Title insurance at a glance

-

What it is: A title insurance policy protects its owner against disputes over who legally owns a piece of property. If a clerical error surfaces in ownership records, or a previous owner left unpaid property taxes, the policy covers legal costs to defend your ownership claim in court or reimburses you for the value of your home.

-

Types: There are two types: (1) lender's title insurance, which protects the mortgage lender, and (2) owner's title insurance, which protects the homeowner.

-

Who pays: Buyers typically pay for the lender's policy, which is almost always required with a mortgage. Owner's policies are optional but usually a good idea. Who pays varies by state. In some, it's the buyer. In others, it's the seller.

-

What it costs: Both policies together typically add up to around 0.5% of the purchase price. This can range from a flat fee of a few hundred dollars to more than 1%, depending on your home's value and location.

How does title insurance protect you?

Title insurance protects you when someone brings a claim against your ownership that wasn't uncovered during the title search. Claims typically relate to public record errors, undisclosed liens, or illegal deeds (for example, if a previous owner wasn't legally eligible to hold title, such as a minor).

When someone files a claim against your title, your policy covers legal expenses to defend your ownership in court. It also reimburses you for financial losses up to the full purchase price of the home. A title insurance policy is essentially the title company placing a "bet" that it caught every possible issue during the title search.

📚 Key definitions

What is a property title?

A property title consists of many legal documents that specify who the rightful owner is. It's more than just a piece of paper that verifies your ownership (that's a document called the "deed"). A home's title includes a history of the chain of ownership and information about any liens (outstanding debts) on the property.

What do title companies do?

A title company verifies that the seller has a clear title to their home (i.e., the legal right to sell the property without any challenges to rightful ownership). Home buyers typically pay a title company for this service.

What is a title search?

A title company performs a title search to confirm the seller's ownership. During the search, the company reviews legal documents to identify anything that might prevent the seller from transferring ownership to the buyer.

Issues with the seller's ownership are commonly called "title defects" or "clouds on title." Title defects are more common than most people realize. Title professionals resolve issues in roughly one in four real estate transactions before closing.[1] If left unaddressed, a title defect could prevent a sale or cloud the buyer's ownership. In most cases, a title professional can resolve these issues before closing. Some of the most common title defects include:

- Unpaid property taxes

- Liens against the property

- Clerical errors in ownership records

- Forged deeds or ownership documents

- Undisclosed heirs with a legal claim to the property

What is a lien in real estate?

A lien is a claim of monetary interest in a property, typically filed and recorded with the county. The most common example is a mortgage. But liens can also arise from unpaid property taxes, home loans, or contractor work (mechanic's liens).

Standard vs. enhanced owner's policies

Not all owner's title insurance policies are the same. Most title insurers offer two tiers:

Standard policy (ALTA Owner's Policy): This covers 10 core risks, including fraud, forgery, unpaid liens and taxes, and unmarketable title. It covers claims based on events that occurred before you purchased the home.[2]

Enhanced policy (ALTA Homeowner's Policy): This covers 33 risks, including some events that occur after closing, such as a neighbor encroaching on your property, certain zoning violations, and post-purchase forgery or fraudulent activity.[3]

The enhanced policy costs roughly 10% more than the standard policy, though some states file higher rates.[4]

Whether it's worth the premium depends on your situation. An older home with a complicated ownership history, for example, may benefit more from enhanced coverage than a newly built property. Ask your title agent which level of coverage they recommend for the specific home you're buying.

Do you need title insurance?

Most home buyers have to get a lender's title insurance policy as a condition of their mortgage. Lenders require this to protect their interest in the home in case there are any title issues.

Owner's title insurance is optional but strongly recommended. Here's why:

Title insurance is a one-time cost. Unlike homeowner's insurance, which you pay year after year, title insurance is paid once at closing and covers you for as long as you own the home. Owner's title policies also pass on to anyone who inherits the property.

The odds are low, but the stakes are high. The likelihood of a title defect slipping through the search is relatively low. But if it does happen and you're uninsured, the consequences can be severe. You could face costly legal battles or, in extreme cases, lose the home and the equity you built in it. Between 2013 and 2022, the title insurance industry paid $4.4 billion in claims.[5]

In many states, the seller pays for it anyway. In some states, it's conventional for the seller to pay for the buyer's owner's policy. If you live in one of those states, you may not have to spend anything out of pocket for this coverage.

🛡️ Example of what title insurance protects you from

Suppose you buy a home and, three years later, a woman shows up claiming to be the daughter of the previous owner. She says she was never informed her late father's property was being sold, and that she has a legal right to a share of it as an heir. She files a lawsuit.

Without owner's title insurance, you'd be responsible for hiring a real estate attorney to defend your ownership. This expense can quickly run into tens of thousands of dollars, with no guarantee of the outcome. With owner's title insurance, your policy pays for your legal defense and, if you ultimately lose the case, reimburses you for your loss up to the purchase price of the home.

