Home prices had seemed poised for a significant fall. Yet, a Redfin analysis found that after 11 weeks of decline, the median home sale price in the U.S. actually rose 1% during the 4-week period ending Sept. 25.

The reason? Mortgage rates, which topped 7% last week.

Rising borrowing costs might normally push prices down, but with mortgage rates at a 15-year high, 85% of mortgage-bearing homeowners are currently locked into a better rate than what they'd find on the market today.

Not surprisingly, many homeowners are postponing their selling plans, meaning fewer homes are coming on the market. The decline is well beyond what we'd normally expect to see each fall.

The latest realtor.com data shows that new listings are down 9.8% over the same period a year ago, and more than 20% since June.

The number of active listings, already grossly below pre-pandemic levels, has also leveled off after a sharp rise between April and July of this year.

"The plunge in new listings is hindering growth in housing supply, which is keeping home prices relatively high even though the market is slowing down," Redfin Deputy Chief Economist Taylor Marr said in a statement, noting that inventory tends to rise in a typical downturn.

With inventory remaining low, we now have a strange situation where home prices are rising even as demand keeps cooling off. The result is a market that's not particularly friendly to either buyers or sellers.

Higher home prices and mortgage rates shut out would-be buyers

At today's prices and rates, homebuyers will pay about 60% more in their monthly mortgage payments than if they’d bought the same home last September. Many first-time buyers have been priced out of homeownership entirely — some of whom had already gone under contract on a home.

Roughly 15% of home purchase agreements have fallen through over the past three months, according to Redfin. That's a level not seen since the start of the pandemic.

"Not everybody can afford a home in our current market, unfortunately," says Sean Gilliam, a realtor in northern Colorado. However, for those with the means, "there's less competition and less people buying homes."

Pending listings — the number of homes actively under contract — are down 23.7% over this time last year. Moreover, it's taking homes an average of seven days longer to go under contract.

"Since homes are sitting on the market for a while," comments Gilliam, "you're not in a rush anymore. You can stop and think about things." However, he cautions that you don't want to wait too long, since homes are still selling much faster than they did prior to the pandemic, when the average time on market was right around 65 days.

"It's still a seller's market, when you look at the numbers regarding months' supply of inventory," says Gilliam. "However, a lot of sellers are a little uncomfortable when their home sits on the market for a couple of weeks and it doesn't go under contract. As such, they do price reductions. They're offering concessions to help pay down rates for buyers. They're also very generous now as compared to before as far as inspection contingencies."

He adds: "I've also seen sellers do a lot just to accommodate buyers and get that home in great shape and make repairs as needed or offer credits towards closing costs. So, right now, the market is almost behaving like a buyer's market in that regard."

Sellers are indeed having to get more aggressive. The number of home sellers who dropped their asking price in September climbed to 19.5%, surpassing the share of price reductions seen at any time since 2018. Even so, many buyers remain priced out.

Home prices and interest rates being what they are, Giliam suggests that there are a limited number buyers who can benefit from the current market, including:

- Cash buyers, who don't need to worry about interest rates and can take advantage of the decreased competition

- Investors, who can buy and hold a property to rent it out, since rents tend to rise during a recession

- Buyers with a long-term plan, since they can take advantage of a fixed mortgage during a time when rents are likely to rise and home prices continue appreciate over the long-term

Those who plan to buy and sell within the next few years may want to hold off, suggests Gilliam, since level home price appreciation will make it difficult to turn a profit.

With buyers maxed out, will home prices finally come down?

While home prices in many markets have fallen from their peaks, some economists suggest that the lack of inventory is likely to keep prices from plummeting like they did in 2008. However, others are more bearish, hinting that prices could fall by as much as 20% in 2023.

In a recent commentary published by Barron's, economists Laurie Goodman and Michael Neal, both of the Urban Institute, suggest that "the state of the economy rather than housing affordability is a larger driver of home price changes."

They note that homes have depreciated nationwide only two times since 1976. The first was in the early 1990s, and the second was during the Great Recession, both recessionary periods when interest rates declined. However, neither period had today's inventory crunch — an important factor they say will likely keep home prices high, even amid slowing economic activity.

The researchers also note that since rent rates trend upward during a recession, locking in a fixed monthly mortgage payment could entice more buyers to the market and rekindle demand.

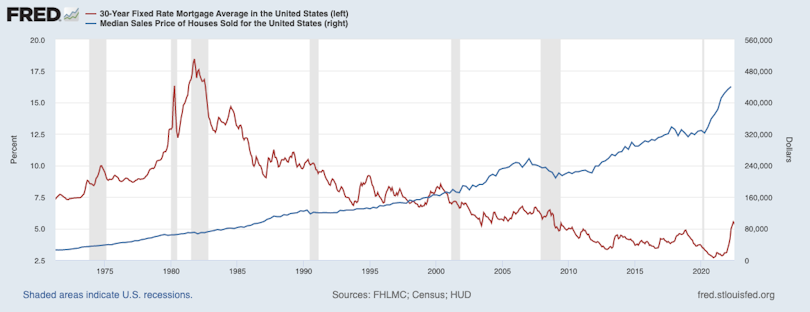

Looking at long-term trends, home prices have certainly risen as interest rates have fallen over the past several decades. However, going back over 50 years of mortgage history, it's hard to spot the reverse trend. For the most part, home prices have appreciated fairly consistently over the long term, even at times when rates have spiked to 7.5% or above.

Home prices vs. mortgage rates, 1970–present

That said, Goodman and Neal's analysis does show that in the two periods when mortgage rates rose more than 1.5% within a year, home price appreciation did slow considerably:

- From 12.9% to 1.1% between September 1979 and March 1982

- From 3.2% to 2.6% between September 1994 and February 1995

While we may not be in for a drastic price drop, homebuyers can at the very least expect some price stability compared to previous years. Buyers should also look forward to an eventual easing in interest rates once inflation is brought back under control, which economists at ING suggest could happen by the end of 2023 (though we may be in for a recession beforehand).

"Towards the end of a recession, mortgage rates tend to drop, sometimes rather significantly," says Gilliam. "On average, it's about 1.8 points."

He suggests buying a home "assuming those mortgage rates will never go lower. But look for that opportunity down the road and then you can refinance to a lower rate and free up that much more of your monthly income."