💸 How Is Debt Impacting Americans' Stress in 2026? 😣

Three-quarters of Americans (76%) are in debt, with almost half of them (46%) saying stress about their debt has affected their day-to-day functioning. Meanwhile, 50% say their debt-related stress has increased in the past year.

America’s Debt Profile | Most Stressful, “Dumbest” Type of Debt | Debt Regrets | Long-term Debt Stress | Debt Delays Major Life Milestones | How Often Americans Feel Financial Stress | Debt Stress Coping Strategies | The Lifestyle of Americans With No Debt | Most Common Debt and Money Goals for 2026

For better or worse, debt is a foundational part of the modern economy. Although buying on credit is as old as commerce, it’s easy to see how developments over the past century have changed the way the average person interacts with and manages debt.

Since the advent of the 30-year, fixed-rate mortgage in the 1930s, debt has supercharged the American housing market while allowing even ordinary people to take on debt loads well into the six figures.

Over the same time, credit cards have gone from a rarity and status symbol to the default method of payment for millions, regardless of whether they actually have the funds to back up their swipes or taps.

Meanwhile, new forms of debt have proliferated, such as buy now, pay later programs, and even longstanding types such as car loans have grown larger and more common.

The result is that it’s easier than ever for Americans to take advantage of debt — or alternatively, have debt take advantage of them.

To find out more about how much debt Americans have, how they feel about it, and how it’s affecting their lives, Clever Real Estate surveyed 1,000 adults, over three-quarters of whom (76%) have some kind of debt.

About 3 in 4 Americans with debt (73%) consider having debt to be normal, but a similar number of those in debt (77%) say it has held back or even harmed their life. Almost half (46%) say stress related to their debt has affected their day-to-day functioning.

Worse still, half of Americans in debt (50%) say their debt stress has increased in the past year, even as nearly all (92%) say they’re making changes or sacrifices to manage their debt.

Read on to learn more, including fascinating insights into the minority of Americans without debt, many of whom make major lifestyle changes to remain so.

🏦😰 Debt Stress Statistics

- Over three-quarters of Americans (76%) have some kind of debt.

- About 3 in 4 Americans with debt (73%) consider having debt to be normal, and just under two-thirds (62%) believe debt is sometimes necessary to get ahead financially.

- Credit card debt is the most common form of debt, with nearly half of Americans carrying it (44%), but it also ranks as the most stressful (34%) and dumbest (29%) form of debt.

- Mortgages are the clear winner when it comes to the smartest debt to take out (43%), although they’re also second when it comes to the most stressful (22%).

- 87% of those in debt say they have regrets about their debt.

- Credit cards are the debt most people regret, with 58% of those who have it expressing remorse, but almost half (48%) of those with student loan debt regret it as well.

- Among those with debt, 92% say they’re making changes or sacrifices to manage it.

- However, this means that 1 in 12 debt-holders (8%) are not making any changes to manage their debt.

- Almost half of Americans with debt (44%) have missed or delayed a debt payment in the past year, while 39% currently have debt with a collections agency.

- 63% of those in debt say the last time they were debt-free (excluding mortgages) was 2020 or earlier, while a third (34%) say it was 10 years ago or longer.

- Nearly half of Americans with debt (42%) worry they’ll die in debt.

- Half of Americans in debt (50%) say their stress about their debt has increased in the past year, and 46% say this stress has affected their day-to-day functioning.

- 81% of Americans with debt say that debt has caused them to delay or avoid major milestones, such as saving for retirement, moving to a better home or neighborhood, or buying a house.

- Nearly two-thirds of Americans who have debt (64%), and 71% of those who don’t, say they wouldn’t marry someone with significant debt.

- 1 in 4 Americans in debt (23%) have lied about their debt to a partner or spouse.

- Over half of those in debt (53%) stress about their finances once a week or more, nearly 20 percentage points higher than those without debt (34%).

Three-Quarters of Americans Are in Debt, With Over Half of Debtors Worried About Their Long-Term Financial Future

The prevalence of debt and Americans’ attitudes toward it reveal just how deeply ingrained this aspect of the financial system is in many people's minds.

