You probably don't need to get an appraisal before selling your home. It's expensive and often unnecessary. Most sellers can accurately price their home based on a comparative market analysis (CMA) report, which real estate agents provide for free.

"A pre-listing appraisal is optional and typically only needed if you want a second opinion on your home's value," notes Cheryl Pendenza, a broker with RE/MAX Andrew Realty Services. "A trusted real estate professional can usually develop an effective pricing strategy by analyzing current market trends and recently sold comparables to project a range of value."

But a pre-listing appraisal could make sense in certain situations, like if you think your agent’s pricing recommendation is off base and want an objective second opinion from a pro.

An appraisal or CMA report will give you the most accurate estimate. But if you want to know your home's value and aren't ready to work with an agent, a good alternative is an online home value estimator. You'll get get a rough idea of what your house is worth and an estimated selling range within a few seconds.

This guide breaks down when getting a pre-listing appraisal might make sense (and when it definitely doesn’t). Read on to learn more so you can make an informed decision about whether the added hassle and cost is necessary to accurately price your home.

Summary: Should you get a pre-listing appraisal?

- Most home sellers probably don't need to get an appraisal before listing.

- Home appraisals are expensive ($350–$400), time-consuming (1–2 weeks or longer to complete), and often unnecessary. The entire appraisal process can take several weeks, especially in busy real estate markets

- You can get a free CMA report from a real estate agent in just a few days. CMAs are usually accurate enough to properly value and price your home. A well-conducted CMA from an experienced realtor can help you sell your home more quickly and for a higher price.

» What's your home worth? Get a CMA from a top local agent - free with no obligation

Pre-listing appraisal vs. CMA: Key differences

Both pre-listing appraisals and CMAs provide you with an estimated value of the property from a real estate professional. But there are a few key differences to be aware of.

| Pre-listing appraisal | CMA |

|---|---|

| $350–$400 | Free |

| Takes 1–2 weeks | Takes 1–3 days |

| Have to hire an independent appraiser | Prepared by your realtor |

| May be necessary for hard-to-value homes (luxury, unique, low-pop areas) | Effective for accurately pricing most homes |

Pre-listing appraisals will cost you more time and money than CMAs.

Appraisals are more formal and regulated than CMAs. Appraisers must meet certain ethical and performance standards to retain their license, whereas real estate agents aren't required to follow any specific guidelines or industry standards when preparing a CMA.

Also keep in mind that appraisers are trained to provide an unbiased opinion of value, and a realtor may not always follow the same standards (they could provide you with an inflated home valuation to win over your business, vs. providing a fair market value).

» MORE: Learn more about CMAs (and how to get one for free)

Who should consider a pre-listing appraisal?

While a CMA report is usually enough to accurately estimate a home's value, some sellers may still benefit from a pre-listing appraisal. Here are two possible scenarios when springing for a pre-listing appraisal could make sense:

You don't agree with your agent: If your real estate agent prepares a CMA and you disagree with their valuation (for example, the value seems too low), an independent appraisal can help verify your home's actual market value.

Your home is hard to value: Realtors typically need to pull at least 2–3 recent sales of similar homes in your area to get an accurate CMA. If your area has few recent home sales — or your home is unique in terms of style and features — an appraisal might be a good idea.

An attorney recommends getting an appraisal: In some situations, such as selling a home in a divorce or as an inherited property, it might make sense to get a pre-listing appraisal so that everyone involved has access to an expert opinion about the home's value before it goes on the market.

Appraisers can pull comps from further away or use other other valuation methods, like the cost approach, to reach an accurate estimate.

If you want just a general idea of what your home is worth, you can get a free online home value estimate. These estimates aren't as accurate as a CMA or an appraisal, but you can at least get your bearings when it comes to knowing the value of your home.

Discover the true value of your home with our Home Value Estimator!

If you’re still on the fence about a pre-listing appraisal, keep reading — I’m going to break down some additional situations and guiding questions that can help you reach a decision.

How to decide if you should get a pre-listing appraisal

If the answer is "“no"” for either of these questions, then we recommend contacting a local realtor for a free CMA.

1. Do you have the money?

Appraisals typically cost $350 to $400 or more, depending mainly on the size of your house and your market.

If you can't afford (or don't want) to pay for an appraisal out of pocket, we recommend finding an agent who can provide a CMA for free. You may also want to read up on how to negotiate lower realtor commission rates when selling.

2. Do you have enough time?

Appraisals can take a few weeks or longer to complete. Appraisers are in high-demand and can be hard to book, and then it takes several days to actually complete the report, especially in busy markets.

Make sure a pre-listing appraisal fits in with your sale timeline. If your goal is to sell ASAP or fairly soon (1–3 months), then you should probably pass on it.

» LEARN: How to sell your house fast

5 common reasons you might want a pre-listing appraisal

1. You and your agent disagree about pricing

An appraiser provides an objective, third-party opinion that will either prove your agent's valuation wrong, or confirm it. This can help you land on a fair-market value.

Here's how: Appraisals consider the whole picture — comparable home sales, your home's condition, and its improvements and upgrades — while a CMA tends to focus more on comparable home sales.

