| ✍️ Editor's note: We strive to provide objective, independent advice. When you decide to use a product or service we link to, we may earn a commission. Learn more. |

This guide contains everything you need to know to buy an apartment building and decide if it's a good investment for you.

For most new investors, buying an apartment building might seem like a daunting task that's too difficult or expensive to achieve. I used to think that myself, until I closed on my first 12-unit apartment building. I realized that the whole process isn't much different than the process I'd already learned to buy a smaller rental property. The biggest benefit is the scale. With one purchase I was able to double my portfolio, while buying an asset with many tenants to mitigate the risk of a few vacant units hurting my cash flow.

While the barrier to entry may seem high, since some apartment complexes require down payments of $100,000 or more, not all apartments are that expensive. There are also some creative financing options that let you purchase an apartment with a down payment that's far less than what you might've thought was possible. In some cases you can actually buy with no money down.

Here's what you need to know about buying an apartment building, including how to find good deals.

If you're thinking about buying an apartment complex, Clever can help.

We've partnered top agents that specialize in investment property across the country, from major brands and top-rated local brokerages.

The agent we connect you with can help you find properties both on and off market, and walk you through the entire process.

Eligible buyers also earn cash back on all eligible purchases!

Getting matched with an agent is free and there's no obligation to move forward.

JUMP TO SECTION

- How much does it cost to buy an apartment building?

- Is it a good investment?

- How much money can I make as an owner?

- Pros and cons

- Step-by-step guide to buy a building

- Case study: Buying a 12-unit apartment building

- 5 pro tips on how to buy an apartment building

- FAQ

- Find buildings for sale

- Value an apartment complex

- Finance an apartment building

- Buy an investment property with no money down

How much does it cost to buy an apartment building?

The average cost of buying an apartment building depends on what you define as an apartment building. If you consider buying a duplex, triplex, or fourplex an apartment building, then the average cost goes down drastically. In my market I can buy a fourplex that cash flows for around $100,000. And if I was willing to live in the property, I could use an FHA loan and house hack by living in one of the units for only 3.5% down.

Banks will finance anything that's four units or less with a residential mortgage. Anything over four units needs a commercial loan. Personally, I draw the line in a similar fashion to the banks. I consider anything four units and under a "small apartment building" and anything larger more of an "apartment complex."

Apartment complexes can be tens of millions of dollars or more if you're buying huge high rises with hundreds of units. However, there is a middle ground of smaller apartment complexes that are bigger than a fourplex but still affordable enough for most investors.

This table shows the average cost you can expect to pay for an apartment building. Note that well over 50% of all apartment buildings sold for less than $1 million in the last 24 months.

| Values and sold prices (last 24 months) | United States |

|---|---|

| Average price/sq. ft. | $1,684 |

| Average sold price | $1,598,091 |

| Median sold price | $238,400 |

| Number of sales | 329,305 |

| Number of sales over $250k | 160,131 |

| Number of sales over $1M | 46,669 |

| Number of sales over $10M | 7,659 |

| Average total tax amount | $31,708 |

| Average assessed value | $758,959 |

| Average market value | $1,205,696 |

Data from Reonomy

Is buying an apartment building a good investment?

The important thing to consider when making any investment is the risk-adjusted return — the amount of money you can hope to make in the face of the risk you take on. Overall, apartment buildings have a great risk-adjusted return. But this varies for each property, usually based on the purchase price that you buy the apartment for.

In short: Apartment buildings in general are good investments, but not every individual apartment building is a good investment. Would-be investors must exercise caution when evaluating a property and take into account many factors, including the condition of the property, price relative to other similar properties, local real estate trends, and rental vs. ownership demand in the area. The easiest way to do this is with a rental property calculator that lets you forecast the returns you can expect from purchasing a particular apartment complex.

However, people always need a place to live, and renting an apartment is often the most affordable housing option. There is currently a shortage of affordable housing in most American cities, which bodes well for owners of apartment complexes that offer affordable to mid-level housing. On the other hand, there is currently a large number of new luxury apartments being built, and those will be the first to reduce rent or go vacant if the economy dips.

How much money can you make owning an apartment complex?

There are four primary ways to make money owning an apartment complex:

- Rental income: After you cover all of your expenses, what you have left over is cash flow that you can spend as you please.

- Property appreciation: This is often where the majority of the money is made, as apartment buildings have been growing in value rapidly in the last 10 years. Some investors are even willing to buy a building that just breaks even on cashflow with rent because they're confident they will make a great return on their investment with appreciation.

- Leverage: If you borrow a million dollars from the bank at 4% and use it to buy an apartment complex with an 8% cap rate (return on investment), you can profit off the difference. If you do this with millions of dollars, you can generate a tremendous return.

- Tax benefits: Real estate is one of the most tax-advantaged investments. You can depreciate your investments and write off the interest you pay in your mortgage.

You can learn more about the four ways to generate income from real estate in our real estate investing guide.

How much money you can make from investing in apartment buildings depends on how big of an investment you make. Generally speaking, you can expect a 4–10% cap rate when you purchase an apartment.

Pros of investing in an apartment building

- High earning potential: You can grow your portfolio faster by buying one large apartment than you can with single-family rentals.