Over three-quarters of Americans (76%) have some form of debt, and a similar share of those who owe money (73%) consider having debt to be normal. Just under two-thirds of debtors (62%) believe debt can be necessary to get ahead financially.

Still, 77% of those with debt say owing money has held back or harmed their life, and over half (55%) worry about their long-term financial future because of debt. Almost half of debtors (47%) feel ashamed about their debt.

Substantial numbers of those in debt owe potentially life-altering amounts of money. Over a third (35%) call their debt unmanageable, while a troubling 42% also worry they’ll die in debt.

Despite these relatively common personal issues, 55% of debtors admit they judge others for being in debt. Gen Z is the most judgmental generation at 62%, and boomers are the least, at 47%.

Credit card debt is the most common form of debt, held by almost half of respondents (44%). This is likely fueled by the near-majority of Americans in debt (49%) who use credit cards to cover essential expenses. This exposes them to potential spikes in debt should they lose their incomes. In contrast, only 28% of those without debt use credit cards for essentials.

The five most common forms of debt are:

- Credit card debt (44%)

- Auto loans (24%)

- Personal loans (19%)

- Student loans (19%)

- Medical debt (19%)

Notably, more than 1 in 6 respondents (17%) have buy now, pay later debt. This new form of consumer credit has only begun to show up on credit reports within the past two years, suggesting some users may not have fully weighed the impact these convenient loans have on their long-term financial picture.

Millennials (82%) are the most likely to be in debt, while boomers (67%) have the lowest proportion of debtors.

Among Americans who have a given type of debt, they hold a median balance of:

- Mortgages: $178,000

- Student loans: $34,000

- Auto loans: $18,000

- Personal loan: $7,500

- Credit card debt: $6,000

- Medical debt: $5,600

- Buy now, pay later debt: $1,221

Millennials, Gen Z Hold Higher Balances in Most Debt Categories

Beneath these overall numbers, there are critical distinctions among different groups of Americans.

For example, millennials ($198,000) and Gen Z ($198,000) have median mortgage amounts 53% higher than boomers ($129,000), reflecting the significantly shorter time the younger generations have had to pay down their loans. When it comes to auto loans, millennials ($19,000) and Gen Z ($18,000) once again outpace boomers ($13,500), with balances 30% to 40% higher.

Although they have the least amount of debt in other categories, boomers ($9,750) have the highest median credit card balance of any generation, almost double Gen Z’s median of $5,500.

Meanwhile, despite requiring the most health services, boomers with medical debt ($2,100) have less than half of Gen Z’s level ($4,600) and around a quarter of millennials' ($8,100). This may reflect the reality that the vast majority of boomers are now eligible for Medicare, while younger generations still face an uneven mix of employer coverage and health insurance marketplaces.

Despite this access to health coverage and smaller debt balances, boomers (23%) are still 2x to 3x more likely to say medical debt is the most stressful form of debt compared to millennials (11%) and Gen Z (8%).

Overall, 83% of Gen Z and 81% of millennials say some form of debt has harmed or held back their lives. Only 57% of boomers say the same, showcasing how younger Americans have increasingly felt the burden of debt loads their elders didn’t face.

Although 72% of Americans with debt say they pay their bills on time, this overall number belies substantial differences across generations. Just 54% of indebted Gen Zers fall in this group, 18 percentage points lower than millennials (72%) and 33 percentage points below boomers (87%).

Americans Say Credit Cards Are Most Stressful, Dumbest Type of Debt

Among all types of debt, credit cards undoubtedly stand out. They’re viewed as the most stressful form of debt (34%) — far ahead of mortgages (22%), student loans (15%), and medical debt (12%).

However, they’re simultaneously viewed as the most manageable form of debt (27%) and the least manageable form (26%).

Although it’s easy to understand why many Americans consider high-interest credit cards to be an unmanageable form of debt, it’s worth considering that many may view them as more manageable than other forms because of the relative flexibility they can provide compared to fixed payments for mortgages, auto loans, and more.

