After the effects of the 2008 Great Recession wore off, the housing market in the United States boomed in the mid and late 2010s: mortgage interest rates were hitting record lows month after month, average monthly home sales increased by 43% between 2008 and 2020, and home values increased by 23% in that same time period.

However, the COVID-19 pandemic put everything on hold.

A historic bull market was swiftly cast aside in the wake of lockdowns and widespread economic turmoil caused by the novel coronavirus.

With rapidly growing unemployment rates and general uncertainty about the severity of the economic impact of the shutdowns, mortgage lenders began tightening their lending standards.

Many homeowners bought just before COVID-19 took over the country, when the market was seemingly strong. Since then, many pre-pandemic buyers have lost significant portions of their household income and are facing unexpected financial hardships.

Many buyers continue to show interest in the housing market in spite of stricter standards.

Sellers have tended to be more cautious in the wake of the lockdowns by keeping their homes off the market: Realtor.com data show an average of nearly 32% fewer new weekly listings and 43% fewer listing-price reductions since mid-March compared to the same weeks last year.

Despite that large drop in new listings and steady prices, home buying demand remains strong with continued week-over-week increases in sales throughout May, according to the Mortgage Bankers Association; but how has the financial security and general outlook of recent home buyers changed in the wake of a global pandemic?

To answer questions like this, we surveyed 1,000 homeowners (May 31 through June 2, 2020) who purchased their home between January and May of 2020. We asked them questions about their current finances, mortgage, and how they felt about homeownership.

Recent home buyers have had very different experiences than those who purchased their homes before the pandemic. Most notably, they experienced more negative affect related to homeownership, higher levels of buyer’s remorse, and more concerns about finances than those who bought between 2015 and 2019.

2020 home buyers are more than twice as likely to report feelings of anxiety and stress than home buyers who bought in the last 5 years, and they’re less likely to report feelings of comfort, security, happiness, and pride.

In this study we’ll dig deeper into financial challenges recent home buyers are facing.

JUMP TO SECTION

- Key Insights

- Recent Home Buyers Are Concerned About Finances

- Financial Contributors Have Lost Jobs

- Mortgage Payments Are Cause for Concern

- Homeowners Are Running Out of Savings, Taking on Debt

- 2020 Homeownership Brings Anxiety and Remorse

- Recent Home Buyers Report More Negative Feelings Toward Homeownership

- Buyer’s Remorse Hits Hard

- Mortgage Lenders Have Tightened Their Standards

- Sellers Have the Upper Hand

- 2020 Buyers Are Less Motivated by Money

- 2020 Buyers’ Must-Haves Include Garages, Large Kitchens, Growth Opportunities and Safe Neighborhoods

- Methodology

Key Insights

- 2020 home buyers are more than twice as likely to report feelings of anxiety and stress than home buyers who bought in the last 5 years, and they’re less likely to report feelings of comfort, security, happiness, and pride

- Roughly 75% of 2020 home buyers reported feeling concerned about paying their mortgage due to COVID-19-related financial hardships.

- In spite of COVID-19 fears, it’s still a seller’s market. 42% of homeowners who bought during the pandemic reported entering a bidding war

- 55% of 2020 home buyers reported that at least one person who typically contributes financially to housing costs has lost their job since purchasing their home

- 63% of home buyers who bought in the beginning of 2020 reported being concerned about their home going underwater compared to 53% of people who bought during the pandemic.

- 37% of recent homeowners have taken out more than $2,000 in non-mortgage debt since purchasing their home

- Nearly one-quarter of recent buyers have less than $1,000 in emergency savings

- 23% of home buyers who bought during the pandemic reported never entering the home in person, only viewing photos or doing a virtual tour

- Regrets of homeownership are largely related to worries about the value of one’s home as a result of the pandemic

Recent Home Buyers Are Concerned About Finances

Buying a new home can be more expensive than expected once you account for moving costs, warranties, insurance, new utility fees, and other often overlooked costs. People who purchased their home in 2020 were in for some additional concerns in the wake of COVID-19, though.

