What is Knock? | Should you use Knock? | Knock reviews | How the Knock Bridge Loan works | Fees | Eligibility | Locations | Alternatives

The Knock Bridge Loan program (formerly called Knock Home Swap) allows home sellers to access a portion of their current home equity to purchase a new home before they sell. The program offers an alternative to having to sell your home first in order to unlock the cash for a new down payment.

As part of their bridge loan, Knock offers up to $35,000 in interest-free funding to help you get your home ready to list and provides a guaranteed backup offer in case your home doesn't sell within six months.

While reviews for knock.com are overwhelmingly positive, a potential drawback is the additional fee. You'll pay a 2% service fee, plus $1,850 in closing costs for your bridge loan on top of traditional realtor fees and closing costs.

However, unlike some of its competitors, Knock lets you choose your own agent and mortgage lender — which can lead to both savings and peace of mind while navigating a complicated trade-in process.

What is Knock?

| Knock, at a glance | |

|---|---|

| 💰 Knock fees | 2% of new home’s purchase price + $1,850 for processing and underwriting |

| 🤝 Programs and services | Knock Bridge Loan, up to $500,000 |

| ⭐ Customer rating | 4.8/5 (810 reviews) |

| 📍 Locations | 75 metro areas across 18 states |

| ☎️ Contact | (866) 996-1695 |

Launched in 2015 by the founders of Trulia, Knock addresses the tricky timing issues homeowners face when selling and buying a new home at the same time.

By advancing sellers a portion of their home's equity before selling, Knock allows them to purchase and move into a new home while before selling their old one.

In 2017, Knock raised a total of $44.5 million in combined Series A and Series D funding.[1] At the time, Knock distinguished itself from other iBuyers by encouraging customers to sell their old homes on the open market. Unlike Opendoor and Offerpad, which make cash offers on homes, Knock planned to purchase just 10–20% of customers’ homes.

» LEARN: What's an iBuyer?

With time, Knock's emphasis on open-market sales grew. In June 2020, Knock began expanding its partnerships with established brokerages and local real estate agents. As of November 2020, Knock's network featured 40 brokerage firms with more than 27,000 agents.[2] From 2021 to 2023, Knock rapidly expanded from 15 to 75 metros.

Today, Knock declines to provide specific data but emphasizes that most customers sell their homes on the open market. This is generally good for customers, who have the potential to receive more than their asking price in competitive markets. If a home fails to sell after six months, Knock will still provide a backup offer equivalent to 80% of the home's fair market value.

Looking for Knock.com reviews from customers? Find them here!

How Knock's Bridge Loan works

Knock's Bridge Loan can help you make a more competitive offer on a new home, while avoiding the financial burden of paying two mortgages during a simultaneous home sale and purchase.

Through Knock, you get access to an interest-free bridge loan of up to $500,000, which you can use on top of your new mortgage loan.[3] The exact loan amount will depend on how much equity you have in your old home and how much you plan to put down on a new home.

The bridge loan can be used to cover several items:

- Down payment (up to 20%) on a new home

- Up to six months of mortgage payments on your old home

- $35,000 toward repairs or improvements to your old home

- Moving expenses

While Knock provides the bridge loan directly, you can choose to work with Knock or another lender of your choosing for your new mortgage, if you need one.

Applying for Knock Home Swap is free, and you're under no obligation to move forward.

How to sell your home with the Knock Bridge Loan

Step 1. See if you qualify at knock.com.

Knock starts the process by evaluating your current home. To see if you qualify, Knock will need your address, estimated home value, and estimated mortgage balance.

You can provide this information yourself or refer them to your mortgage lender.

If you qualify for the program, you’ll complete a formal loan application and submit official documentation so Knock can prepare a bridge loan estimate and backup offer amount.

Step 2. Purchase and move into a new home.

If you decide to move forward with Knock, you'll begin your home search knowing that you can make a non-contingent offer on the home of your choice.

Once you close on your new home, Knock will take over the mortgage payments on your old home, so you won’t have to cover two monthly payments at once.