Mortgages likewise break even on views of them as manageable vs. unmanageable, a reflection of their typically large balances but also of their predictable, long-term nature.

Americans also see credit cards as the dumbest form of debt (29%), beating out second-place buy now, pay later debt (22%).

In contrast, there’s far more consensus on the smartest form of debt: mortgages (43%). There’s one generational exception to this. Only 19% of mostly non-homeowning Gen Z believe mortgages are the smartest form of debt, compared to 40% of millennials and 61% of boomers.

Notably, credit card debt (13%) is essentially tied with student loans (12%) as the smartest form of debt to incur.

In fact, a similar percentage (13%) think student loans are the dumbest form of debt to take on. This feeling is most common among college-aged or recently graduated Gen Z (18%). Those in debt (15%) are also twice as likely as those who aren't (8%) to call student loans the dumbest form of debt.

This may be a somewhat surprising finding, given the conventional wisdom about the value of investing in education, but that advice seems to have fallen out of favor among those who have followed it most recently.

Credit Cards, Student Loans Are Most Likely to Hold Back Debtors

Credit cards (38%) are also the clear leader when it comes to the most common type of debt that indebted Americans feel has harmed or held back their lives. That’s twice the 19% who feel credit card debt has improved their lives.

More than 1 in 5 (21%) of those with debt, however, say student loans have held them back the most. This includes a third (32%) of Gen Z.

Mortgages (30%) are the clear leader for the type of debt that has improved debtors’ lives the most. Still, this just narrowly edges out the 1 in 4 Americans with debt (26%) who say no type of debt has improved their life.

With this in mind, it makes sense that Americans in debt are fairly clear in their preferences for which types of debt to prioritize paying off, with credit card debt first (40%) — nearly double the 21% who say mortgages and 4x the percentage for third-place personal loans (11%).

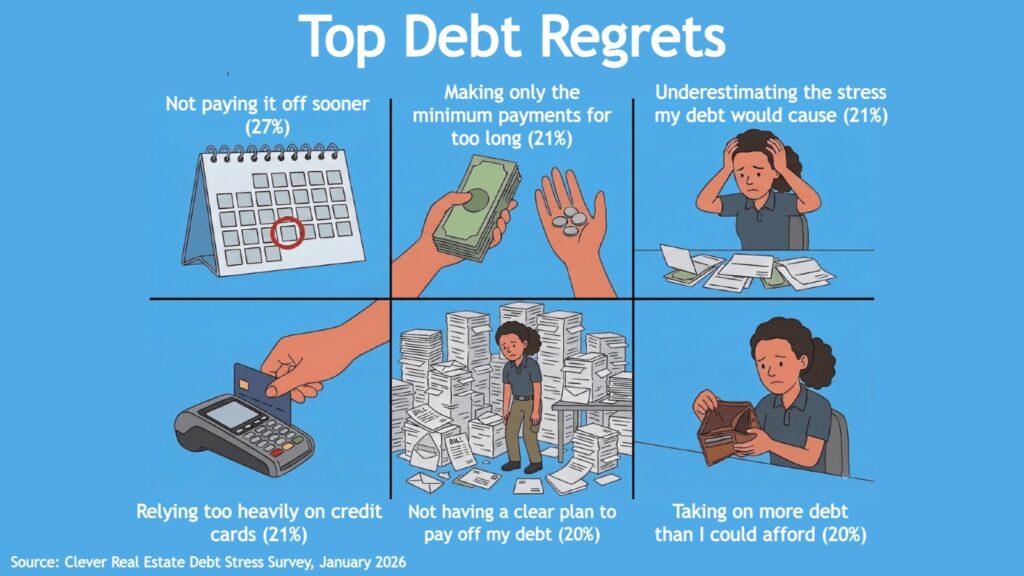

Nearly 9 in 10 Americans Have Regrets About Their Debt

Even if Americans can acknowledge that debt isn’t necessarily a bad thing in theory, their actual financial reality reveals a different picture. About 87% of those in debt say they have regrets about their debt.