Financial Contributors Have Lost Jobs

COVID-19 brought about millions of job losses in a matter of weeks in early March as shutdowns began to sweep across the country. By April, when the economy lost 20.5 million jobs, the unemployment rate reached a record high of 14.7%.

Joblessness is financially stressful regardless of homeownership status, but people who lose their jobs after a big purchase like a house are put into a unique position.

Over half of the homeowners we surveyed said that at least one person who typically contributes to housing costs had lost their job since purchasing their home, leaving many with a new mortgage and far less money coming in.

Pre-pandemic buyers who purchased before the WHO declared COVID-19 a pandemic (i.e., in January or February, 2020) were slightly more likely to be affected by those widespread job losses with nearly 60% of homeowners losing one income compared to 50% of those who purchased since March (i.e., pandemic buyers).

Mortgage Payments Are Cause for Concern

The coronavirus-related shutdowns brought about the CARES Act, which required banks to allow deferred payments without penalty for government backed mortgages.

As a result, many homeowners aren’t paying their full mortgage each month. In April, we asked homeowners whether they were paying their mortgage as part of our COVID-19 Financial Impact Series (denoted as "Average Homeowners" in the graphs below). The homeowners in that survey could have purchased their homes at any time prior to April 28, 2020.

At that time, nearly 84% said they were paying in full.

In stark contrast, only 55% of the recent home buyers we surveyed said they’re paying their mortgage in full — even fewer (45%) if a financial contributor has lost their job.

Even more concerning is that many of those who aren’t paying their mortgage in full right now don’t have an agreement with their lender.

Recent buyers were 1.7x more likely to be late on their payments without having an agreement in place than the average homeowners we surveyed back in April, suggesting that more-recent buyers were less financially prepared for the pandemic.

Regardless of whether people are currently paying their mortgage in full, nearly 80% of recent buyers said they’re concerned about making mortgage payments in the coming months as a result of COVID-19 related financial hardships.

Homeowners Are Running Out of Savings, Taking on Debt

Many new homeowners use the bulk of their savings as a down payment toward their mortgage and take on additional debt as they settle into their new home. Loss of savings to fall back on and racking up debt amid an economic downturn isn’t ideal.

American consumer debt is around $14 trillion, leaving the average household with over $137,000 in debt. While much of that debt is from mortgages, the average household with at least one credit card carries over $8,000 in credit card debt alone, according to Debt.org.

Credit card debt alone makes up a small proportion of household debt but high interest rates can cause long-term expenses and difficulty repaying those debts, especially during a financial crisis.

37% of the homeowners we surveyed have taken on more than $2,000 in non-mortgage debt since purchasing their home this year.

The combination of increasing expenses from a brand new house and taking on additional debt as a result of homeownership and the coronavirus pandemic has put many homeowners in a tough spot financially.

Having little in emergency savings leaves people at risk of taking on even more debt when unexpected events — like suddenly losing income during a pandemic — hit home.

Last year, 31% of respondents in our annual Credit Card Debt Survey indicated that they wouldn’t be able to pay for a $2,000 emergency out of pocket and would instead use a credit card.

Recent home buyers are in a similar situation: Nearly one-quarter of those who purchased a home in 2020 currently have less than $1,000 in emergency savings.

2020 Homeownership Brings Anxiety and Remorse

The majority of prospective home buyers consider owning a home to be part of the American Dream — a rite of passage into adulthood that exudes success.

But purchasing a home can come with feelings of regret, anxiety, and stress as costs pile up and other factors, like the state of the economy, shape buyers’ view of the future.

Recent Home Buyers Report More Negative Feelings Toward Homeownership

Last year, we surveyed people who purchased their home between 2015 and 2019 about costs related to their home in our True Cost of Homeownership Survey. Many of those buyers were more likely to report feelings of happiness, security, pride, and comfort as a result of homeownership.

Those who purchased their home in 2020, however, immediately experienced an economic downturn. Millions of people lost their jobs, businesses closed, and the world seemed to change overnight as a result of COVID-19.

