You've agreed on a price, your offer was accepted, and then your lender sends over the Closing Disclosure. Somewhere in the middle of a long list of costs, you see "escrow fees." And if you're like most buyers or sellers, you're not entirely sure what you're actually paying for.

Escrow fees are part of your closing costs and typically run 1–2% of the home's purchase price. On a $400,000 home, that's $4,000–$8,000. The fees are paid to a neutral third party (an escrow company, title company, or real estate attorney), who manages the transfer of money and documents so the transaction closes cleanly.

The good news: these fees are negotiable, and in many markets, the buyer and seller split them. A knowledgeable agent can help you understand what's reasonable in your area and advocate on your behalf. Here's what you need to know.

Buy your home with a top Clever agent, get cash back.

Clever vets agents based on performance from Berkshire Hathaway, Keller Williams, and hundreds of other top brokerages and negotiates cash back on your behalf.

What is escrow?

Escrow is a third-party service that acts as a neutral holding zone for funds and documents during a real estate transaction. Neither the buyer nor the seller controls the escrow account; the escrow company does until both parties have met all the conditions of the sale.

Think of it like this: You wouldn't hand a stranger $400,000 on the promise that they'll hand you a house later. Escrow exists to make sure the money moves only when the deal is legitimate and complete.

There are actually two different ways you'll hear "escrow" used in real estate:

- Escrow at closing: The temporary account used during the home sale to hold the buyer's earnest money, coordinate documents, and distribute funds to all parties at closing. This is where escrow fees come from.

- Escrow account after closing: An ongoing account your mortgage servicer maintains to collect and pay your property taxes and homeowners insurance on your behalf. This isn't a fee — it's money you'd owe anyway, just held by the lender.

When people ask "what are escrow fees?", they're almost always asking about the first type.

What are escrow fees?

Escrow fees are what you pay the escrow company (or title company or real estate attorney) for facilitating the closing process. The fee structure typically works one of two ways:

- Flat fee plus a percentage: Many companies charge a base fee (often $250–$500 per party) plus $1–$2 for every $1,000 of the sale price. On a $400,000 sale, for example, you might see a base fee of $250 plus $800 (at $2/per $1K), totaling $1,050 per side — or about $2,100 split.

- Percentage of sale price: Others simply charge 1–2% of the purchase price total.

The term "escrow fees" is also used as an umbrella term for the full range of costs the escrow company manages at closing. These commonly include:

- Property taxes (prorated at closing)

- Attorney fees

- Title insurance premiums

- Document preparation

- Notary services

- Wire transfer fees

Less common add-ons include flood insurance, HOA transfer fees, or rush/expedited document fees. Your escrow officer will walk you through the full breakdown; be sure to ask for it in writing before closing day.

Who pays escrow fees?

The buyer and seller typically split escrow fees. However, you can negotiate and specify who pays escrow fees in the purchase agreement.

In certain areas, it’s customary for one party to cover all the escrow fees.[1]

| Sellers cover escrow in: | Buyers cover escrow in: |

| Southern California | Louisiana |

| Maryland | |

| Northern California | |

| West Virginia |

Market dynamics also play a role. In a seller's market, buyers sometimes offer to cover escrow fees to make their offer more attractive. In a buyer's market, sellers may offer to pay them as a concession to get a deal done. If you're buying with cash or have strong negotiating position, it's worth asking. You may be surprised what's possible.

Working with an experienced local agent matters here. They know what's typical in your market and can help you negotiate who pays what — potentially saving you thousands. Find a top Clever agent in your area →

How much are escrow fees?

According to Mortgage Investors Group, escrow costs are 1–2% of the property’s value.[2]

Escrow fees typically run 1–2% of the home's purchase price when you count all third-party costs managed through escrow. Here's what that looks like in real numbers:

| Home sale price | Estimated escrow fees (1–2%) |

| $300,000 | $3,000–6,000 |

| $412,000 (national median) | $4,120–8,240 |

| $500,000 | $5,000–10,000 |

Keep in mind that the escrow company's actual service fee (what you pay for their time and administration) is usually a smaller portion of this. The rest is made up of third-party costs (taxes, title insurance, etc.) that are held and distributed through escrow.

Several factors affect your total:

- Location: Some states and counties have higher escrow costs than others due to local regulation, attorney requirements, and typical fee structures.

- Property tax rates: Higher property taxes mean more funds moving through escrow at closing.

- Insurance premiums: Homes in flood zones, hurricane-prone areas, or high-risk neighborhoods carry higher insurance costs.