Over a quarter (27%) say they regret not paying it off sooner, the most common response among all generations and both men and women. However, this ranges from 34% of boomers to 23% of Gen Z.

There’s a large cluster of other regrets roughly 1 in 5 Americans have, including:

- Making only the minimum payments for too long (21%)

- Underestimating the stress their debt would cause (21%)

- Relying too heavily on credit cards (21%)

- Not having a clear plan to pay off their debt (20%)

- Taking on more debt than they could afford (20%)

- Taking on multiple debts at once (20%)

There are also broad differences among the types of debt people regret. Credit card debt is the only type with a majority of those who have it (58%) regretting it. Still, almost half of those with student loans (48%) regret taking out the debt.

On the other hand, only 19% of those with mortgages regret going into debt to buy a house, and fewer than 1 in 4 of those with auto loan debt (24%) regret it.

When Debt Feels 'Too Much'

There are a variety of signs those in debt see as evidence that their debt has begun to feel “too much” for them to handle.

Most commonly, these are:

- When monthly payments feel hard to keep up with (33%)

- Missing or falling behind on payments (32%)

- When they can’t afford necessary expenses, such as a car repair, furnace repair, water heater repair, etc. (31%)

However, the numbers also reveal a wide range of tolerance for different levels of debt among Americans who carry it.

For example, 29% feel their debt has become “too much” when it goes to a collection agency, a serious step that could lead to long-term credit damage, while 26% say the same for when debt limits their ability to afford things on a day-to-day basis.

On the other hand, 28% say debt feels “too much” as soon as they can’t meaningfully save money anymore.

Spending Cuts, Career Changes, and Bankruptcy: How Americans Are Managing Their Debt

Whether or not debt has become “too much,” it’s clear that nearly all of those who have it are taking it seriously. Among those in debt, 92% say they’re making changes or sacrifices to manage it.

As might be expected, the most common debt management strategies are:

- Cutting back on discretionary spending (33%)

- Sticking to a strict budget (33%)

- Pausing major purchases to get their debt under control (31%)

- Paying more than the minimum on their debts (29%)

- Taking on extra work or a side income (25%)

Meanwhile, some are taking even more drastic, life-altering steps due to their debt. Almost 1 in 5 (19%) are looking to change to a new, higher-paying career, while 1 in 9 (11%) are declaring bankruptcy or considering it.

Mid-career millennials are most likely to be weighing a career switch for debt-related reasons, with almost 1 in 4 (24%) saying so.

Naturally, there are other major differences among generations in how they choose to manage their debt. Boomers (43%) are roughly twice as likely as Gen Z (22%) to cut back on discretionary spending, and the same holds true for paying more than the minimum on their debts: 40% versus 22%.

On the flip side, Gen Z is more likely than boomers to:

- Pause major purchases (33% vs. 23%)

- Take on extra work or income (33% vs. 21%)

- Automate debt payments (20% vs. 11%)

- Seek professional financial advice or counseling (18% vs. 4%)

- Consolidate or refinance debt (17% vs. 6%)

All of these make sense for a younger generation that’s both more tech-savvy and has a longer career runway ahead of them but also has less experience managing their finances.

Despite all this, 44% of indebted Americans, including 57% of Gen Z, have missed or delayed a payment on a debt in the past year. Another 39% of Americans with debt currently have debt with a collections agency. Almost half of millennials (46%) and Gen Z (46%) are among them.

Half of Americans in Debt Haven’t Been Debt-Free Since 2020 or Earlier — And Feel Growing Stress About It

For many, being in debt is a long-term problem. Among those with debt, a third (34%) say the last time they were debt-free, excluding mortgages, was 10 years ago or longer. Nearly twice that amount (63%) say their non-mortgage debt has been hanging over them since at least 2020.

This doesn’t mean the intensity of debt stress hasn’t varied over time. Half of Americans in debt (50%) say their stress about their debt has increased in the past year. That includes 60% of indebted Gen Zers.