Those 2020 buyers have different feelings when it comes to homeownership than the people we surveyed last year. More specifically, 2020 home buyers are more than 2x as likely to report feelings of anxiety, 1.6x as likely to report stress, and nearly half as likely to say homeownership makes them feel comfortable and secure than those who bought in the last 5 years.

Buyer’s Remorse Hits Hard

The cost of buying a home can bring on feelings of regret in many new owners regardless of whether the purchase was a good decision or not. Worries about the future likely exasperate feelings of regret when it comes to buying a home.

In fact, 2020 home buyers are 28% more likely to report having feelings of buyer’s remorse than those who purchased their homes between 2015 and 2019.

Those feelings of remorse were largely associated with concerns about home values dropping, wishing a better deal came along, and the expense of a mortgage.

The possibility of home values declining is especially worrisome for new homeowners who have little equity in their new homes — and that worry was reflected in our data such that 58% of recent homeowners were concerned about going upside down on their mortgage.

Interestingly, those who purchased during January and February of this year are more concerned (63%) about going underwater on their mortgages than those who bought during the pandemic (March through May, 53%).

The discrepancy between pre-pandemic and during-pandemic 2020 buyers is likely due to expectations: Those who purchased a home during the pandemic had expectations that the market was slowing down and may have purchased accordingly, whereas those who bought a home before March this year were under the impression that the housing market in the U.S. was going strong.

Interestingly enough, the fears of going underwater may be unwarranted as home prices have yet to dip down past last year’s prices and historically home values don’t suffer as a result of pandemics, according to Zillow.

In the case that home values do depreciate, many projected a "checkmark" shaped impact wherein the market would rebound quickly after the pandemic lockdowns were eased.

Mike DelPrete’s recent research on the real estate market suggests that trends in many — but not all — markets have begun to show that checkmark pattern as restrictions have been lifted.

The trend toward a quick rebound implies that people’s worries about home equity are likely unfounded in the long run.

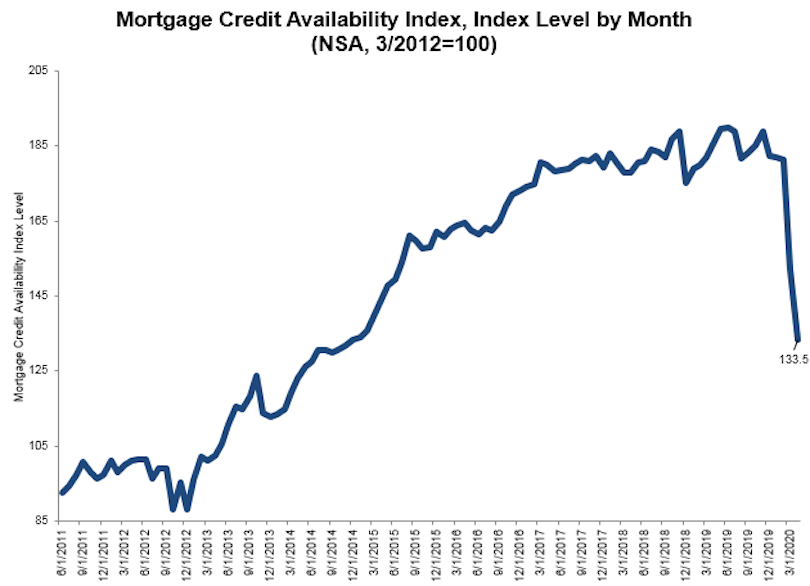

Mortgage Lenders Have Tightened Their Standards

The 2008 financial crisis caused banks to tighten their lending standards for mortgages to avoid future housing bubbles. But as time went on, those standards loosened.

Over the last couple of years, banks were requiring lower down payments and credit scores than in previous years and there was an increase in subprime lending. For instance, nearly 40% of home buyers put less than 20% down on their homes in 2018, up from only 22% in 2008.

Since the pandemic, lenders have begun tightening their standards again. According to Reuters, the largest lender, JPMorgan, increased minimum credit scores and down payments in April as a protective measure against COVID-19 related economic hardships.