- Dependable cash flow: Apartment buildings provide a reliable income stream. If some of your units are vacant or tenants aren't paying, you still have other units that are paying that cover your expenses.

- Appreciating asset: Like all real estate, apartment buildings are an appreciating asset. If you no longer want to run your complex, you can sell it for a profit after a few years.

Cons of investing in an apartment building

- Harder to diversify your market exposure: Apartment buildings can be expensive, and it's hard for new investors to buy a lot of them. This means that it's hard to diversify your portfolio in different market classes.

- Higher turnover rate: Single-family properties usually have longer-term renters. Since apartment buildings have to deal with more resident turnover, owners need to spend more time finding new renters and getting their units ready for new residents.

- Large down payment: Buying an apartment building usually isn't cheap and often requires a hefty down payment. The required down payment for a multi-family property is usually higher than the down payment for single-family rental properties.

12 steps to buy an apartment building

If you're looking to buy an apartment complex, you can follow this 12-step guide:

- Set your goals: If you don't know where you're going, you will never get there. Ask yourself what you want to achieve from owning an apartment complex, and then work backward to figure out how much income you need to generate.

- Set your budget: Establish an amount that you're willing to spend buying an apartment complex. Make sure you leave enough cash on hand for repairs, and keep your portfolio diverse. It's not a great idea to put over 50% of your investment portfolio in one property.

- Learn how to forecast cash flow: This is where a renal property calculator comes in handy. You should be able to model prospective deals so you know where to focus your time and energy.

- Choose a market: I recommend that you start by looking in your local market and modeling a few deals to see if it's feasible before you start looking out of state. It's much easier to manage something you can drive to, and you can be more confident that you understand the dynamics of the neighborhood.

- Get pre-approved for financing: Talk to at least three lenders and compare their products and rates. It's a good idea to get pre-approved with at least two so you can get detailed quotes to compare once you find your property.

- Start looking for properties: You can use popular real estate apps to find deals, like DealMachine. This app helps investors find and research distressed homes (foreclosures, pre-foreclosures, short-sales, etc.) and get in touch with motivated owners fast via batch skip tracing and direct mail campaigns. You can also look on the MLS, LoopNet, and other commercial real estate websites, as well as network with brokers that have off-market properties.

- Start making offers: Remember not to get emotional! These are investments, and you should only offer a number that makes sense for you, even if it's drastically lower than the list price.

- Make inspections: Make sure your apartment complex is in the same condition it was advertised in. Be sure to check the roof, HVAC, plumbing, and electrical systems, as those can be the most expensive if they need repairs.

- Choose a property management company: The management company you choose will make or break your investment. Be sure to interview at least three companies and hear real reviews from some of the current owners they manage property for.

- Lock in your financing: Go back to the same lenders that got you pre-approved, and bring the actual deal you found so you can compare rates. Pick a lender, and they'll take your personal financial statement and get you fully approved.

- Close: Congratulations! Get ready to sign a ton of paperwork, then take a moment to celebrate your accomplishments.

- Grow your portfolio: Once you stabilize your investment and are generating cash flow, it's time to repeat this process and start looking for your next investment!

For a more detailed explanation, you can read our guide on how to purchase investment property.

Case study: Buying a 12-unit apartment building

The picture above isn't pretty, but it's probably the best investment my partner and I have made to date. This is a 12-unit apartment complex that my partner and I bought a few years ago in rough shape, and we brought it back to life.

We purchased the building from an investor that had recently saved the building from being boarded up, but they didn't do much more than that. The units were in rough shape and had structural issues, leaking roofs, sewer issues, and damaged interiors.

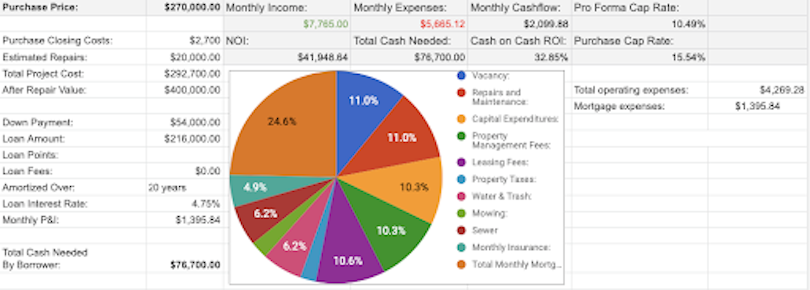

We bought the entire complex for around $270,000, or $22,500 per door. The moment we closed, we had our crew come in and put on new roofs, fix the sewers, redo the tuckpointing, and start renovating the apartments as they became vacant (three units were vacant, and two tenants weren't paying). Over the next year, we completed the renovations and raised the average rent from $550 to $650. By our calculations, we increased the value of this apartment complex by over 100%. We currently value this property at $600,000, and it cost only about $130,000 in renovations to get there.

This property now generates over $2,000 in cash flow for us after covering all our expenses.

5 pro tips to buying an apartment building

Convinced that an apartment complex is the right investment for you? Here's five pro tips to help make the buying process move along smoothly.