Step 3. Prepare, list, and sell your old home.

Once your home is vacant, you'll have 45 days to make any repairs or improvements, using up to $35,000 in interest-free funding from Knock to cover the costs. You can tap Knock’s network of contractors or find one on your own.

When your home is ready, your real estate agent will start the process of listing, marketing, and showing your old home, just as they would in a traditional sale.

You'll have six months to find a buyer — which gives you an opportunity to get the most competitive offer possible.

If your home doesn't sell on the open market, you can always accept Knock's backup offer, which is typically 80% of fair market value.

Step 4. Settle your bill.

You won't have to pay Knock's fees until you sell your home. When you receive the proceeds from your home sale, Knock will deduct its interest-free Home Swap loan and service fees.

Keep in mind that you'll also need to cover all of the usual expenses associated with selling a home, including realtor commission and closing costs.

» JUMP: See your all-in costs for using Knock

What to watch out for

Knock's Home Swap program comes with a few caveats.

First, Knock will hold your home as collateral until it sells. When you use Knock Home Swap, Knock will place a lien against your property until you pay the loan back in full through the proceeds from your home sale.

Second, Knock's backup offer will only cover 80% of your home's fair market value. If your home doesn't sell after six months, you can choose to accept Knock's cash offer as a last resort — but you'll end up getting far less than your asking price.

Finally, Knock won’t give you the cash from your bridge loan outright — instead, it will pay approved expenses like mortgage payments and repair bills on your behalf.

Am I eligible for the Knock Bridge Loan?

In a nutshell, Knock has to make the numbers work before agreeing to work with you. You’ll have to qualify for a conventional mortgage — and the expected proceeds from selling your old home will have to cover the loans and services Knock is providing.

Knock requires customers to complete two screening processes:

- Pre-qualification, which estimates the approximate size of your loan

- Pre-approval, during which Knock specifies the terms of your loan

Because Knock expects customers to sell their old homes on the open market within six months, the company also takes your old home into consideration. The criteria is flexible, but Knock typically wants to work with sellers who:

- Plan to sell and purchase a primary residence (not a vacation home or rental property)

- Currently live in a single-family home, in good condition

- Live within a current service area

Knock might deem your home ineligible if you:[4]

- Live in a condo, manufactured home, multi-family unit, or 55+ community

- Have significant water damage or foundation damage

- Lack recent, similar sales data in your area

- Have unpermitted additions

Additionally, Knock doesn't currently accept distressed or bank-owned homes. In these situations, we recommend working with an experienced real estate agent who can showcase your home to the right buyers in your area.

» CONNECT: Find a great local agent and save thousands with Clever!

Should you use Knock?

✅ You may want to use Knock’s Home Swap program if…

|

❌ You may want to avoid Knock’s Home Swap service if…

|

If you don't have a lot of cash on hand for a down payment, it can be hard to afford a new home until you sell your old one. Knock closes the buy/sell gap by fronting you a portion of your current home quity — its market value minus what you owe on the mortgage — to let you move into a new home while they cover the costs of listing and selling your old one.

Knock is a particularly useful option if you are concerned about missing out on your dream home due to a competitive market. Through their equity advance, Knock lets you remove the usual contingencies around selling your home — making your offer far more attractive to a seller.

Knock also provides up to $35,000 in interest-free funds for repairs and cosmetic updates to help you sell your home for more.

As an added benefit, Knock lets you work with your own real estate agent to buy and sell — something competitors like Orchard and Flyhomes don't allow.

Customer reviews indicate that Knock Home Swap reduces the stress of selling and buying a home. The trade-off is that you'll have to pay Knock a service fee on top of the commission you pay to your agent.

Knock's convenience comes at a slightly higher cost

As a bridge loan provider, Knock charges a a 2% service fee, plus approximately $1,850 in closing costs.

While Knock's Home Swap service negates the risk of having to pay two mortgages at once, you'll eventually have to pay Knock back for carrying the costs of your old home while it sells. The company's expenses will be deducted from your proceeds at closing.