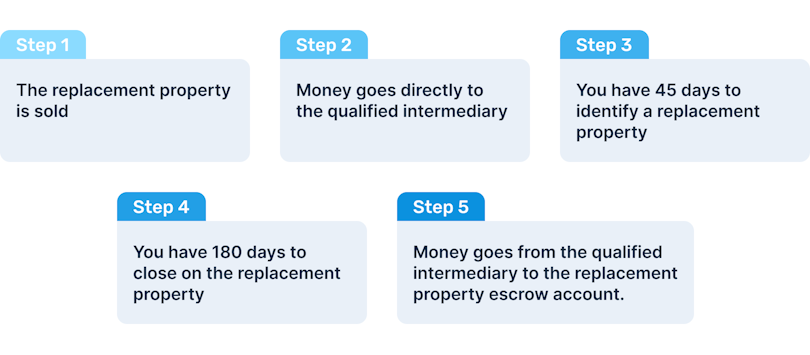

- Transaction complexity: 1031 exchanges, estate sales, or transactions involving multiple liens typically cost more.

{kind=link}

You can often negotiate or shop for a better rate. Ask your agent to recommend a title company with competitive fees. In most states, you have the right to choose your own escrow provider, and prices vary.

Before agreeing to the terms of your escrow, carefully review the contract and consult a real estate attorney if you need clarification on anything.

How the escrow process works

- Open an escrow account and deposit earnest money. After agreeing on a price, the buyer and seller sign a purchase agreement to start the escrow process. Your real estate agent will work with you to open an account, collect earnest money, and deposit it into escrow as a sign of good faith.

What to watch for: Missing your earnest money deadline can put you in breach of contract, so make sure the deposit deadline in your contract is realistic. - Undergo a title search and acquire insurance. Title searches evaluate the home’s history to ensure the property’s title is clear and transferable. You also acquire title insurance at this stage to act as a safety net against future claims on the property’s title.

- Complete property inspections and negotiate. Once the money is deposited, a home inspector completes a thorough inspection to ensure the home meets expectations. Any problems the inspector finds will need to be addressed before the sale is complete.

What to watch for: Don't skip specialized inspections (such as mold, termite, or roof) if the general inspector flags concerns. It's better to find out about a potential $20,000 before you close on the house. - Complete the appraisal process and secure financing. After the home inspection, buyers can negotiate a lower purchase price or for the seller to repair problems found during the inspection. The buyer’s lender will then perform an appraisal to determine fair market value and offer financing.

- Review and sign documents. After securing financing, the buyer and seller meet to sign documents that finalize the sale. These include the closing disclosure of final costs, the deed, loan documents, and other required paperwork.

- Fund the escrow account. The buyer deposits the remainder of the down payment and closing costs into the escrow account. From there, the lender wires the remaining payment into the account.

- Close escrow. The escrow company performs a final evaluation to determine whether all the conditions for the sale are met. If everything checks out, it distributes funds to necessary parties and officially transfers ownership by registering the deed with the local government.

What are the conditions of escrow?

Conditions of escrow are certain obligations listed in the escrow agreement that each party must comply with before the deal can move forward. A real estate transaction can't close until all terms have been satisfied by the deadlines in the escrow agreement and both parties have signed the appropriate documentation.

Here are some of the most common conditions of escrow that must be met before closing in real estate:

- The buyer's lender does an appraisal and approves financing, which is transferred to the escrow account.

- The escrow account pays property taxes, homeowners insurance, and mortgage insurance (if required) on behalf of the buyer.

- The seller completes any repairs that were discovered during the inspection and agreed upon in the purchase and sale agreement.

- The title report shows the title is clear of any liens.

- Title insurance is purchased to protect the buyer and lender of any legal challenges that didn't come up during the title report.

Once all the conditions specified in the escrow agreement are met, the transaction can move to closing.

How to find a reputable escrow company

In most states, you have the right to choose your own escrow or title company, and it's worth shopping around because fees vary.[3] Start by asking your real estate agent for referrals; good agents have worked with multiple providers and know who is reliable and competitively priced.

When evaluating options:

- Check online reviews and ratings.

- Verify licensing and insurance (your state's department of financial institutions or insurance will have a lookup tool).

- Ask for a sample fee schedule up front.

- Ask how they communicate: Will you have a dedicated escrow officer, and how quickly will they respond?

- Get estimates from at least 2–3 companies before choosing.

One practical tip: some companies charge additional fees for things like wire transfers ($30), notary services ($150), or document preparation ($75–$100) that won't appear in the headline rate. Ask for a full itemized estimate in writing.

