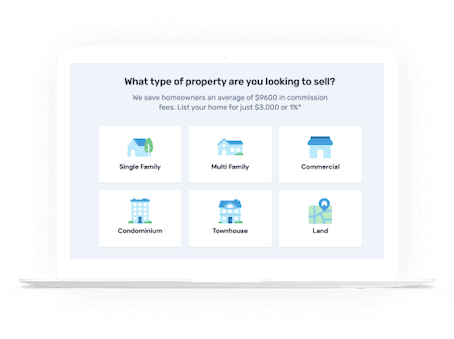

Compare top local real estate agents. Save thousands on commission.

Sell with a top agent for just a 1.5% listing fee. Clever’s service is free with no obligation. Get matched in minutes.

More than 20,000 people have bought or sold their home with Clever. We've helped them save over $140M in real estate fees.

Better Agents. Better Rates. Zero Hassle.

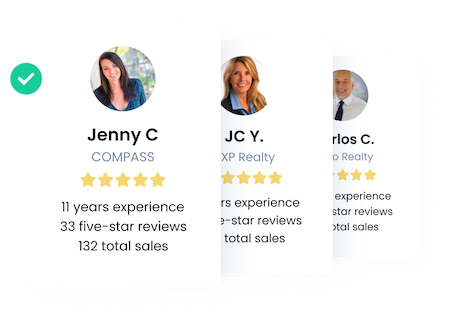

A nationwide network of 14,000 top agents

We partner with top-producing agents from all the major brands, like RE/MAX, eXp, and more. Agents have to maintain exceptional reviews to stay in our network.

The best rates in real estate

These agents have agreed to offer Clever customers our special rate: just a 1.5% listing fee ($3,000 minimum). You get top-producers for half their typical fee. Clever sellers save $7,000 on average!

Free with no obligation

Sign up and compare agent matches in minutes. Choose the best fit, request more matches, or walk away at any time. Clever’s service is completely free for you to use (our agents pay us a portion of their commission when they close a sale).

How Clever Works

Enter a few details to get started

Our Concierge Team will reach out within 5 minutes to answer your questions, offer advice, and learn exactly what you’re looking for in an agent. You can also call us directly at 833-2-CLEVER 7 days a week.

We negotiate better rates on your behalf

These aren’t discount agents. We bring you the best, full-service agents from major brands and brokerages nationwide. Since we send these agents more business at zero upfront cost to them, they’re willing to pass part of that savings along to you.

Choose the best agent for you

We decide which agents to recommend based on your specific goals and needs. You’ll get to meet each agent and decide for yourself. If you’re not 100% comfortable with your matches, you can request more agents or walk away at any time. You never owe us a dime.

Our team of licensed real estate experts is ready to help

We’re here to answer your questions, offer advice, and help you find the right agent — full concierge service, 7 days a week.

Contact our Concierge Team today!

Available 8am to 8pm EST (5am to 5pm PST)

12h 00m 00s

By clicking “Contact Us Now” I opt-in to receive calls, email, and SMS and agree to Clever’s Terms of Use, Privacy Policy, and Consent to Contact Customer. Message and data rates apply. Message frequency varies. Text STOP to cancel. Text or call 1-833-225-3837 for help.

How much can I save with Clever?

Clever

Traditional

(usually 2.5 to 3%) still applies

Ready to save thousands on commission?

Here's how much cash back you'll get when you buy your next home with Clever

| When you... | Clever Cash Back™ |

|---|---|

| Buy with Clever | $250 |

| Buy and sell with Clever | $500 |

Our team of real estate experts is standing by to help you get the process started.

Why work with Clever?

Work with the best local agents

Save big on commissions

Sell your home faster

Choose from top local agents

Get money to help cover your move

Real-time MLS alerts and on-demand showings

Clever has helped thousands of happy home sellers and buyers

Ryan M Oconnor

Saved lots of money

Saved lots of money, quick response, great experience, professional realtors. highly recommend.

Linda Marr

Our realtor Sherill Douglas

Our realtor, Sherill Douglas, could not have been more helpful and knowledgeable. She was with us every step of the way, very patiently answering all of our questions and concerns. And getting everything done to get our house sold. We so appreciate all of her help...

Alyssa

I thought this was going to be a hoax…

I thought this was going to be a hoax after dealing with some other sites claiming to give you a fair price for your home. We were connected with Erica Quamme, and can honestly say it was the easiest and most positive experience we've had in selling our home...

Robert Pierce

A great selling experience!

Chris Doss was punctual, professional and provided excellent personal service. I highly recommend him. Thanks for a great experience!

Jennifer Z.

Charles Sparks is FANTASTIC!

Charles Sparks, our realtor, was FANTASTIC. He was very thorough in the listing prep, communication and really worked to sell our house not only quickly but with a full price offer. He was reasonable in his price suggestion and aggressive in his marketing...

Lisa B.

Clever is actually quite clever

Clever is actually quite clever! I had a great experience with the real estate agent they referred. She was professional, experienced, and enthusiastic and handled the sale of a unique property...

Meet your next real estate agent

JC Young

Carlos C.

Cathy C.

Nathan L.

All of our partner agents are...

Frequently Asked Questions About Clever

Is Clever really free?

Yes! Clever’s service is 100% free and there’s never any obligation to sign or move forward with one of our recommendations. Interview as many agents as you’d like until you find the perfect match. When you sell with Clever, you’ll only pay your reduced fee if and when your home actually sells. If you’re buying, you won’t pay a dime.

Why do agents work with Clever and offer discounts and cash back?

We know you’re excited to get teamed up with a top agent — and rest assured, our agents are just as excited to be working with you.

Clever works with more than 14,000 agents across the country from major brands and top regional brokerages, like Keller Williams, Century 21, RE/MAX, and more. We provide our partners with a steady stream of new business so they can focus their attention on doing what they do best: Selling and buying homes.

Because we help them save on the typical cost of finding new clients, they’re able to pass those savings along to you in the form of a reduced listing fee or home buyer rebate.

Is Clever’s service available in my area?

Yes! Clever’s service is available in all 50 U.S. states and Washington, D.C. We partner with thousands of top-rated real estate agents nationwide to help you save thousands when buying or selling a home.

Get in touch to learn more and get started! Submit your info via the link below and we’ll help you set up a preliminary consultation with a top-performing agent in your area. Remember, the referral is 100% free and there’s never an obligation to sign or move forward.

Clever makes finding the perfect agent easy

Finding a seller's agent with Clever

Finding a seller's agent on your own

Finding a buyer's agent with Clever

Finding a buyer's agent on your own

We have licensed experts standing by to help

By clicking “Contact Us Now” I opt-in to receive calls, email, and SMS and agree to Clever’s Terms of Use, Privacy Policy, and Consent to Contact Customer. Message and data rates apply. Message frequency varies. Text STOP to cancel. Text or call 1-833-225-3837 for help.