Appraisers also have more experience and training when it comes to valuing homes — it's literally all they do, while realtors have dozens of other responsibilities.

2. You're worried about mispricing your home

Pre-listing appraisals could make sense when you're worried about underpricing or overpricing your home, and to get a more detailed home valuation.

But if there are at least a few comparable home sales in your area, you can always get a second and third opinion from other agents via free CMAs vs. paying for an appraisal.

» Need an experienced agent? Clever can help

3. You live in an area with few recent home sales

It can be hard to complete a CMA in remote or rural areas where not many homes have sold.

Appraisers have experience pulling home sales from further away, and can factor in additional home features such as lot size, land use (residential, commercial, or industrial), and outbuildings (barns, sheds, garages, workshops, etc.).

Appraisers can also use the cost approach or the income approach (for investment properties) to value your home, if necessary.

4. Your home has unique features that are hard to value

Appraisers tend to have more experience valuing a home's unique features than realtors. Examples of unique features include:

- Flashy outdoor renovations (fireplace, brick oven, huge in-ground pool, putting greens, etc.).

- Converted garages or attics.

- Second story additions.

- Luxury bathroom features (freestanding tubs, walk-in shower, marble floors, etc.).

- High-end kitchen renovations and appliances.

5. You're selling for sale by owner (FSBO)

On average, FSBO listings sell for 22% less than agent-listed homes, and mispricing homes is likely a major contributing factor.

Setting the list price too low can leave a ton of money on the table, while going too high risks your home not selling, receiving and taking a lowball offer, or re-listing with an agent (and burning a lot of your time and energy). Decluttering and cleaning can also help you avoid these pitfalls.

Why FSBOs should avoid CMAs

Can't you just trick an agent into giving you a free CMA? You can, but we don't recommend it. Realtors are usually self-employed and work 100% on commission. It's wrong to lead them on if you have no intention of hiring them.

You may also get a ton of follow-up calls after your appointment (until you make it clear you don't need their help). It's best to be honest with the agent.

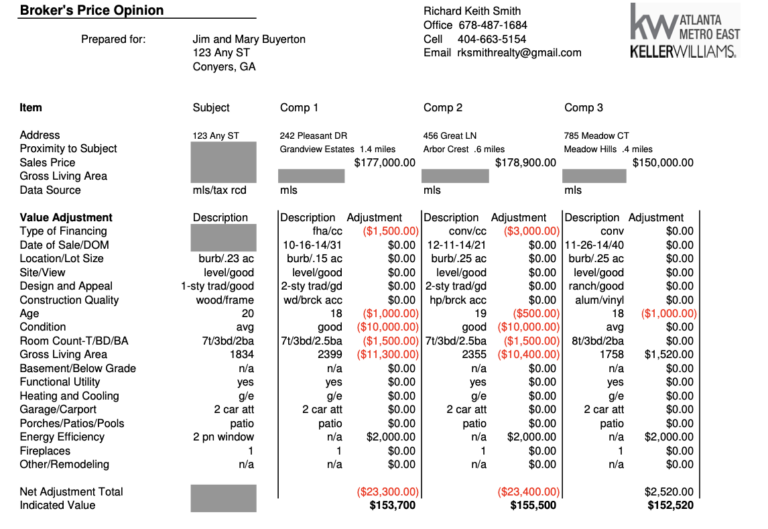

Instead, ask an agent for a broker price opinion (BPO). A BPO is a home valuation report prepared by a realtor, but unlike a CMA, you pay for it ($50–$100). It's a lot cheaper than an appraisal, and it can pay for itself in terms of the impact on your ability to sell fast and for a good price.

| Can't I just get an appraisal online?A pre-listing appraisal or CMA will give you the most accurate estimate of your home's value to best help you price your home. (Get a free CMA from a top local realtor now). But an online appraisal tool can be a good first step if you just want a general idea of your home's worth. Our home value estimator tool gives you a free, convenient home valuation in seconds. Find out what your home is worth here. |

How do pre-listing appraisals work?

The first step is to call a licensed appraiser to set up an in-person appointment.

Your initial phone call is a great time to bring up any repairs or improvements you've made to your home since buying it. You can also make a repair list and give it to them when they arrive at your home.

Appraisals cost between $350 to $400 (paid after the report has been completed), although it could cost more, depending on your market and the size of your home.

What happens during the appraisal?

The appraiser spends an hour or so walking through the inside and outside of your house, examining its overall condition, its features and amenities, and measuring its square footage.

Appraisers take plenty of photos of your home's bedrooms, bathrooms, kitchen, garage, front and back yard, and of the surrounding area, including your neighborhood's recent home sales.

What does the appraiser look at?

Appraisers consider the size and general condition of your home, including its location, age, and any updates or repairs you've made since taking ownership.

FHA or VA loan appraisals take it a step further, as appraisers are required to inspect the home's major components (HVAC, roof, electrical, plumbing, etc.) for health and safety compliance.

What happens after the appraisal?

What happens after the appraisal?