Troublingly, a third of those with non-mortgage debt (35%) saw their debt levels increase in the past three months, more than twice the number who reported a decrease (15%). Gen Z (41%) and millennials (37%) are about twice as likely as boomers (20%) to say their debt increased recently.

Likewise, boomers (30%) are roughly 4x as likely as Gen Z (8%) to have their debt decrease in the past three months.

Things have been a bit bleaker over the past year; 41% of those with non-mortgage debt say their debt levels increased over that period, compared to 17% who decreased their debt. Once again, Gen Z is experiencing the worst effects, with almost half (46%) saying their debt increased in the past year, compared to 28% of boomers.

Americans Don’t Expect Debt to Increase in 2026, But They Don’t Expect to Pay Off Their Loans, Either

The largest percentage of Americans with non-mortgage debt (41%) expect their balances to stay the same in the year ahead. However, a third (33%) expect their non-mortgage debt to decrease in 2026, higher than the 25% who expect it to increase.

Once again, Gen Z (30%) and millennials (28%) are far more pessimistic about their debt increasing than boomers (13%). Conversely, a whopping 58% of boomers expect their non-mortgage debt to decrease in the coming year. Only about half as many Gen Zers (32%) and millennials (28%) agree.

However, those in debt generally aren’t expecting to get out of it anytime in the near future, either. Excluding mortgages, just 14% of Americans with debt expect to become debt-free this year. This number rises to 31% by the end of 2027.

However, a quarter (26%) think they’ll still be paying off their non-mortgage debts more than six years from now.

Regardless of how imminent a threat this may be, 42% also worry they’ll die in debt.

Despite all this, two-thirds of Americans with debt (65%) are optimistic about what they owe. As with many other similar stats, Gen Z lags behind, with just 57% optimism.

This is likely fueled, in part, by sunnier predictions for their finances overall. About 39% of Americans with debt, and 37% of those without, foresee their financial situation improving in 2026. Only 19% and 20% of these groups, respectively, expect their financial situation to get worse in the year ahead.

Debt Has Forced 81% of Debtors to Delay or Avoid Major Life Events or Milestones

Debt has wide-ranging impacts on those dealing with it, regardless of the amount or how long they’ll be paying it off. Well over three-quarters of those in debt (81%) say owing money has caused them to delay or avoid major milestones.

This includes a wide range of needs and wants, such as:

- Taking vacations or traveling (28%)

- Building an emergency fund (28%)

- Making major purchases, such as a car or appliance (25%)

- Saving for retirement (25%)

- Improving their living situation (20%)

Roughly 1 in 5 millennials (20%) and Gen Zers (20%) with debt say their loans have forced them to delay or avoid buying a home. It’s likely this is part of the reason that the average age of first-time home buyers has reached record highs in recent years.

About 30% of Gen Z also say their debt prevents them from improving their living situation by moving to a better home or neighborhood, compared to just 13% of boomers.

Even for those who have bought homes, about 1 in 7 (14%) have had to delay or avoid renovations or repairs.

Most shockingly, about 1 in 5 millennials (19%), all of whom will be 30 or older by the end of 2026, say their debt prevents them from moving out of their parents' house or out of a home with roommates to an independent living situation.

Boomers in debt face different challenges, including 1 in 4 (23%) who say they’ve delayed medical appointments or medical procedures.

More generally speaking, almost two-thirds of those with debt (64%) feel their debts limit their sense of financial freedom. Meanwhile, just 40% of those in debt feel prepared for an unexpected large expense.

Roughly Two-Thirds of Americans Wouldn’t Marry Someone With Major Debts

A small but notable number of Americans have also had to put major events in their personal lives on hold because of their debt, including starting or growing a family (12%), retiring (9%), getting married (8%), or even getting divorced (6%).

Ironically, nearly two-thirds of Americans with debt (64%) say they wouldn’t marry someone else with significant debt.

The percentage of Americans without debt who wouldn’t marry someone with significant debt is similarly high at 71%.

Findings like this may help explain why roughly 1 in 4 Americans in debt (23%) have lied about their debt to a partner or spouse. Almost a third (32%) of indebted Gen Zers admit to doing this.