1. Find deals by hunting for off-market properties

If you're serious about buying an apartment building, you need to find a good deal. Here are two ways:

Get real estate software: You can sign up for real estate investment software that focuses on helping investors buy off-market properties. Apps like DealMachine are useful tools for investors looking to find apartment buildings to flip, BRRRR, or wholesale.

How it works: As you're driving around town and spot a home that looks like it could be a great fixer-upper, you pull up the home on your DealMachine app, get detailed information about the home, and get the owner's contact information.

From there, you can call the owner to see if they're interested in selling, or you can instantly send them direct mail from the app.

DealMachine and other apps also offer batch skip tracing services, which helps investors find and contact the homeowners of off-market properties.

⚡ Get a seven-day free trial with DealMachine

Get an investor-friendly agent: Another idea is to hire a real estate agent who's focused on helping investors. They'll have access to a lot of sellers who want to sell but don't want to list their properties on the market.

If you're not sure where to find one of these agents, Clever can help.

If you're thinking about buying an investment property, Clever can help.

We've partnered top agents that specialize in investment properties across the country, from major brands and top-rated local brokerages.

The agent we connect you with can help you find properties both on and off market, and walk you through the entire process.

Best of all, in the states that allow it, you could get cash back after closing.

Getting matched with an agent is free and there's no obligation to move forward.

2. Choose your property type

There are quite a few types of apartment buildings: high-rises, mid-rises, garden-style, and walk-ups, among others. Make sure to evaluate the current real estate trends in your area before deciding which type to buy, since popularity varies by region. Your real estate agent can make recommendations based on what they see in their day-to-day work.

You also need to decide if you want a new apartment complex or one that will require some fixing up. You can generally find fixer-uppers for a better bargain, but they require a greater time investment and a keen eye for undervalued properties.

3. Visit multiple properties and do your homework

Don't buy the first property you see. Look into local demand, perform an inspection to get an idea of the condition of the apartment, and visit as many properties as possible.

The ratio of renters to owners in a region can be a good indicator of your investment's success probabilities. Cities with more renters than owners have more demand for apartments, so be sure to look into these statistics before making a purchase.

4. Understand the financial process and run the numbers

To buy an investment property, you'll have to make a 20% down payment, and you'll also need to pay for insurance, mortgage payments, maintenance and management costs, and marketing expenses.

Upkeep expenses can take a big bite out of your bottom line. Prior to buying a complex, look up the local going rate for some of the most common renovations, like repainting the exterior of the building and the interior of the apartments for when tenants move out.

Make sure that after all these expenses, you'll still be in the black. There's no worse situation to be in than owning a multi-million dollar apartment complex that loses you money every month.

5. Choose the right lender

There are three common types of loans for apartment buildings (not counting residential loans for buildings smaller than four units):

- Government-backed apartment loans: These loans offer high LTV (loan-to-value) ratios and have a range of $750,000 to $6 million. Fannie Mae, Freddie Mac, and the FHA offer this type of loan. Typical rates are 3.5–6%.

- Bank balance sheet apartment loans: Many local lenders love making loans to investors to buy apartments. You can expect loan terms of 20–25 years, with balloon payments ranging from 3 to 15 years, and interest rates between 3% and 6%.

- Short-term apartment financing options: These loans are meant to help investors compete with cash buyers by offering mortgages on short notice. Minimum loan amounts are $100,000, with LTVs up to 90%. Rates are high at 7.5–12%.

Once you decide what type of loan is right for you, begin researching each lender's offerings. Each bank and lender is different, so be sure to pore over all your options. A small rate increase can eat into your profits.

FAQ about buying an apartment building

Where do I find apartment buildings for sale?

Working with a real estate agent is the best way to find apartment buildings for sale. They can use their professional network and the MLS to monitor new listings and alert you of suitable properties for sale. Besides a real estate agent, you can find listings in the local paper and online.

For off-market properties, try using real estate software that helps you find good deals (e.g., foreclosures, pre-foreclosures, motivated sellers), and reach out to owners quickly. Examples of software include DealMachine and Propstream.

How do you value an apartment complex?

There are three ways to value an apartment building: the sales approach, the replacement approach, and the income approach. Of these, the income approach is the most common.

To determine an apartment's value using the income approach, start by finding the NOI. Multiply the monthly rent per unit by the number of units in the building, and subtract all operating expenses. Next, divide the NOI by the cap rate that's common in the properties location. You can find the cap rate by speaking with real estate agents in your area.

For example, if the NOI on the property is $30,000 and the cap rate is 0.12, the value of the property is $250,000.

How do you finance an apartment building?

To finance an apartment building, you need to find a lender that offers government-backed loans, bank balance sheet loans, or short-term financing options. The rates and maximum loan amounts vary depending on the type of loan. Compared to residential property lenders, commercial real estate lenders are more likely to base lending decisions on an applicant's real estate investment experience.

How can I buy an investment property with no money down?

In some cases, sellers are willing to offer seller financing for the entire purchase, or enough to cover the down payment with a commercial lender. Personally, I've had several sellers be willing to owner finance our down payment for three to five years so we can refinance, but I have yet to have a seller agree to owner finance the entire property.