You should also know that Knock's backup offer will only cover about 80% of its fair market value — if you're unable to find another buyer, you'll take a financial hit.

Where you CAN save is in using Knock with an agent from a reputable low-commission real estate brokerage.

Try Clever today! Compare top local agents, list your home for just 1.5%. Our service is free with no obligation. Get your matches in minutes.

How does Knock compare to alternatives?

Knock isn’t the only home trade-in service on the market. Since 2017, Orchard (formerly called Perch) has offered similar services.

iBuyers like Opendoor have also begun to offer similar trade-in services to supplement their cash-offer services.

Knock vs. Orchard

| Criteria | Knock | Orchard |

|---|---|---|

| ⭐ Average customer rating | 4.8 | 4.8 |

| 📍 Locations | 75 metros across AZ, CA, CO, FL, GA, IL, MD, MI, MN, NJ, NC, OH, OR, PA, SC, TN, TX, WA | 11 metros across CO, GA, MD, NC, OR, TX, VA |

| 🧑💼 Choose your own agent? | ✅ | No |

| 💰 Choose your own lender? | ✅ | ✅ |

| 🚚 Move first | ✅ | ✅ |

| 🛠️ Assistance with repairs | ✅ | ✅ |

| 🔒 Backup offer | ✅ | ✅ |

Like Knock, Orchard offers an equity advance on your current home to cover the down payment on a new one, letting you move in right away while it lists and sells your home. Orchard also provides interest-free funding to make repairs and a guaranteed backup offer if your home doesn't sell within 120 days.

While Orchard requires you to work with its team of agents and transaction coordinators, its all-inclusive 6% fee means you won't have to pay a separate agent commission. Orchard also allows you to choose your own lender.

Orchard really sets itself apart from Knock by giving you access to as much as 90% of your home's equity before you sell. On a $500,000 house, that's $450,000 in equity to put towards a down payment and related costs.

By comparison, Knock caps its bridge loan at $500,000. If you need more to cover your down payment, buyer closing costs, or repairs and mortgage on your previous home, you'll need to come up with the cash yourself.

With Knock, the sale and purchase happen in a single transaction: Knock holds your old home as collateral until it sells.

Knock vs. iBuyers

By positioning itself as a lender, Knock distanced itself from iBuyers — companies that use technology and in-house real estate expertise to make cash offers on homes.

There are two key differences between Knock and iBuyers:

- Offer price on your old home

- Speed

Knock customers work with real estate agents to sell their homes on the open market. This allows you to potentially receive more than your asking price — or at least a competitive offer.

By contrast, iBuyers typically offer fair market value AT MOST. You won’t have much room to negotiate.

On the flip side, iBuyers can move much faster than Knock. For example, Opendoor can provide an initial cash offer within 24–48 hours, and you can close on your home in as little as 14 days. However, it won't be as much as you could get on the open market.

We recommend comparing cash offers from multiple iBuyers if you're looking for a quick cash sale. You can do this using Clever Offers. A top local agent will present you with offers and tell you what your home is actually worth so you can make sure you're getting a good deal.

Compare offers from top companies like Opendoor to the sale price you'd get with an agent.

Knock Home Swap fees

We estimate that it'll cost you 9.5–16.25%, plus $1,850 in loan fees, to use Knock Home Swap. On a trade-in of two homes valued at $600,000, that equates to $58,850–98,950. You'll also need to reimburse Knock for any funds borrowed for repairs, up to $35,000.

Knock's fees, plus your mortgage payoff and bridge loan, will be deducted from your final proceeds.

Keep in mind that you’ll also have to pay the typical closing costs and realtor commissions.

To compare, trading the same two $600,000 homes using Orchard would cost between $54,000–84,000 (9–14%), plus deductions for any home repairs made prior to listing.

You can save thousands in listing fees using Clever to find your agent

Knock stands out from competitors by allowing you to work with any agent you like. This way, you can work with someone you trust while saving considerably on commission.

Clever's free service connects you with top local agents who guide you through the selling process for a 1.5% commission. You can compare and interview multiple agents, with no obligation to use their services.