The Mortgage Bankers Association’s mortgage credit availability index suggests that lenders took a swift turn toward tightening standards in recent months, as well.

New homeowners are having a harder time getting a mortgage without a hefty downpayment and high credit scores.

In fact, people who purchased a home in 2020 were 32% less likely to put less than 20% down on their homes than those who purchased between 2015 and 2019.

Sellers Have the Upper Hand

Even though mortgages are more difficult to obtain, there seems to be plenty of demand in the housing market.

In line with our previous survey data that suggested homeowners were holding off on putting their homes on the market, Realtor.com reported 23% fewer homes on the market now than this time last year.

Moreover, the prices have remained relatively steady compared to last year and a smaller proportion of sellers have reduced their listing price as of late (41% fewer in the week ending on May 30), suggesting that the demand for homes is still present.

While inventory was down over the past few months, the Mortgage Bankers Association reported increased week-over-week sales throughout May, including a 5% increase in the first week of June, 2020. Redfin also suggested that demand for housing was up 17% in May from pre-pandemic rates, showcasing a "seller’s market."

The seller’s market means that buyers have to act quickly and aggressively when making decisions on buying a home — sometimes offering over asking price or getting into a bidding war with other potential buyers.

In fact, over 40% of homeowners who purchased their home during the pandemic reported entering into a bidding war on at least one home.

The shutdowns from the pandemic have also led to restrictions on how real estate processes are carried out. While specific state and local governments put in place different mandates, many real estate agents moved toward online viewings and meetings instead of in-person.

In pre-pandemic times, buying a home sight unseen was relatively rare. According to the National Association of Realtors, the average buyer looked at about 9 homes in person before putting in an offer in 2019, but over 20% of 2020 home buyers bought their home without viewing it in person.

Buying a home without seeing it does come with some risks, even in the middle of a pandemic. Much of that risk lands on the buyer, putting the seller in a better position to frame their home positively in photos or virtual tours.

2020 Buyers Are Less Motivated by Money

People’s desire to own a home is like a rite of passage — homeownership is part of the American Dream and a symbol of success and prosperity. The reasons people buy a certain home at a particular time, though, varies depending on personal and economic circumstances.

The majority of homeowners who purchased their homes in the last 5 years said they bought their current home because it was cheaper than renting and they were tired of throwing money away on rentals and the home was a good investment.

People who purchased their home in 2020 had slightly different motivations. More specifically, 2020 buyers were less likely to be motivated by renting versus buying advantages and investment opportunities, but were more motivated by the ability to make renovations, starting a family, and being able to host family and friends.

2020 Buyers’ Must-Haves Include Garages, Large Kitchens, Growth Opportunities and Safe Neighborhoods

Earlier this year, we asked prospective home buyers what features of a home they considered "must haves." The majority of respondents needed a garage and large kitchen, a dedicated laundry room, and space to grow.

While those who did purchase a home this year had similar top requirements, they were more interested in having room to grow, two stories, a pool, and dedicated office space than those who hadn’t purchased a home yet.

The differences in must haves likely has something to do with concessions during the buying process, but the pandemic situation could have encouraged buyers to look for different properties, as well.

More specifically, remote work has become widely available for many jobs where it wasn’t before, so more people were likely looking for dedicated office space in their new homes to ensure they had a place to work in the coming months or long term. Additional space to grow and play with a family, like a pool, could also be motivated by the increased need to stay homes as a result of the pandemic.

Buyers are also typically concerned about the location of their home. Previous prospective buyers indicated family matters and safety concerns to be the top-ranking priorities when it came to looking for a home and those who bought this year were no different.

Nearly 40% of 2020 home buyers indicated that safe neighborhoods were the most important location factor when they chose their home, followed by good school districts (18%) and proximity to family and friends (18%).

Methodology

The data in this report were gathered from an online survey on May 31 through June 2, 2020. The only restriction for participation was that respondents were 18 or older, lived in the United States, and had purchased a home between January and May of 2020.

We collected data from 1,000 homeowners who each answered up to 21 questions (some were dependent on answers to other questions, so not all respondents answered all of the questions).

You can find all the questions and data here.