A Third of Americans in Debt Feel Financial Stress Every Day

Financial stress is a fact of life for most Americans, with nearly three-quarters (73%) saying they feel it at least once a month, and almost half (49%) feeling financial stress at least once a week.

Still, whether a person is in debt makes a massive difference in how they experience this stress. Over half of those with debt (53%) stress about their finances once a week or more, nearly 20 percentage points higher than those without debt (34%).

Almost a third of Americans with debt (31%) feel stressed about their finances every day. Only 22% of those not in debt say the same.

A lucky 1 in 5 (19%) of those without debt say they never feel stressed about their finances, 3x the number of those in debt who don’t ever stress about it (6%).

By a narrow margin, more Americans feel their financial situation is worsening compared to last year (26%) rather than improving (21%). However, a majority of Americans (52%) are financially treading water, saying their financial situation is staying about the same.

Notably, there’s little difference between those in debt and those who aren’t. Among debtors, 21% see improvement compared to 27% who have a worsening situation. For non-debtors, 21% are improving versus 23% who are worsening.

Distractions, Exercise, and Stress Eating Are Top Debt Stress Coping Mechanisms

Debt-related stress can have real, noticeable effects on the daily lives of those suffering under it. Almost half of those in debt (46%) say stress from debt has affected their day-to-day functioning. A majority of Gen Z (57%) is among them.

A similar 44% say debt stress has negatively affected their sleep or physical health.

So, how do those stressed about their debt handle it? The most common option is distracting themselves with TV, social media, or other diversions — a technique over a third (36%) of this group uses.

Many of the top coping strategies focus on making debtors temporarily feel better, rather than improving their outlook. These include:

- Exercise or physical activity (27%)

- Stress eating (27%)

- Engaging in a hobby, such as cooking, journaling, art, etc. (23%)

- Venting or complaining to a partner, family member, or friend (21%)

- Crying (18%)

However, 1 in 4 handle their debt stress by planning how to get out of debt (25%) or setting small financial goals to feel they’re making progress (24%).

Although men (32%) are more likely to lean on exercise as debt stress relief than women (24%), they’re also nearly twice as likely (21%) as women (12%) to reach for alcohol and other substances.

Younger Americans Use More Unhealthy, Counterproductive Coping Strategies

To be sure, all generations indulge in some unhealthy, unhelpful, or even counterproductive habits to deal with stress. However, younger Americans are often more likely to be guilty of them.

For example, 1 in 4 Gen Zers (23%) say their coping methods include crying, compared to 14% of boomers. In addition, Gen Z (20%) and millennials (18%) are 2x to 3x more likely to use alcohol or other substances to cope with debt stress, compared to boomers (7%).

Meanwhile, nearly 1 in 5 millennials (19%) and 16% of Gen Zers avoid opening bills or checking balances. Again, only 7% of boomers manage their stress in this way.

There’s also a social element: 1 in 6 (16%) millennials and Gen Zers cope by comparing themselves to others who seem worse off. This is more than twice the number of boomers (7%) who do this.

Gen Z (16%) is also far more likely to simply deny they’re in debt as a coping mechanism, twice the number of millennials (9%). Almost no boomers (2%) are in this kind of denial.

About 1 in 8 millennials (13%) and Gen Zers (13%) may actually make their financial situation worse while trying to deal with the debt-related stress by indulging in “retail therapy” or impulse spending. Decades of life experience have led just 5% of boomers to do the same.

Still, it’s worth noting that, at 13%, Gen Zers are also much more likely to take part in traditional therapy or counseling for their debt stress than boomers (2%).

A Majority of Non-Debtors Wouldn’t Take On Debt to Significantly Improve Their Quality of Life

Avoiding debt of any kind in today’s economy is undoubtedly an unusual feat. Naturally, an almost universal 92% of Americans without debt say they’re proud of this.

Some of this can likely be explained simply by their attitude toward debt. In contrast to the 73% of indebted Americans who believe having debt is normal, only 57% of debt-free Americans believe it’s normal to have debt. Nevertheless, this is still a majority, indicating how widespread these attitudes are, regardless of a person’s financial situation.

