As home values skyrocketed during the pandemic, homeowners made huge equity gains. But now that home prices are dropping in many markets, about 450,000 recent home buyers are experiencing a problem we haven't seen for a while: Their mortgages are underwater.

According to the Mortgage Monitor report by Black Knight, 60% of those homes were purchased in 2022. If these underwater homeowners try to sell anytime soon, they'll need to come up with the difference between their net sale result and what they owe on their mortgages.

What does it mean when a home is underwater?

When a home is underwater, it means the homeowner owes more on the mortgage than the home is worth. For example, if a homeowner has a mortgage of $300,000 but the current value of the home has fallen to $250,000, the home is considered to be underwater.

This can make it hard to sell, because you need to come up with the difference between the mortgage and the net sale price to pay off the mortgage.

Andrew Daniels, co-founder of Millennial Homeowner, notes an additional problem for these homeowners: "Being underwater on your home can also make it difficult to refinance your mortgage, which could prevent you from taking advantage of lower interest rates in the future or changing the terms of your mortgage."

Finally, being underwater means you don't have any equity to enable a home equity loan or a home equity line of credit, or HELOC. Those are two common ways that homeowners fund a home renovation.

>>OUTSMART THE MARKET. Get Clever Real Estate's free weekly newsletter for homeowners, buyers and sellers.

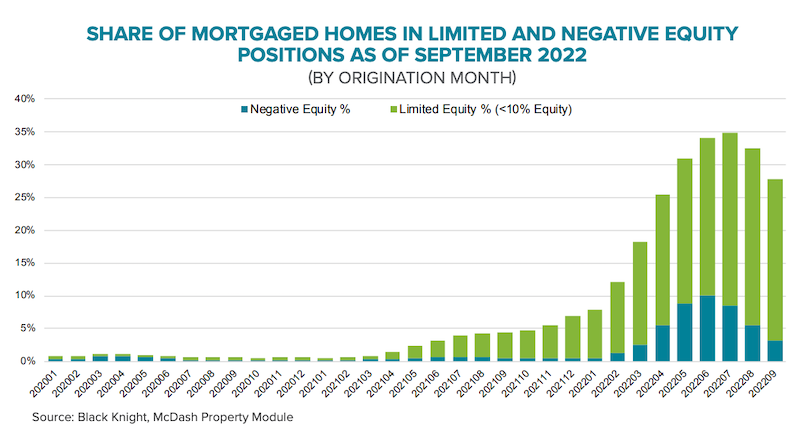

1 million homes have limited equity

In addition to the underwater homes, one million homes purchased in 2022 have less than 10% equity. This means that even a small drop in the value of these homes could push them underwater as well.

Compare that to homes purchased in 2021 where "fewer than 1% of homes mortgaged are currently underwater with only 3% having limited equity."

Black Knight data reports that most limited-equity homes were purchased in May-July 2022, the peak of the real estate market.

Equity positions for homes purchased before 2022

While the data is concerning for homeowners who bought in 2022, most earlier buyers maintain positive equity in their homes.

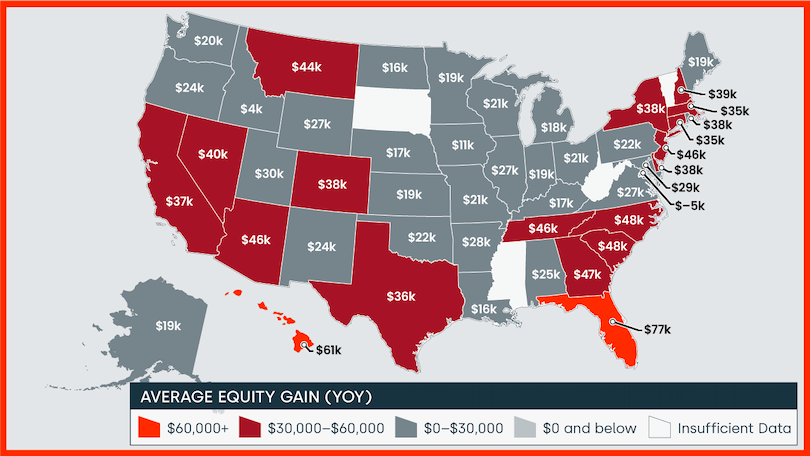

According to the CoreLogic Homeowner Equity Insights report, "U.S. homeowners with mortgages have seen their equity increase by a total of over $2.2 trillion since the third quarter of 2021, a gain of 15.8% year over year."

Selma Hepp, CoreLogic's interim lead of the Office of the Chief Economist, says their data shows a slight increase in the average U.S. loan-to-value (LTV) ratio. But she adds: "Today’s homeowners are in a much better position to weather the current housing slowdown and a potential recession than they were 12 years ago."

In fact, the CoreLogic report says, "In the third quarter of 2022, the average homeowner gained approximately $34,300 in equity during the past year."

How does this compare to the Great Recession?

About one in four homes were underwater during the Great Recession, which lasted from December 2007 to June 2009.

Many homeowners couldn't make their mortgage payments and lost their homes. According to the report Underwater America by the Haas Institute, "From September 2008 through the end of 2013, approximately 4.9 million families lost their homes to foreclosure. Between 2010 and 2013, another 1.3 million families lost their homes to short sales."

The 2022 housing market is nowhere near that crisis level. In fact, data shows that "nationally, household equity reached 70% in the second quarter of 2022, the highest level in over 35 years." This, combined with a strong labor market, means the housing market is in a far better position than during the Great Recession.

How homeowners can insulate against financial stress in 2023

Homeowners who purchased homes in 2022 might have concerns after reading the Mortgage Monitor report. However, consumers can take steps to insulate themselves against financial strain:

- Stay put. Historically, homes appreciate over time. According to SFGate, "National appreciation values average around 3.5 to 3.8% per year." So even if you purchased at the housing market peak in 2022, your home is likely to appreciate over time and stop being underwater.

- Stockpile savings. Daniels recommends that homeowners keep an emergency of three to six months of expenses plus a separate home maintenance fund. "It's important to have cash on hand if you know that you're living in a house that's underwater," says Daniels. "That way, if you have to move for an unexpected reason or because of a job relocation, you have the cash on hand to bring to closing if necessary."

- Renovate. Consider renovating if you have cash on hand and plan to stay in the home for a while. A home renovation can increase the home's value, getting you closer to what you paid for it. The 35th annual Cost vs. Value report by Zonda shows exterior home renovations that offer the best return on investment (ROI).

Final thoughts on underwater homes

If you have an underwater home or limited-equity home, your situation is likely to improve over time. The current situation is not nearly as as bad as the Great Recession. Still, it pays to be conservative with your money and not take on undue risks.