The right escrow company keeps your transaction on track. A good agent can recommend trustworthy providers — and having an experienced agent in your corner is often the best protection against surprises at closing. Find a top Clever agent near you →

Sourcing referrals and talking with previous customers are two reliable ways to learn if an escrow service is legit. You can also do the following:

- Analyze its online reviews

- Look up the company’s licensing and insurance

- Ask for their portfolio of prior deals

Don’t settle on the first company you find. Instead, interview multiple escrow services to get the best deal. Many real estate agents can recommend trustworthy services to evaluate. The right company will help you keep your transaction costs straight to ensure the process goes smoothly.

Buy your home with a top Clever agent, get cash back.

Clever vets agents based on performance from Berkshire Hathaway, Keller Williams, and hundreds of other top brokerages and negotiates cash back on your behalf.

Top FAQ about escrow in real estate

What happens when a house is in escrow?

When a house is in escrow, the real estate transaction is in its final stages. Once a buyer makes an offer that a seller accepts and a purchase and sales agreement is drawn up, the buyer will make an earnest money deposit on the house. That deposit opens the account, and the escrow process begins.

Each party has different tasks they must complete during this process. For buyers, this could mean securing financing and fulfilling any requirements of their mortgage lender, such as paying property taxes, homeowner's insurance, title insurance, and private mortgage insurance. Inspections and appraisals may also happen at this time.

Sellers will most likely take the home off the market and make any agreed-upon repairs.

What does it mean when a house falls out of escrow?

A house falls out of escrow when the negotiated terms of the purchase contract can't be met. This can happen for a variety of reasons:

- The buyer may not qualify for a mortgage.

- The home inspection could turn up serious issues that the buyer and seller can't agree on.

- The appraisal ordered by the lender could come up short, leaving the buyer unable to meet the purchase price.

- The title search could reveal hidden liens on the property that must be sorted out before the seller can legally sell the house.

What's the difference between escrow fees and an escrow account?

These are two different things that often get confused. Escrow fees are the one-time costs paid at closing to the escrow company for facilitating the transaction. An escrow account is an ongoing account your mortgage servicer maintains after closing; it collects a portion of your monthly payment and uses it to pay your annual property taxes and homeowners insurance on your behalf. The escrow account doesn't have a service fee; you're just pre-funding costs you'd owe anyway.

Can I negotiate escrow fees?

Yes, in many cases. The third-party costs held in escrow (like property taxes and insurance) aren't negotiable, but the management fee for the escrow service itself often is, especially in cash transactions or in markets where multiple providers compete for business.

You can also negotiate with the seller to have them cover a portion or all of the fees. In some states you can shop for your own escrow provider; ask your agent whether that's an option in your market.

How long does a house stay in escrow?

A house stays in escrow until the requirements laid out in the escrow agreement have been satisfied. As long as the inspection reveals no additional issues, the buyer qualifies for funding, and the title is clear, a house usually stays in escrow anywhere from 30–60 days. Of course, this can be much longer if unexpected issues pop up.

Do you get escrow money back at closing?

Escrow money is the fee paid to the escrow service, title company, or attorney who handles the account and processes. It's not a deposit, but someone must pay those fees to the escrow officer. Unless the buyer and seller have negotiated who pays the escrow fees, they usually split these fees down the middle.

What happens to money in escrow if the buyer backs out?

If the buyer backs out of the sale, contingencies in the purchase agreement — and when and why the buyer backs out — will determine what happens to the earnest money in escrow. Sellers don't like contingencies in a contract but may agree to them in a buyer's market. A loan contingency, an appraisal contingency, and a home sale contingency are most common.

Contingencies say that if certain conditions aren't met before a certain date, a buyer can back out within a specified window of time and keep the earnest money. Otherwise, if a buyer simply gets cold feet and backs out, the seller is usually entitled to keep the earnest money.

Are HOA fees included in escrow?

Yes, some HOA fees fall into escrow. But it’s important to read the details of your escrow agreement because HOA fees aren’t included with every escrow account.

How are escrow fees calculated?

Escrow fees are calculated based on several factors, including:

- The selling price of the home

- Property tax rates

- The complexity of the transaction

- Where you’re located

- How long escrow lasts

- Special services provided by the escrow company

What’s included in escrow fees?

Escrow fees include legal and administrative fees paid during the closing process on a home. Property taxes, attorney fees, title insurance and search, document preparation, notary services, and fees paid to the escrow company often fall under escrow fees, but this list isn’t exhaustive.

Are escrow fees tax deductible?

No, not all escrow fees are tax deductible. However, some of the fees you incur during escrow may be deductible. It’s essential to consult a knowledgeable tax expert before assuming which costs count as a tax write-off.