Who pays for title insurance?

Home buyers typically pay for the lender's title policy.

Who pays for the owner's title insurance largely depends on your location. In some areas, it's conventional for the buyer to pay; in others, the seller covers it. Ultimately, it comes down to what the buyer and seller negotiate. Even if buyers typically pay in your area, you can always try to negotiate with the seller to cover all or part of the cost.

This is who's expected to pay for owner's title insurance in each state:

| Who pays for owner's policy* | States |

|---|---|

| Buyer | Alabama, Connecticut, Delaware, Iowa*, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Minnesota, New Hampshire, New Jersey, New York, Oklahoma, Pennsylvania, Rhode Island, Vermont, Virginia, Washington DC, West Virginia |

| Seller | Alaska, Arizona, California, Colorado, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Michigan, Mississippi, Missouri, Montana, Nevada, New Mexico, North Carolina, Ohio, Oregon, South Carolina, South Dakota, Tennessee, Texas, Utah, Washington, Wisconsin, Wyoming |

| Split | Arkansas, Hawaii, Nebraska, North Dakota |

**Iowa uses a state-run program called Iowa Title Guaranty instead of private title insurance.

The Iowa exception: Title guaranty instead of title insurance

Iowa is the only state in the country where private title insurance is prohibited by law. Iowa Code § 515.48(10) bars the sale of insurance against title defects,[6] a prohibition that dates back to the 1940s, when private title insurance companies operating in the state went bankrupt and left homeowners without recourse.[7]

Instead, Iowa uses a state-run program called Iowa Title Guaranty (ITG), administered by the Iowa Finance Authority. ITG functions similarly to title insurance. It protects buyers and lenders against covered title defects, but at a significantly lower cost. For residential transactions under $750,000, the owner's coverage costs a flat $175. And if your lender also obtains ITG coverage simultaneously, the owner's coverage is free.[8]

Unlike private title insurers, ITG does not operate for profit. Excess revenue is reinvested into Iowa affordable housing programs and down payment assistance for first-time and low-income buyers.[7]

If you're buying a home in Iowa, ask your lender whether they are obtaining ITG lender coverage. If they are, your owner's coverage may be free.

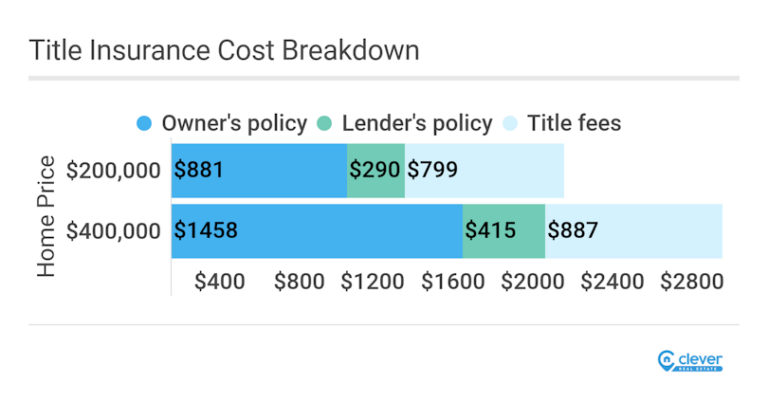

How are title insurance premiums calculated?

Title insurance costs are based on your home's value and location.

Policies are typically priced as a percentage of the home's purchase price. That percentage usually isn't fixed. If your home is more expensive, you may pay a slightly lower rate. Here's what that can look like:

| Home value | Title insurance premiums as % of home value |

|---|---|

| $200,000 | 0.55% |

| $400,000 | 0.45% |

Title insurance premiums are regulated differently from state to state, which is why your location can have a significant impact on what you'll pay.

Most states use a "file-and-use" system, where title companies set their own rates as long as they file them with the state insurance department. A handful of states (Texas, Florida, and New Mexico) go further with "promulgated" rates, meaning the state insurance commissioner sets a mandatory rate that every title company must charge.

For example, in Florida, the owner's title insurance premium for a $300,000 home is exactly $1,575 — the same regardless of which title company you choose. On a $400,000 home, it's $2,075.[9]

Texas has been actively revisiting its promulgated rates. After a multi-year review process, the Texas Department of Insurance commissioner ordered a 6.2% reduction in the state's basic title insurance premium rate, effective March 1, 2026.[10] Based on that reduction, a $300,000 home in Texas carries an owner's policy premium of ~$1,456, and a $400,000 home runs ~$1,794.

» Calculate your title insurance costs by state.

How long does a title insurance policy last?

Title insurance policies generally don't expire. They cover you until you sell the home. For mortgage lenders, the lender's policy remains in effect until the mortgage is fully repaid. Owner's title policies also pass on to anyone who inherits your home.

