"How to fix my credit score in 6 months" is one of the most often searched queries from potential homebuyers, especially if their credit isn’t currently in the best shape.

Having good credit is essential for qualifying for a mortgage. And, since 65% of American homeowners currently have a mortgage on their home (as opposed to just paying for it outright in cash), it is very likely that you will need to get one, too.

Credit scores are important because they tell the lender many things about you. But, most importantly, they let them know how good you are at paying back money that you owe.

If a lender if going to give you hundreds of thousands of dollars, they want to make sure you are good for it.

What is a credit score?

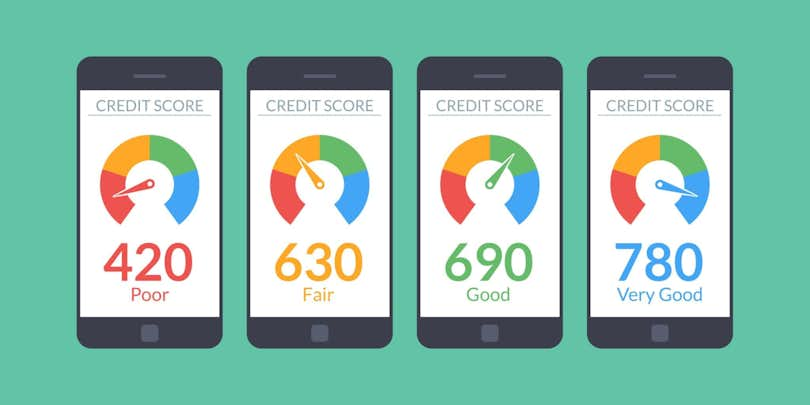

A credit score is a number that tells lender how likely you are to pay back money you owe. Scores range from 300 (the worst) to 850 (the best). The higher your score, the more money lenders will be willing to give you because they know you will likely have no problem paying them back.

This is because you have a proven track record of paying your debts in full, on time.

Many different factors go into your credit score. Here are just a few of the things that are likely to show up on your credit report.

Student Debt

If you took out money to attend university, then all of those loans are likely to show up on your credit report, especially if you are a younger first-time homebuyer. Student loans are the first experience that many young Americans have with building up their credit. It is the first time that they realize it becomes important to pay on time each month to achieve good credit.

Credit Card Debt

This is the most common type of debt to appear on credit reports because most people use credit cards, starting early and often in their life. Your credit report looks at how many credit accounts you have open, how close you come to maxing them out each month, and whether or not you pay your bills on time.

Past Loans

Whether it is for a car, house, or business venture, any money you have borrowed in an official capacity from a lender will show up on your credit report. Future lenders will pay close attention to the amount of the loan as well as the payment history attached to it.

How does a credit score impact your mortgage?

Credit affects many things in a mortgage. It’s best to lead by example:

Let’s take the example of a $20,000 auto loan:

If you have good credit….

You get an interest rate of 2.69%

You get a repayment period of 60 months.

Your monthly payment is $357.

The total repayment is $21,420.

If you have average credit…

You get an interest rate of 3.19%

You get a repayment period of 60 months.

Your monthly payment is $361.

The total repayment is $21,600.

Even just the difference of a few points in your credit score will cost you money. In this case, it’s only $240 of the course of the loan. But that’s with a relatively small difference in the interest rate.

Differences in mortgage rates can be as much as 1.5%... Can you imagine how much more you would pay for a house over the course of 30 years?

How can I quickly improve my credit?

Once you know your credit is not exactly where you want it to be, the first step is not to panic. Avoid the urge to have your lender check it all the time to see if it’s "good enough yet." This is because each time you do a "hard" inquiry into your credit, it can drop by a few points.

A hard inquiry is when an official lender looks into your credit for you.

A "soft" inquiry, however, is when you check your credit yourself. You can look at this credit as often as you would like, as this is simply responsible credit management.

However, checking it daily is likely to just stress you out. Small fluctuations in your credit score are normal as it evens itself out. Make a promise to yourself to only check up on your credit once a month, with more time in between if possible.

While you’re waiting in between checks, here are the best steps to take:

Check for errors.

The easiest way to get rid of poor credit is to simply review your credit report for errors. Credit bureaus have human employees. They can make mistakes! Ensure that every loan amount, term, and payment is correct.

If you find an error, contest it! While contesting a credit error is an involved process, it is totally worth it and can save you a lot of money in the long run.

Consolidate payments.

Money guru Dave Ramsey has an excellent method of consolidating debt called the Snowball Plan.

Here is what Dave says:

Myth: You need to pay off the debt with the highest interest rate first to get out of debt quickly.

Truth: You should knock out the smallest debt first to create momentum in your debt snowball.

So, instead of just meeting your minimum payments for your debts each month, you can gain momentum by knocking out your smallest debt first, then using that money on your next smallest, until your debt is completely under control.

Using this Snowball Plan method can really help you with the next step as well…

Pay on time.

Once you have the money to send off to your creditors each month, this step becomes a breeze. However, even if you are just meeting your minimum payments, it is essential to pay on time. Just one late payment of 30 days can drop your credit score by up to 100 points!

So, one of the easiest ways to improve your credit score is to either set up automatic payments from your bank account directly to your lenders, or at least set up reminders so you don’t miss the deadline, even by just a few hours.

Spend less.

A great way to improve your credit is to not use it.

Well, all of it anyway. Let’s say you have a credit card that has a limit of $10,000. Don’t put that much (or anywhere near it!) on your card each month. This is called a credit utilization ratio. Essentially, using 35% of less of your credit limit each month looks really good. And, if done consistently, can raise your score.

How long does poor credit last?

What if you are currently on track to great credit but have had some financial hiccups in the past? What if you have consolidated your debt into manageable monthly payments and no longer max out your credit cards?

Just how long do the little blemishes stay on your credit record?

Any negative reports on your credit score stay there for about seven years. So, if you missed a credit card payment on Jan. 1, 2016, then this missed payment report wouldn't "fall off" your credit report until Jan. 1, 2022! This means that you don’t have to close out an account to eventually leave the bad bits of it in the past—just keep up the good work and it will eventually work itself out.

Likewise, if you close out a credit account, either because you completely paid off the debt (like with a student loan) or if you just don’t want to use as many credit cards anymore, the entire account falls off your report after seven years as well.

But there is even more good news!

Good credit upkeep never really goes away. If you are paying your bills on time each month and keep the account open, your credit report will reflect the great work you are doing indefinitely. Even if you do end up closing the account (again, like with a student loan), the positive information will stay accessible to credit bureaus on the report for up to 10 years after the fact.

‧ ‧ ‧ ‧ ‧

Look for an agent who can help you buy a home, no matter your credit? The team at Clever are experts at helping connect buyers with their dream homes. Call us today at 1-833-2-CLEVER or fill out our online form to start.