Title insurance protects homeowners and lenders from issues related to the legal ownership of a home. Below, we cover how title insurance works, who pays for it, and if you should get it.

A title insurance policy protects its owner against disputes over who owns a piece of property. So if there’s a clerical error in the ownership records, or if a previous owner has unpaid property taxes, this policy pays the cost to defend your ownership claim in court or even reimburse you for the cost of your home.

There are two different types of title insurance policies:

- Lender's title insurance, which protects the mortgage lender

- Owner's title insurance, which protects the homeowner

Buyers usually pay for the lender's policy, which is almost always required if they're getting a mortgage. On the other hand, owner's policies are 100% optional — but usually a good idea! In some locations, it’s conventional for the buyer to pay for an owner’s policy; in other areas, it’s more common for the seller to cover this cost.

The cost of both title insurance policies — the lender’s and the owner’s — typically adds up to around 0.5% of the purchase price of the home. However, depending on your home's value and location, this cost could range from a flat rate of a few hundred dollars to more than 1%.

JUMP TO SECTION

- How title insurance works

- Do you need title insurance?

- How are title insurance premiums calculated?

- How long does a title insurance policy last?

- Who pays for title insurance?

- Should you get title insurance?

- What title insurance does not cover

How title insurance works

Before we get into the details of how title insurance works, we need to cover what a title is and what happens behind the scenes when you purchase one of these policies.

What is a property title?

A property title consists of many legal documents that specify who is the rightful owner. It is more than just a piece of paper that verifies your ownership (that’s a document called the "deed"). A home's title includes a history of the chain of ownership and information about any "liens," outstanding debts, on the property.

What do title companies do?

When you buy a home, you typically pay a title company to verify that the seller has clear title to their home — that is, that they have the legal right to sell you the property without any challenges to their rightful ownership.

What is a title search

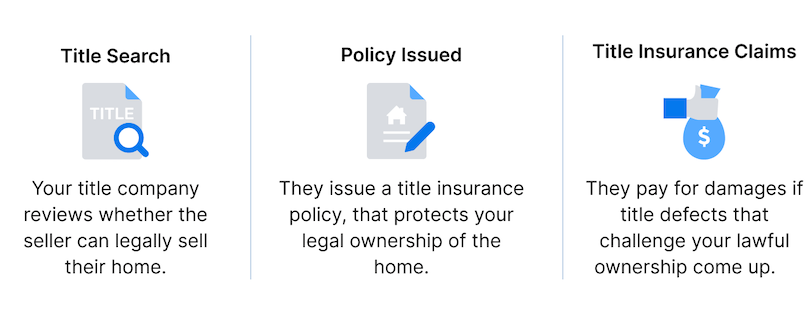

To confirm the seller's ownership, title companies perform what's called a "title search." During the title search, the title company researches legal documents to identify anything that might prevent the seller from transferring their ownership to you, the buyer.

Issues with the seller’s rightful ownership are commonly called "title defects" or "clouds on title." Title defects are fairly common, but the seller is usually able to correct them and continue the sale. Some of the most common title defects include:

- Unpaid property taxes

- Liens against the property

- Clerical errors related to the property title

» MORE: Title Companies and Closing Agents: The Ultimate Guide

What is a lien in real estate?

A lien is a claim of monetary interest in a piece of property. Liens are typically filed and recorded with the county.

The most common example of a liens in real estate is a mortgage; however, there may also be liens for other home loans, property taxes, and contractor work (mechanic's liens).

Unfortunately, a title search might overlook some crucial issues with the title. This is where title insurance comes in!

Title insurance protects you from challenges to your legal ownership of your home when someone brings up a claim that wasn’t revealed during the title search. Most often, these claims relate to errors in the public records, undisclosed liens, and illegal deeds (meaning a previous owner wasn't eligible to own their home — for example, if they were a minor).

When someone files a claim against your title, your policy will pay for any legal expenses necessary to defend your right to ownership in court. Title insurance will reimburse you for any financial losses that result from a covered claim up to the full purchase price of the home.

One way to think about a title insurance policy: it’s basically the title company placing a "bet" that it caught all possible issues during the title search.

Do you need title insurance?

