared to the national average of $2,070. This means residents spend just 25.3% of the median household income for a typical rental property.

Electricity prices are also the third-cheapest of our top 100 markets at $0.15 per kilowatt hour, a 17% discount from the national average rate.

Most Affordable ZIP Code in the Metro Area: Midfield, AL (35228)

» Learn more about the most affordable places to live in Alabama.

13. Augusta, GA

| Typical Home Price: $235,671 (No. 90) Typical Rent: $1,434 (No. 83) Median Household Income: $64,581 (No. 85) |

If finding a cheap place to buy is the top goal, the home of the legendary Masters golf tournament is among the best options. When taking into account principal, interest, taxes, and insurance on a typical residential property, Augusta boasts the country’s sixth-lowest PITI payment, estimated at $1,500 per month.

Average home values ($235,671) are the 11th lowest of the markets studied, while property taxes on a typical home are the 14th lowest ($2,168 annually). Augusta homeowners also save about $100 per month in insurance costs. The average premium is $1,544 annually, compared to $2,743 nationwide.

Rent is a bargain, too, with a typical monthly rent of $1,434, which is 31% cheaper than the national average. Meanwhile, Augusta provides a roughly 8% “discount” on gas compared to national prices.

Most Affordable ZIP Code in the Metro Area: Martinez, GA (30907)

» Learn more about the most affordable places to live in Georgia.

14. Louisville, KY

| Typical Home Price: $260,835 (No. 77) Typical Rent: $1,406 (No. 87) Median Household Income: $69,547 (No. 68) |

Although Louisville may not be a standout in any category in particular, it offers broad affordability for those who choose to put down roots in this vibrant, historic city just across the river from Indiana.

Average rent is the 14th lowest in the U.S. ($1,406), allowing typical residents to spend just 24.3% of their income on the average property.

Meanwhile, buyers will find typical home values ($260,835) that are roughly $100,000 less than the national average ($362,481), representing a 28% savings.

Kentucky’s property tax rate (0.83%) is also 20% cheaper than in the typical market (1.04%). In addition, energy prices are the third lowest in the country at $0.15 per kilowatt hour.

Most Affordable ZIP Code in the Metro Area: Louisville, KY (40214)

» Learn more about the most affordable places to live in Kentucky.

15. Cleveland, OH

| Typical Home Price: $233,535 (No. 91) Typical Rent: $1,455 (No. 81) Median Household Income: $65,198 (No. 84) |

Reasonably priced homes and rental properties seem to be a trend in Ohio, with Cleveland snagging the final spot in the top 15. The city features a typical home value of $233,535, about 3.6x the market’s median household income. In the average market, it’s 4.8. By this metric, Cleveland is the 11th-most affordable place to buy.

Modestly priced homes and relatively low homeowners insurance rates help keep the insurance bill at the country’s fifth-lowest level — $1,025 annually.

Meanwhile, average rent sits at $1,455, which is 30% lower than the national price of $2,070. This allows renters to spend just 26.8% of their incomes on rent — 19% less than average nationwide.

Most Affordable ZIP Code in the Metro Area: Brook Park, OH (44142)

America’s Most Affordable State: Ohio

There’s little doubt about which state offers the most affordable places to live in our rankings. Not only does Ohio earn the top spot (Toledo), but it’s also home to two cities in the top 15 (No. 4 Akron and No. 15 Cleveland) and two in the top third (No. 26 Cincinnati and Columbus, tied for No. 31).

Ohio's status as the most affordable state is primarily a result of modest home and rental costs, as well as reasonable median incomes and below-average homeowners insurance rates ($1,317 annually for a $300,000 property).

Pennsylvania, the Buckeye State’s neighbor to the east, is the second-most affordable state, with two cities in the top 10 (No. 5 Pittsburgh and No. 7 Scranton), alongside No. 16 Harrisburg, No. 46 Allentown, and No. 50 Philadelphia in the top half.

The commonwealth scored highly for similar reasons to Ohio: moderate home and rental prices, appropriate incomes, and even lower homeowners insurance rates ($1,202 per year for a $300,000 property).

Honorable mentions go to Oklahoma, with two cities in the top 20 (No. 9 Oklahoma City and No. 17 Tulsa), and Missouri, with two in the top 25 (No. 6 St. Louis and No. 23 Kansas City).