What title insurance doesn't cover

Title insurance doesn't protect your physical home. Damage caused by a fire, vandalism, or weather is covered by your homeowner's insurance policy, not your title insurance policy.

There are also several exclusions built into every title policy. Both standard and enhanced ALTA policies exclude, among other things:

- Government laws, ordinances, and actions, such as eminent domain

- Title defects that you yourself created, agreed to, or were aware of before purchasing

- Claims arising from bankruptcy laws

Title insurance also does not protect you from wire fraud during your closing. This is a growing and costly scam that many buyers mistakenly assume they're covered for.

Wire fraud and title fraud

As more of the closing process happens online, real estate fraud has become one of the most common financial crimes in the U.S. The FBI's Internet Crime Complaint Center recorded 9,359 real estate fraud complaints in 2024 alone.[11]

There are two types of fraud buyers should know about:

Wire fraud happens when a scammer intercepts your closing communications (typically by hacking or spoofing your agent's or title company's email) and sends you fake wire transfer instructions. You wire your down payment or closing costs to the scammer's account instead of the legitimate one. By the time you realize what happened, the money is often gone. Business email compromise (BEC), the technique most commonly used in real estate wire fraud, resulted in $2.77 billion in losses reported to the FBI in 2024.[11]

Title (deed) fraud happens when someone illegally transfers your property's title to themselves using forged documents or stolen identity. This can result in someone taking out a mortgage against your home or even attempting to sell it.

Title insurance does cover some forms of title fraud, like forged deeds or documents that existed before your purchase and were missed in the title search. What it generally does not cover is money lost through wire fraud during your closing.

How to protect yourself

- Verify wire instructions by phone before sending any money. Call your title company directly using a number you found independently (not from an email) to confirm instructions. Never trust a last-minute email asking you to change wire information.

- Use secure portals, not email, for sensitive documents. Many title companies now offer online portals specifically to reduce email interception risk.

- Check your property records. After closing, periodically verify that your deed hasn't been tampered with through your county recorder's website. Some counties offer free fraud alert programs that notify you when a document is recorded in your name.

- If you suspect fraud, act immediately. Contact your bank and request a fraud wire recall, notify your title company, and file a report with the FBI at the Internet Crime Complaint Center (IC3).[12]

How to shop for title insurance

Many buyers don't realize they have the right to choose their own title company. Under the Real Estate Settlement Procedures Act (RESPA), your lender must provide you with a list of approved title service providers in your area, but you're not obligated to use anyone on that list.[13] Be aware that lenders sometimes recommend affiliated title companies, so there may be a financial incentive behind those recommendations.

Research has found substantial, unexplained variation in title service charges between settlement agents — even for comparable transactions in the same market — suggesting that shopping around can make a meaningful difference in what you pay.[14] The Consumer Financial Protection Bureau (CFPB) notes that shopping around for title services can save buyers up to $500.[15]

Here's how to shop smart:

1. Get at least two or three quotes. Title insurance premiums are regulated by state, so the base premium may be similar across companies. But title service fees (settlement fees, document prep, closing fees) are not regulated and can vary. Ask for an itemized quote so you're comparing apples to apples.

2. Ask about the simultaneous issue rate. When you buy both the lender's and owner's policies from the same company at the same time, you're often eligible for a discount called the "simultaneous issue rate." Many buyers don't know to ask for this, and it can meaningfully reduce the total cost.

3. Ask about a reissue rate. If the home was previously insured and the prior policy was issued within the last few years, you may qualify for a discounted "reissue rate" on the new policy.

4. Check the company's reputation and local experience. A title company that does a lot of business in your specific county and market will be more familiar with the unique aspects of local public records. Ask how many closings they've completed in your state and whether an experienced closer (not just a notary) will be present at your closing to answer questions.

5. Decide between standard and enhanced coverage. Some title companies default to quoting the more expensive enhanced policy. Make sure to ask about both options and decide which is right for your situation before signing anything.

How to file a title insurance claim

If a title issue surfaces after closing, here's how to start the claims process:

Step 1: Notify your title insurer in writing as soon as possible. Don't wait. Delayed reporting can complicate or jeopardize your claim. Your policy documents will include the insurer's claims contact information and reporting instructions.

Step 2: Document everything. Gather all documents related to the title issue: the claim being made against your property, any court filings, correspondence, and your original policy.

Step 3: The insurer investigates and responds. The insurer will review the claim, determine whether it falls within your policy's covered risks, and decide how to proceed — either by defending you in court, resolving the underlying issue, or paying out on the claim up to your policy's coverage limit.

Step 4: If you disagree with the outcome, you can appeal or seek legal counsel. Most policies have a dispute resolution process. Consulting a real estate attorney is advisable if the insurer denies a claim you believe should be covered.

Related reading