If you use one of Clever's partner agents to represent you, your all-in costs on a $600,000 home swap go down by 2% ($12,000). Plus, Clever offers eligible buyers cash back at closing — helping you maximize savings while taking full advantage of the benefits of Knock Home Swap.

Clever can help you keep more money in your pocket at closing!

With Clever:

✅ Sellers pay only 1.5% in listing fees

✅ Buyers earn cash back on eligible purchases

✅ You'll work with a local realtor from top brokers, like RE/MAX and Keller Williams

Clever's service is 100% free, with zero obligation. You can interview as many agents as you like, or walk away at any time. Enter your zip code to find a top local agent today!

Knock reviews

Knock has an average rating of 4.8 across 810 reviews.

While most customers praise Knock for its ease, transparency, and quality of customer service, a small minority of reviews cite delayed closings caused by poor communication and disorganization on the part of the company.

Knock isn’t currently accredited by the Better Business Bureau but has a B+ rating, with 13 complaints as of December 2023.

| Site | Average review |

|---|---|

| Zillow | 4.8 across 738 reviews |

| Trustpilot | 4.3 across 55 reviews |

| BBB | 4.35 across 17 reviews |

| Weighted average rating | 4.8 across 810 reviews |

Positive Knock reviews

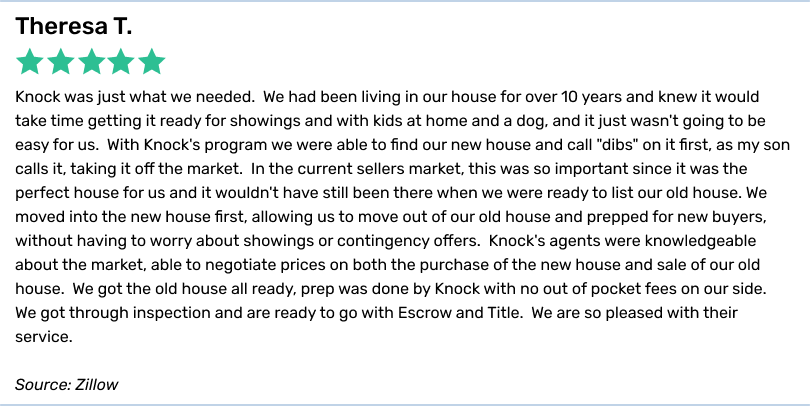

Home sellers appreciate Knock Home Swap's convenience — especially in highly competitive markets. Knock trade-in reviews emphasize the benefits of making a cash-like offer on a new home, avoiding disruptive showings, and getting extra time to prep their old homes after moving out.

Help in a competitive market

On the positive side, Knock's Home Swap allowed Theresa T. to secure her dream home in a tough market.

Less stress than a traditional home sale

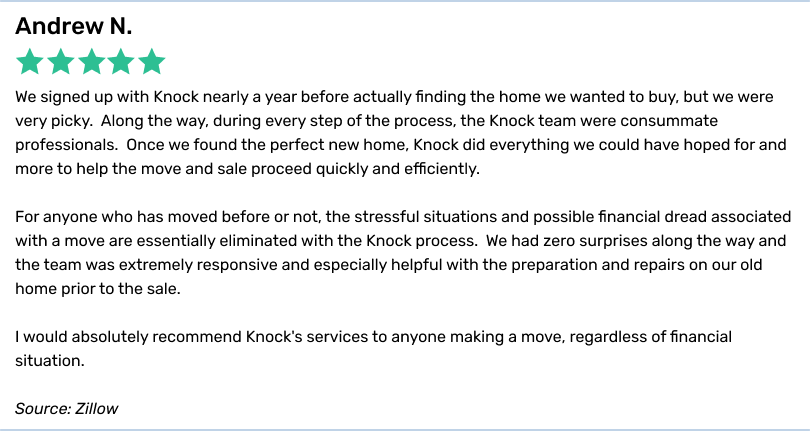

Andrew N. was impressed by Knock's customer service, which greatly reduced the stress of purchasing a new home.