Likewise, a slim majority of debt-free Americans (51%) believe debt is sometimes necessary to get ahead financially. However, that’s still an 11 percentage point difference from the 62% of those in debt who feel this way.

On the other hand, roughly 1 in 7 Americans without debt (14%) admit they judge people differently if they find out they’re in debt.

At the same time, roughly a third (30%) are so committed to a debt-free life that they wouldn’t even take on debt if needed for an emergency.

Even if debt would significantly improve the quality of their lives, 55% still wouldn’t do so. Another 38% of debt-free Americans don’t believe any debt is ever acceptable.

Ending up debt-free was not an accident for most of these respondents. Almost two-thirds (62%) have made lifestyle sacrifices to remain debt-free, while 84% say they prefer to live debt-free even if it limits their major purchases.

Still, almost half (46%) admit it’s a challenge to stay debt-free. Another 46% say they’ve stayed in a stable job longer than they wanted to avoid potential debt.

In spite of all of this discipline and sacrifice, a third (33%) think they'll fall into debt in the future.

Saving Money, Avoiding New Debt Are Americans’ Top Financial Goals for 2026

Financial goals are always a common aspiration, and in 2026, the most common one among Americans is to save more money for emergencies (41%).

The top financial goals for 2026 include:

- Save more money for emergencies (41%)

- Avoid taking on new debt (38%)

- Pay down debt (36%)

- Save more or start saving for retirement (30%)

- Budget better/track spending more closely (29%)

- Fully pay off debt (25%)

- Improve financial skills/knowledge (24%)

- Invest more money (23%)

- Get a higher-paying job or promotion (22%)

There are two critical differences between those in debt and those who aren’t when it comes to these goals. Almost half of those without debt (46%) plan to save more money for emergencies, compared to 39% of debtors. Meanwhile, 42% of those in debt have a goal to avoid taking on new debt, compared to 24% of those without debt.

Generational differences persist, too. Although 37% of millennials and 36% of boomers have a 2026 goal to pay down debt, only 26% of zoomers say the same. Gen Z is apparently more focused on improving their financial skills and knowledge; 28% of them have a goal to do so in the year ahead, compared to 11% of experienced boomers.

Early-career Gen Z (32%) is also the most focused on getting a higher-paying job or promotion, compared to millennials (24%) and boomers (4%).

Although relatively few Americans (6%) say they have no financial goals for 2026, this is roughly 3x more common among those without debt (11%) than those with it (4%).

Methodology

Clever Real Estate surveyed 1,000 adult Americans concerning their debt levels and attitudes toward debt. The survey ran Jan. 29th, 2026.

About Clever

Since 2017, Clever Real Estate has been on a mission to make selling or buying a home easier and more affordable for everyone. 12 million annual readers rely on Clever's library of educational content and data-driven research to make smarter real estate decisions—and to date, Clever has helped consumers save more than $210 million on Realtor fees. Clever's research has been featured in The New York Times, Business Insider, Inman, Housing Wire, and many more.

More Research From Clever Real Estate

Articles You May Like

FAQs

What are the most common types of debt?

Credit card debt is the most common form of debt, with nearly half of Americans carrying it (44%). Learn more.

What regrets do Americans have about their debt?

Among the 87% of Americans with debt who regret it, over a quarter (27%) say they regret not paying it off sooner, while over 1 in 5 regret making only the minimum payments for too long (21%), underestimating the stress their debt would cause (21%), or relying too heavily on credit cards (21%). Learn more.

How are Americans managing their debt?

The most common debt management strategies are cutting back on discretionary spending (33%), sticking to a strict budget (33%), and pausing major purchases to get their debt under control (31%). Learn more.

How is debt impacting the lives of Americans who owe money?

Approximately 81% of Americans in debt say debt has caused them to delay or avoid major milestones, including building an emergency fund (28%), taking vacations (28%), saving for retirement (25%), and making major purchases, such as a car or appliance (25%). Learn more.