America’s 10 Least Affordable Cities

- San Diego, California

- Los Angeles, California

- New York City, New York

- Oxnard, California

- Boston, Massachusetts

- Miami, Florida

- Riverside, California

- Bridgeport, Connecticut

- San Francisco, California

- San Jose, California

The country’s most populated state offers plenty to residents: warm weather, gorgeous scenery, and a bustling economy. However, home affordability is certainly not among the benefits. California is home to six of the bottom 10 spots in our rankings. Only one California city, No. 65 Bakersfield, even made the top two-thirds of affordable markets.

Although residents often enjoy higher-than-average salaries, the cost of buying or renting a home is even more elevated. The Golden State's lack of affordable housing affects not only metropolises such as Los Angeles and San Francisco but also their suburbs and small cities such as Stockton, the 15th-least affordable market.

The Northeast is also home to three of the 10 most unaffordable cities: New York, Boston, and Bridgeport. Miami is the only city on the bottom 10 not located in that region or California.

The Least Affordable City in the U.S.: San Diego, CA

| Typical Home Price: $952,865 (No. 4) Typical Rent: $3,106 (No. 5) Median Household Income: $98,928 (No. 9) |

San Diego residents, in particular, feel the brunt of California’s unaffordable housing.

The city’s median home value is $952,865, with typical homes priced at roughly 9.6x the median household income. There are only three markets in the country where properties are more expensive. The situation has gotten comparatively worse, with values rising by 60% since 2019, outpacing the national increase of 49%.

It’s no better for renters, with an average monthly rent of $3,106, which is 50% higher than the national median.

In addition, utilities are sky high, with electricity priced at $0.42 per kilowatt hour, 2.3x the nationwide average price and the most expensive in the country. Gas is also the third-most expensive in the country, more than 26% pricier than the national average.

Rankings by Category

Methodology

We used the following weights when building our city ranking:

- Current typical home value (17%)

- Home affordability, determined by dividing the typical home price by the median household income (17%)

- Typical monthly rent (17%)

- Annual rent affordability, determined by dividing average annual rent by median household income (17%)

- Monthly principal, interest, taxes, and insurance payment with 20% down (8.5%)

- Monthly principal and interest payment with 20% down (6.4%)

- Home value increase, last five years (2.1%)

- Home value forecast, next 12 months (2.1%)

- Property tax rate (2.1%)

- Property tax on typical home value (2.1%)

- Annual insurance on a $300,000 home (2.1%)

- Annual insurance on a typical home (prorated) (2.1%)

- Fuel prices per gallon (2.1%)

- Energy prices per kilowatt hour (2.1%)

We combined these rankings to produce an overall ranking, which determined the most affordable city. For the most affordable ZIP code within each city, we evaluated typical home value, typical rent, home affordability ratio, and rent affordability ratio within that ZIP code with equal weight.

Sources for our data include Zillow, the U.S. Census, the American Community Survey, Bankrate, Rocket Mortgage, The Tax Foundation, Freddie Mac, and the Bureau of Labor Statistics.

About Clever

Since 2017, Clever Real Estate has been on a mission to make selling or buying a home easier and more affordable for everyone. Twelve million annual readers rely on Clever's library of educational content and data-driven research to make smarter real estate decisions—and to date, Clever has helped consumers save more than $160 million on realtor fees. Clever's research has been featured in The New York Times, Business Insider, Inman, Housing Wire, and many more.

More Research From Clever

Articles You May Like

FAQs

What is the cheapest state to live in?

Ohio is the country’s most affordable state. It's home to five markets in the top third of our rankings: No. 1 Toledo, No. 4 Akron, No. 15 Cleveland, No. 26 Cincinnati, and No. 31 Columbus. Learn more.

What city in America has the lowest cost of living?

America’s most affordable place to live is the northwestern Ohio city of Toledo, with typical homes just 3.1x the median household income. That’s more than a third lower (36%) than the national average of 4.8. Learn more.

Where are the least affordable cities in the U.S.?

The least affordable city in the country is San Diego, where the average home value is $952,865, roughly 9.6x the median household income. Typical renters pay $3,106 per month, which is 50% higher than the national median. Learn more.

Where are the most expensive homes in America?

San Jose, California, has the priciest homes for buyers, with a typical home value of $1,586,998. The highest rents are in New York City, with an average cost of $3,493 per month. Learn more.