After the appraiser finishes their inspection, they’ll go back to their office to upload photos and notes to prepare their report.

The appraisal report is completed and emailed over to you. The exact timeline depends on the appraiser’s schedule and how fast they work (it may take a few days or longer).

The appraiser should either call or email you payment instructions once the report is completed, and you can view it after making payment.

You’ll be able to download the appraisal report. These reports are typically at least 20–25 pages and full of numbers and abbreviations. But your report should also have a summary page with the appraiser's opinion of value (and a brief summary of how they arrived at it).

Call your agent (if you have one) and the appraiser to discuss the report if you have any questions or need an explanation.

3 potential pre-listing appraisal outcomes (and what to do after)

1. Appraisal comes in high, or as expected

A high or as-expected appraisal value is a best-case scenario because it means the appraiser thinks your home is worth as much as (or more!) than you do. You can price your home and roll with it!

Ask your agent if it makes sense to share the appraisal report with potential buyers to support your listing price, and to help with price negotiations once an offer has been submitted. You can also back out if the appraisal is higher than the offers you get.

2. Appraisal comes in lower than expected

If the home’s value is far lower than expected, you may need to take a step back and re-evaluate your pricing strategy — and potentially take a hit on your expected price.

If the difference in value is small, and you're in a hot market with limited inventory, it could make sense to roll the dice and list higher than the appraised value. There's always the chance that your home's value rises by the time you list — or you’ll find a buyer who loves your home and is willing to pay up for it.

Your agent can advise you on the best route to take.

Note: You can challenge a low valuation, but only if you think the appraiser used the wrong comparable homes, or made errors. You have to provide evidence to support your argument, and there's no guarantee the appraiser will change their mind.

3. Appraisal uncovers issues with the home

It's possible the appraiser could discover an issue during their inspection (like a plumbing or roof leak, a busted HVAC system, mold, etc.) that negatively affects your valuation.

It may be smart to get a pre-listing inspection to get to the bottom of it. You can then either make the repairs or sell your home in as-is condition, depending on your budget, and the cost vs. benefit of fixing the issues.

It's best to ask your agent the best way to proceed (or find an agent if you don't have one yet).

Your appraisal vs. buyer's appraisal

A pre-listing appraisal informs your pricing strategy, but that’s all. If the buyer uses a mortgage to purchase your house, their lender will likely require a new appraisal a few weeks before closing.

Here's why: Lenders need to protect their investment, and ensure the appraisal value is accurate and up to date.

Housing prices fluctuate: There could be a rise or fall in housing demand in your area by the time you sell your home, due to fluctuations in interest rates, inventory levels, and seasonal trends.

Homes are selling fast: Appraisals are partly based on recent home sales, and homes that sell after your pre-listing appraisal can change your home's valuation, resulting in a higher or lower value.

Why it's important to price your home correctly

Low appraisals can be a deal-killer. If you list for way higher than its fair value, you risk getting few showings and offers. Even if you do get a good offer, the buyer's appraisal may come in lower than the sale price, which could potentially derail the deal.

A low appraisal isn't always the end of the world, but you and the buyer would need to negotiate on how to make up for the appraisal gap — which could mean lowering the sale price or making seller concessions.

Next steps

1. Talk to an agent: Call your agent — or find an agent if you don't have one yet — to decide on getting a CMA or a pre-listing appraisal.

2. Get a CMA report: Ask an agent for a free CMA report, and make sure you mention any renovations or upgrades you've made since buying the home to get the highest valuation.

3. Or get a pre-listing appraisal: Ask your agent or a lender for appraiser recommendations, search on sites like HomeAdvisor or Angi, or browse for certified appraisers in your area.

4. View the report: The CMA or pre-listing appraisal should help you decide on a fair listing price, and if you need to make any upgrades or repairs before listing.

5. Prepare your home for sale: Determining your home's fair value is just one step in the home sale process. Learn other ways to get your house ready to sell.

Don't sell your house without getting a local agent's expert opinion first. Fill out the form below to get a free home valuation from a top-rated realtor from a trusted brand like Keller Williams or Berkshire Hathaway. It's 100% free with no obligation.

Pre-listing appraisal FAQs

Pre-listing appraisal FAQs

Why might a seller want to get their own appraisal before listing?

A pre-listing appraisal might make sense when a seller doesn't agree with their agent's recommended listing price. Pre-listing appraisals can also be useful for accurately pricing homes in areas with few recent sales — or homes with unique features that make them hard to value based on comparable sales.

How much above pre-listing appraisal value should I list my house?

You can technically list your home for any amount you want, but pricing it above your pre-listing appraisal value risks it sitting on the market with no offers. And a high sale price could result in a low appraisal that potentially delays or derails the entire deal. Talk to your agent about whether or not you should list your home for more than its pre-listing appraisal value.

Who hires the appraiser when buying a house?

The buyer's lender is in charge of hiring the appraiser, although the buyer still pays for the report. Lenders need appraisals to verify that the property's value aligns with the purchase price, thereby protecting the lender's investment. Appraisers are licensed, independent professionals who have no business relationships with lenders or realtors.