Knock complaints

While Knock reviews skew positive, a few pointed customer reviews reveal that there’s room for improvement in the company's communication and customer service.

Unexplained delays right before closing

This customer feared losing out on a new home because of a closing delay caused by Knock's disorganization and lack of communication, noting last-minute requests for loan documents that had already been delivered.

Costly miscommunication

This customer was told late in the process that they would need to come up with extra cash at closing, resulting in their needing to put less money down than the 20% they originally intended. A down payment of 20% would have allowed them to avoid paying for private mortgage insurance (PMI).

While Knock indicated that the customer would be able to use the money from their home sale to quickly make up for the lesser down payment — allowing them to revise their loan terms to remove the PMI after 60 days — that ended up not being the case. Instead, Knock immediately sold the loan to another creditor with steeper requirements for removing the PMI.

While selling loans in the secondary market is common practice in mortgage lending, the miscommunication on Knock's part cost the home seller hundreds of dollars in extra appraisal fees and PMI — not to mention a lot of added stress.

A real estate agent can make or break your transaction

When buying and selling, you want the right team in your corner. This is especially true in a complicated transaction like a home swap, where you're managing negotiations, closing dates, loan paperwork, requests from the title company, and more all at once.

It's important to choose a realtor who knows the ins and outs of the local real estate market and will stay on top of the transaction from start to finish.

At Clever, we match home buyers and sellers with top agents from some of the country's best-known brokerages, who work for a pre-negotiated commission of 1.5%.

Through our matching service, agents save considerably on time and marketing costs to find new clients while you save thousands of dollars on commission.

Find top-rated agents from local brokerages and get a pre-negotiated 1.5% listing fee.

Clever's service is 100% free, with zero obligation. Interview as many agents as you like until you find the perfect fit — or walk away at any time.

Is Knock available near you?

Knock currently offers its Home Swap in over 75 markets across the U.S.[5]

Knock has a relatively large service footprint, operating in major metros across 18 states. Its closest competitor, Orchard, is available in just 7 states.

If you live within one of Knock's eligible service areas, you can apply for financing just as you would with any other lender.

| Company | States where it operates |

|---|---|

| Knock | AZ, CA, CO, FL, GA, IL, MD, MI, MN, NJ, NC, OH, OR, PA, SC, TN, TX, WA |

| Orchard | CO, GA, MD, NC, OR, TX, VA |

| Opendoor | AL, AZ, CA, CO, FL, GA, ID, IN, MN, MO, NV, NJ, NY, NC, OH, OK, OR, SC, TN, TX, UT, VA, WA, DC |

» Not available near you? Find the best Knock alternatives.

FAQs about Knock

Is Knock.com legit?

Yes, Knock is a legitimate business that offers loans to home buyers and sellers. Knock's Home Swap lets you make a competitive, cash-like offer on a new home before selling your old one. However, you'll still have to hire your own real estate agent. Compare low commission real estate companies to save thousands on your next sale.

How does Knock.com work?

Knock follows the same pre-approval process you'd use to secure a traditional mortgage. The key difference is that you can make a non-contingent offer on your new home BEFORE selling your old one. You can move right away, and Knock will cover your mortgage until you find a buyer. At the end, you'll settle your bill with the proceeds from your home sale. Learn more about how Knock works.

How does Knock.com make money?

Knock earns money through its 2% service fee (replacing the typical loan origination fee) and by selling loans in the secondary mortgage market (a standard practice among lenders). Learn more about how Knock works.

What is a Knock-certified agent?

Knock-certified agents are independent real estate agents who are familiar with Knock's service offerings and can guide their clients through the Home Swap process. They may also receive referrals through Knock. To become a Knock-certified, agents participate in a brief training and take a certification test. Learn more about how Knock works.

Methodology

Before writing this review, our team spent weeks studying real estate trade-in services to compare each company across multiple axes. Our research process included:

- Mystery shopping each company

- Content analysis of hundreds of online reviews

- Interviews with real estate experts

- Spreadsheet analysis to compare each service provider's terms and fees