Most home buyers have to get a lender's title insurance policy as a condition of their mortgage. Lenders require this to protect their interest in your home in case there are any issues with its title.

On the other hand, owner's title insurance is optional. However, it's strongly recommended that you opt for one of these policies as they’re often well worth the cost.

How are title insurance premiums calculated?

Title insurance costs are based on two things: your home's value and its location.

Title insurance policies are typically priced based on a percentage of your home's value. However, this percentage is usually not fixed. If your home is more expensive, you'll probably pay a slightly lower rate.

In addition to home value, title insurance premiums also vary by location. This is because, in most cases, your state's insurance commissioner regulates the title insurance premiums in your area. And since each state has slightly different standards for how title insurance companies can set their rates, where you live has a big impact on your premiums.

» CALCULATE: Title Insurance Costs

How long does a title insurance policy last?

Title insurance policies generally don’t expire. They cover you until you sell the home or, if you’re a mortgage lender, until the mortgage is fully repaid. Owner's title policies pass onto anyone that inherits your home as well.

Who pays for title insurance?

Usually, when you're a home buyer, you're expected to pay for the lender’s title policy.

In contrast, the question of who pays for the owner's title insurance depends largely on where you're located. In some areas, it’s more common for the buyer to pay for their own title insurance. In other areas, it’s conventional for the seller to pay for the buyer's owner's policy.

That said, who actually pays will ultimately come down to what the buyer and seller negotiate. Even if it’s common for the buyer to pay in your area, you could always try to get the seller to cover all — or just a portion — of the cost.

According to our research, this is who's expected to pay for owner's title insurance in each state:

| State | Who pays for owner's title insurance |

|---|---|

| Alabama | Buyer |

| Alaska | Seller |

| Arizona | Seller |

| Arkansas | Split |

| California | Seller |

| Colorado | Seller |

| Connecticut | Buyer |

| Delaware | Buyer |

| Florida | Seller |

| Georgia | Seller |

| Hawaii | Split |

| Idaho | Seller |

| Illinois | Seller |

| Indiana | Seller |

| Iowa | Buyer |

| Kansas | Seller |

| Kentucky | Buyer |

| Louisiana | Buyer |

| Maine | Buyer |

| Maryland | Buyer |

| Massachusetts | Buyer |

| Michigan | Seller |

| Minnesota | Buyer |

| Mississippi | Seller |

| Missouri | Seller |

| Montana | Seller |

| Nebraska | Split |

| Nevada | Seller |

| New Hampshire | Buyer |

| New Jersey | Buyer |

| New Mexico | Seller |

| New York | Buyer |

| North Carolina | Seller |

| North Dakota | Split |

| Ohio | Seller |

| Oklahoma | Buyer |

| Oregon | Seller |

| Pennsylvania | Buyer |

| Rhode Island | Buyer |

| South Carolina | Seller |

| South Dakota | Seller |

| Tennessee | Seller |

| Texas | Seller |

| Utah | Seller |

| Vermont | Buyer |

| Virginia | Buyer |

| Washington | Seller |

| Washington D.C. | Buyer |

| West Virginia | Buyer |

| Wisconsin | Seller |

| Wyoming | Seller |

Should you get title insurance?

If you're buying a home, it's recommended that you get an owner's title insurance policy.

If you'd be paying out of pocket for a policy and are weighing the cost, our advice is that it’s worth getting for the following reasons:

- Title insurance is a one-time cost. Unlike homeowner's insurance — which you have to continuously pay — title insurance covers you as long as you own the home.

- Not having title insurance (if you ever needed it) could be disastrous. Although the likelihood of this is fairly low, the cost of being uninsured if the home you're purchasing has an unknown title defect is astronomical. You could potentially lose your home, along with any of the equity you've built.

Note that in many areas, it's common practice for sellers to pay for the owner's title insurance policy. If you live in one of these areas, you probably don't have to consider purchasing one of these policies because it won't represent any additional cost.

What title insurance does not cover

While title insurance protects your ownership stake in your home, it doesn't protect your actual, physical home.

Damage caused to your home by a fire, vandalism, or weather would be covered by your homeowner's insurance policy — which home buyers are also required to purchase — not your title insurance policy!